Unveiling the Results of Giant Slimming: 3M, GE, Johnson & Johnson... Who Profited and Who Regrets?

3M

International Comprehensive Product Manufacturer

Solventum

Comprehensive healthcare service provider

If you were told that a medical company named Solventum (Shuwanuo) had an annual revenue exceeding 8 billion US dollars, you might feel surprised and confused, racking your brain for any clues about it. Now, once you learn that Solventum was actually spun off from the industrial giant 3M, everything makes sense.

As the first full fiscal year after going public, Solventum delivered impressive results in its 2025 financial report, with all key metrics surpassing market expectations. This seems to provide another compelling argument for the growing trend among global healthcare giants in recent years towards spin-off listings…

The renowned 3M was founded in 1902 and has a history of over a hundred years. Initially, its goal was merely to mine a mineral for producing abrasive grinding wheels, which led to its name, Minnesota Mining and Manufacturing Company.

In the following decades, 3M played a part in writing the history of modern industry and survived the Great Depression and two World Wars in the United States to become an industrial giant. Particularly, its invention of the world's first transparent tape in 1930, whose derivative product, adhesive bandage, became an important medical strategic material during World War II, saving countless lives.

Nevertheless, 3M did not officially start expanding its medical business until the 1970s. In 1978, 3M launched its first medical transparent dressing, Tegaderm. With innovative film material technology, this product was able to provide protection while allowing for direct observation of wounds, quickly becoming a standard supply in hospital settings. To this day, it remains one of the best-selling medical dressings globally.

Starting from the 1990s, through independent development and multiple mergers and acquisitions, 3M expanded its medical business from the initial medical dressings and consumables, gradually building a prototype of operations covering three major sectors: surgical care, dental, and healthcare IT. The healthcare sector has also become one of 3M's significant core business areas.

According to the fiscal year 2009 financial report, the revenue of the medical sector reached 4.294 billion US dollars, ranking second in 3M's business segments and accounting for 18.6% of the total revenue.

However, as part of a diversified industrial group, 3M's healthcare business has long been constrained by the overall pace of the group in terms of resource allocation and strategic decision-making, adopting a rather conservative strategy. Its average annual growth rate has remained at a low level of 1-2%, significantly lower than the growth rate of independent healthcare companies.

At the same time, there is still a certain proportion of non-medical related businesses within the medical sector. In the fiscal year 2021, non-medical related businesses such as industrial filtration and drinking water purification accounted for even 11.4% of the medical sector. This is obviously not conducive to the focus on medical business.

As the saying goes, "When it rains, it pours." Starting from 2016, 3M became embroiled in lawsuits over defects in its military earplugs. This "case of the century" is considered the largest mass tort lawsuit in U.S. history, with hundreds of thousands of veterans alleging that military earplugs produced by 3M and its subsidiaries caused permanent hearing damage. In 2023, the two sides finally reached a settlement, with the amount totaling $6 billion, posing a significant test to 3M's cash flow.

Against this backdrop, 3M began evaluating the spin-off of its healthcare business in 2022. On April 1, 2024, 3M's healthcare division officially spun off from 3M under the new name Solventum and was listed on the New York Stock Exchange, becoming an independent publicly traded company focused on the healthcare sector.

Its new name, Solventum, is a combination of two words: "solve," representing problem-solving and reflecting the new company's commitment to finding breakthrough solutions; and "entum," derived from the latter part of the word "momentum," symbolizing faster and more agile innovation.

Once granted independent decision-making authority, Solventum embarked on an extensive restructuring of its organizational framework. By launching the global Solventum Way restructuring initiative, the company aimed to decentralize, drive innovation, and rectify its previous organizational structure, which was "centralized, sluggish, and lacking in decision-making power and accountability."

Restructuring the product lines was also expected. In addition to concentrating resources on a few core product lines, Solventum sold its purification and filtration business to Thermo Fisher for $4.1 billion in February 2025, further focusing its operations on healthcare. The new company also gained much-needed funds to pay down debt and finance potential future acquisitions.

With financial backing, Solventum made its first significant acquisition as an independent entity in November of last year, purchasing acute care company Acera Surgical for $725 million. The regenerative medicine synthetic therapies offered by this company for complex wound repair in acute care settings will create synergies with existing products.

In addition, Solventum has also strengthened its international expansion by not only building a new factory in Brazil but also establishing a new distribution center in Europe, thereby enhancing its global market competitiveness.

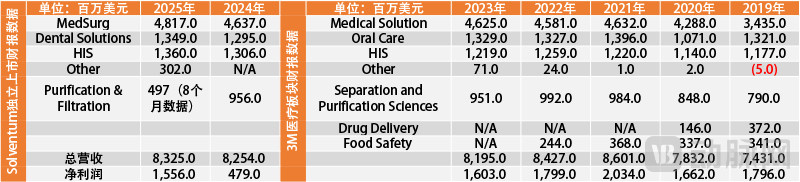

From the financial reports before and after the spin-off, these moves have evidently helped improve Solventum's business. In the 2023 fiscal year, 3M's healthcare business generated a total revenue of $8.195 billion. The 2024 fiscal year, as a transition year, achieved a full-year revenue of $8.254 billion, with organic growth of 1.2%. However, core business growth remained weak, with the largest segment, dental care, seeing organic growth of only 0.4%, healthcare information systems growing by 1.6%, and the surgical medical sector increasing by 1.2%.

Financial Data of Solventum Before and After the Spin-off (Compiled by VCBeat)

As the first full fiscal year after becoming independent, Solventum showed a clear recovery in the 2025 fiscal year. Annual total revenue reached 8.325 billion USD, with organic growth rising to 3.3%, surpassing market expectations.

If the previously sold purification and filtration business is excluded, the year-on-year growth rate of core business revenue has actually reached 4%. Specifically, the organic growth rate of dental solutions was 3.3%; medical information systems grew by 4.0%; and the surgical medical segment increased by 3.5%. Market penetration of key products such as negative pressure wound therapy, dental restoration materials, and medical coding systems also significantly improved.

The new company’s asset structure has also been optimized through the sale of non-medical businesses and acquisitions, with net debt significantly reduced from $7.3 billion at the start of the spin-off to $4.2 billion. Cost-saving initiatives are projected to save $500 million in operating costs annually. The first strategic acquisition has also laid the foundation for future growth in the surgical business.

According to Solventum's announced fiscal year 2026 performance guidance, the full-year organic revenue growth rate for fiscal year 2026 is expected to reach 2-3%, with available cash flow projected at 200 million U.S. dollars, indicating a positive outlook.

The spin-off of Solventum is merely a representative example of the recent global trend of healthcare giants undergoing spin-offs. Prior to Solventum, several other major companies had already executed spin-offs. The effectiveness of these spin-offs might be partially evaluated by comparing financial reports before and after the events.

The case of 3M's spin-off of Solventum is most similar to that of GE (General Electric) and Siemens. First, before the spin-offs, both companies, like 3M, were long-established industrial giants operating across multiple fields. Secondly, the spin-offs by these industrial giants all involved separately spinning off their medical divisions and listing them independently.

In January 2023, GE Healthcare was the first to spin off from GE and become independently listed. The corresponding fiscal year 2023 marks the first full fiscal year after its independent listing. Compared to before the spin-off, GE Healthcare's revenue significantly increased, with a growth rate of 6.7%. Additionally, the revenue of several core businesses showed notable improvement. Revenue from the Imaging department increased by 6.5%, PCS division revenue rose by 7.8%, and PDx division revenue surged by as much as 17.8%.

GE Healthcare Financial Data Before and After the Spin-off (Compiled by VCBeat)

Subsequently, after a brief adjustment in fiscal year 2024 (revenue growth of 0.6%), GE Healthcare rebounded strongly in the recently concluded fiscal year 2025, achieving revenue of $20.63 billion and a growth rate of 4.8%. This also marks the first time that the segment's revenue has exceeded $20 billion since fiscal year 2017 (the earliest year available in the official financial reports).

Before the split, GE Healthcare underwent multiple adjustments (Compiled by VCBeat).

On the surface, fiscal year 2025 seems to have only returned to previous levels — in fiscal years 2019 and 2018, revenue in this segment reached $19.9 billion and $19.8 billion, respectively. However, these figures prior to the spin-off also included revenue from the now-sold BioPharma business, which alone generated as much as $3.29 billion in fiscal year 2019.

Until 2019, GE sold its BioPharma business, which belonged to the medical segment, to Danaher for $21.4 billion. This also resulted in the full consolidation of the 2021 fiscal year, with the entire GE medical segment's revenue declining to $17.59 billion.

If this is used as a benchmark, the annual revenue of GE Healthcare after its independence has actually increased by as much as 17.3%. It should be noted that, before the spin-off, during the fiscal years 2017-2021, excluding the impact of the sale of the BioPharma business, the revenue of GE's healthcare segment had not seen much change for many years. The results of the spin-off have been clearly reflected in the performance.

Siemens made the move to split earlier. As early as March 2018, Siemens Healthineers was independently spun off from the group and listed. The fiscal year 2019 was its first full fiscal year after the independent listing, achieving a total annual revenue of 14.519 billion euros, an increase of 9.6% year-on-year.

Siemens Healthineers Financial Data Before and After the Spin-off (Compiled by VCBeat)

Among them, several core businesses have seen significant growth compared to the previous fiscal year, with Imaging business revenue increasing by 9.6%, Diagnostics business growing by 4.3%, and Advanced Therapies business rising by 8.6%.

In 2020, Siemens Healthineers announced the acquisition of radiation therapy giant Varian for a record $16.4 billion. Its performance immediately entered a high-growth mode, and in fiscal year 2022, revenue exceeded €20 billion for the first time. In fiscal year 2025, Siemens Healthineers' annual revenue reached €23.375 billion, a year-over-year increase of 4.5%; net profit reached €2.168 billion, a year-over-year increase of 10.7%.

Comparable financial data of Siemens Healthineers before the spin-off (Compiled by VCBeat)

Compared to the healthcare segment's revenue of 13.677 billion euros in the fiscal year 2017, the fiscal year 2025 is almost approaching the recreation of Siemens' healthcare business. According to Siemens' annual reports over the years, from fiscal year 2013 to 2017, the annual revenue of its healthcare segment did not change significantly. The independent listing was obviously a successful decision for Siemens' healthcare business.

In addition to industrial giants, medical-focused giants have also begun to spin off their businesses for independent listings in recent years. In October last year, Johnson & Johnson (J&J), a global medical giant, announced that it would spin off its orthopedics business for an independent listing. This is actually not the first spin-off by J&J. In May 2023, J&J’s original consumer health division was independently listed under the new name Kenvue. The division covers three areas: self-care, skin health, and beauty, and owns several well-known brands such as Neutrogena, Band-Aid, Tylenol, and Dabao.

Kenvue's Financial Report Data After Independent Listing (Compiled by VCBeat)

However, Kenvue's performance since its listing has been mediocre. In the 2024 fiscal year, its first full fiscal year as an independently listed company, it achieved annual revenue of $15.455 billion, a 3.3% increase from the 2022 fiscal year, but net profit was only $1.03 billion, a drop of as much as 50% compared to the 2022 fiscal year. Net profit rebounded somewhat in the 2025 fiscal year, but annual revenue fell by 2.1%. Meanwhile, the performance of its three core business segments not only failed to improve but instead showed a trend of gradual decline.

Last November, Kimberly-Clark, the global consumer goods giant, acquired Kenvue for approximately $48.7 billion, and Kenvue's path to independent listing will soon come to an end. From Kenvue’s perspective, this is clearly not a successful spin-off.

J&J Financial Data Before and After the Split (Compiled by VCBeat)

J&J Comparable Financial Data Before Split (Compiled by VCBeat)

Interestingly, the original parent company J&J has fared better after the spin-off. According to J&J's recalculated financial reports of its existing businesses over the years, both its overall business and its two core businesses—innovative drugs and medical devices—have achieved four consecutive years of performance growth. In the fiscal year 2025, revenue reached $94.193 billion, a year-on-year increase of 6%, which is already very close to the highest level of the entire J&J before the spin-off (fiscal year 2022 revenue of $94.943 billion). The extent of this strong growth is evident.

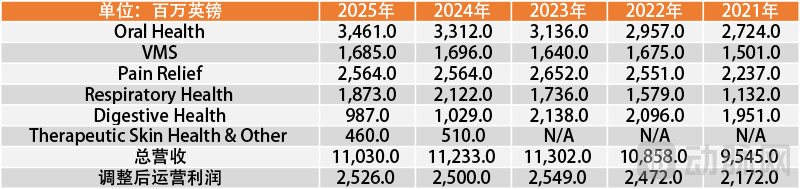

Interestingly, a similar situation can be seen with pharmaceutical giants GSK (GlaxoSmithKline) and Haleon. The latter, originally GSK's consumer healthcare business, owns well-known brands such as Caltrate, Centrum, Sensodyne, Panadol, Voltaren, Contac, Bactroban, Flixonase, and Polident, and was independently listed in July 2022.

Haleon's Financial Report Data After Independent Listing (Compiled by VCBeat)

Apart from a 4.1% revenue growth in the first full fiscal year, Haleon's revenue continued to decline in the following two fiscal years. In the 2025 fiscal year, it achieved revenue of 11.03 billion pounds, almost falling back to the level before its spin-off.

What is most troubling is that, among Haleon's six business segments, only oral health is showing continuous growth, while the other businesses are experiencing a slow decline. Currently, Haleon’s performance after the spin-off does not look optimistic. Referring to Kenvue's situation, it may not be long before a major company considers acquiring Haleon.

GSK Financial Data Before and After the Split (Compiled by VCBeat)

Instead, GSK, the parent company before the spin-off, has experienced continuous growth in recent years. In the fiscal year 2025, GSK achieved revenue of 32.667 billion pounds, a year-on-year increase of 4.1%. This revenue is already close to the total revenue of GSK before the spin-off (34.114 billion pounds in the fiscal year 2021). If recalculated by excluding the previous consumer healthcare business from the annual financial reports, the business of post-spin-off GSK has actually maintained growth for five consecutive years.

Particularly noteworthy is that after the spin-off, GSK's operating profit surged significantly, with an operating profit of £7.932 billion in the 2025 fiscal year, markedly higher than the pre-spin-off operating profit (£6.201 billion in the 2021 fiscal year) despite lower revenue.

On the surface, the reasons for the giants to split their medical businesses vary. Some aim to streamline structures and focus on core businesses, while others seek to摆脱低增长业务的束缚, and there are even cases of emergency splits. However, it is certain that splitting has become a current trend.

On the one hand, in recent years, the capital market has been more optimistic about "specialized and refined" enterprises. Compared with large-scale, diversified conglomerates, enterprises specializing in a certain niche business are now more likely to gain capital favor. Historically, the combined market value of the two companies after a spin-off often exceeds the market value of the original single company.

On the other hand, the wave of spin-offs is also a result of the healthcare industry's own evolution. The recent trends of digitalization and precision in the medical device field require companies to have agile organizations and rapid technological iteration capabilities. This is precisely a structural weakness of diversified conglomerates, especially when their healthcare businesses struggle to secure sufficient internal resources.

Of course, judging from the performance of spin-offs by several major giants, spinning off and listing independently may not be a panacea, with varied results. Generally speaking, for technology-driven medical device businesses with relatively deep barriers, the benefits of focus after a spin-off will continue to materialize over the medium to long term. Both Siemens Healthineers and GE Healthcare have shown this trend.

On the contrary, for the consumer health business in the broader healthcare sector, although a spin-off can independently face the pressures of market competition, forcing brand innovation and efficiency improvements, the macroeconomic environment has been under pressure in recent years, with consumer downgrading becoming the prevailing trend. Against this backdrop, even companies with many flagship products like Kenvue and Haleon are finding it difficult to reverse the situation.

However, by spinning off their consumer health businesses, J&J and GSK have been able to focus limited resources on their high-growth core medical businesses, enhancing their main business performance and largely offsetting the revenue loss from divesting the consumer health segment. From this perspective, 1+1>2 still holds true, and the value of separating the healthcare business remains intact.

Under this logic, it is believed that more giants will continue to split in the future. Especially for diversified industrial giants like 3M, GE, and Siemens, spinning off their medical businesses into independent listings will likely remain an unavoidable topic. Even major medical device companies are already involved. For instance, Medtronic has already spun off its diabetes business MiniMed for an independent listing, and J&J is further advancing the independent listing of its orthopedics business.

Spin-offs have evolved into an industry-wide structural transformation. Who will be next? Let's wait and see.