Who can generate their own resources? Everest Medicines' answer is worth a look

Everest Medicines

Developer of Innovative Therapies

After the innovative drug industry has undergone a reevaluation of its valuation and a retreat of capital, a question has become increasingly critical: Who can break free from continuous cash infusions and truly achieve self-sustaining profitability?

In 2026, this question is being answered in phases by Everest Medicines.

On April 8, Everest Medicines announced a proposed acquisition of Hasten Biopharmaceutical (Singapore) ("Hasten Singapore") for US$250 million. This move follows its impressive financial report for 2025, which showed that Everest Medicines achieved a total revenue of RMB 1.707 billion in 2025, representing a significant year-over-year increase of 142%.

More significantly, Everest Medicines achieved its first annual profit of 187 million RMB under the Non-IFRS, and realized positive operating cash flow in the fourth quarter of last year. This indicates that Everest Medicines has officially entered a new phase of "self-sustainability."

For a long time, Biotech has been regarded as a synonym for high investment and slow returns. However, Everest Medicines has officially entered the value realization phase through the dual drivers of "licensing collaboration + self-research." The acquisition of Hasten Singapore by Everest Medicines is not simply about licensing deal or expansion; rather, it serves as a validation of the commercial platform's capacity spillover and regional replication capabilities.

Everest Medicines is transitioning from a Biotech driven by R&D investment to a Biopharma powered by commercialization.

In this regard, Wu Yifang, Chairman of Everest Medicines, stated: "The core of Everest Medicines' 2030 strategy is to ride on the wave of 'China's booming innovative pharmaceuticals industry,' and through licensing collaborations with like-minded innovative companies, bring Chinese innovation to clinical applications, benefiting patients, growing our own capabilities, achieving self-sustainability, supporting innovative R&D with our own profits, and creating greater future value. The question we face in the coming years is how to transform from a qualified pharma company into an excellent one, which will require an upgrade in strategic capabilities."

Profit Inflection Point, Commercial Platform Value Realization

For innovative drug companies, profitability itself is not scarce; what is scarce is sustainable profitability.

In 2025, Everest Medicines delivered the most impressive annual report since its listing. Total annual revenue reached 1.707 billion RMB, marking a 142% year-on-year increase. Under non-IFRS, the company achieved a profit of 187 million RMB, realizing its first annual operating profit. By the end of the year, cash reserves amounted to 2.731 billion RMB, providing substantial resources for future licensing, self-research, and strategic expansion.

One of the contributors to this report card is NEFECON®. NEFECON®, which holds a cornerstone position in the first-line treatment of IgA nephropathy, achieved sales of 1.44 billion RMB in its first full year of commercialization, with a year-on-year increase of over 300%, setting a record for chronic disease medications.

This performance is built on multiple foundations. Data shows that the population of IgA nephropathy patients in China exceeds 5 million, with approximately 100,000 new confirmed cases annually, indicating an urgent unmet clinical treatment need. NEFECON® directly addresses a vast unmet market of over 5 million patients. Financial reports reveal that NEFECON® was included in the medical insurance system through negotiations in its first year on the market. To date, it has achieved medical insurance coverage in 29 provinces and has been incorporated into single-payment management. Additionally, this drug has been included in the 2025 KDIGO guidelines and China's first IgAN guidelines, establishing it as the preferred treatment option targeting the underlying cause.

With the continuous accumulation of evidence for NEFECON® in the Chinese population, research results further confirm its significant clinical value in the new management strategy for IgA nephropathy, which emphasizes "treating the cause, early treatment, and long-term treatment." The efficacy of NEFECON® in special populations has also been validated, reinforcing its position as a cornerstone in the first-line treatment of IgA nephropathy.

Rogers Yongqing Luo further analyzed that the growth in sales of NEFECON® is not only due to market penetration and expanded hospital coverage, but also stems from a revolution in treatment concepts – authoritative guidelines now recommend lowering the treatment initiation threshold from "proteinuria greater than 1 gram" to "0.3 grams." With the treatment window broadened, more patients who should be treated but have not yet been treated will be included.

The key change for Everest Medicines lies in the shift of its profit sources from a single product breakthrough to systematic output.

Everest Medicines' sales team consists of fewer than 200 people, with per capita output exceeding 7.3 million RMB and a cost-to-sales ratio of only 30%, representing extremely high operational efficiency within the industry. Everest Medicines has not relied on high costs to drive growth but has instead established a highly efficient commercialization model.

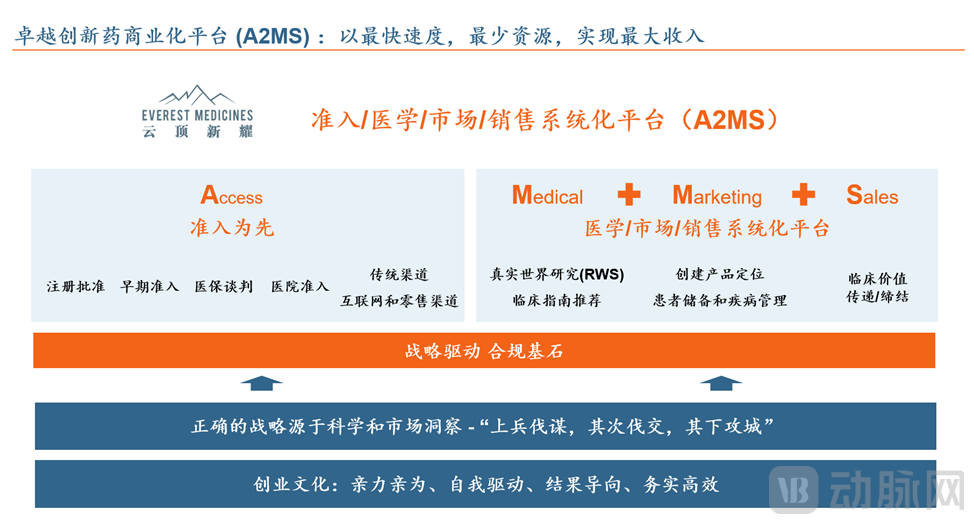

As Rogers Yongqing Luo, CEO of Everest Medicines, said: "NEFECON® has set a record in the history of China's pharmaceuticals, and the reason behind it is our robust commercialization platform, the A2MS — Access, Medical, Marketing, Sales systematic platform, which demonstrates the capability of the entire value chain of commercialization."

This platform capability, after being validated by NEFECON®, is being rapidly replicated. In February 2026, after VELSIPITY® was approved for marketing in mainland China, it took only 21 working days to issue the first prescription and quickly covered patients in key areas across the country. XERAVA™'s in-hospital sales in 2025 increased by 44% year-on-year, generating revenue of 262 million RMB.

To date, the continued growth of NEFECON®, the rapid implementation of VELSIPITY®, and the steady increase of XERAVA™, have expanded Everest Medicines' product portfolio from a single core to multiple varieties. On this basis, the success of NEFECON® has validated the effectiveness of Everest Medicines' A2MS innovative drug commercialization platform, demonstrating that its commercialization capabilities can be replicated across different therapeutic areas.

Everest Medicines' commercialization capabilities have been upgraded from "single-product driven" to "system-driven."

Strategic Layout in Advance to Seize the First-Mover Advantage in the Asia-Pacific Region

The acquisition of Hasten Singapore's Asia-Pacific business is another upgrade to Everest Medicines' commercialization blueprint. Why the acquisition? It lies in replicating the proven commercialization capabilities in China, through the integration of mature products, to broader markets.

The core value of Hasten Singapore lies in its ready-made commercialization capabilities in the Asia-Pacific region. Everest Medicines disclosed that Hasten Singapore is expected to achieve regular revenue of 82.23 million U.S. dollars and EBITDA of 27.27 million U.S. dollars by 2025. It has a portfolio of 14 mature chronic disease products and a professional sales team of over 120 people, covering eight regional markets including Singapore, Malaysia, the Philippines, Thailand, and Australia. Through cooperation with Hasten Singapore, Everest Medicines can integrate mature product management capabilities and possess a team encompassing registration, market access, marketing, medical, and sales expertise.

For Everest Medicines, the acquisition has an immediate effect, instantly boosting profits and enhancing overall profitability. However, this collaboration is not merely a simple product introduction but rather an integration of capability systems.

Thus, Everest Medicines' commercialization system is expected to be upgraded to a full-channel, multi-product adaptation, and from local validation to regional replication.

In recent years, an increasing number of Chinese pharmaceutical companies have set their sights on the Asia-Pacific region, particularly Southeast Asia, as the starting point for their international expansion. Regulatory agencies in countries like Singapore and Indonesia are exploring ways to accelerate the introduction of innovative drugs from China. Chinese pharmaceutical companies can bypass the stringent and lengthier approval processes in Europe and the U.S., achieving their first round of international presence at a lower cost.

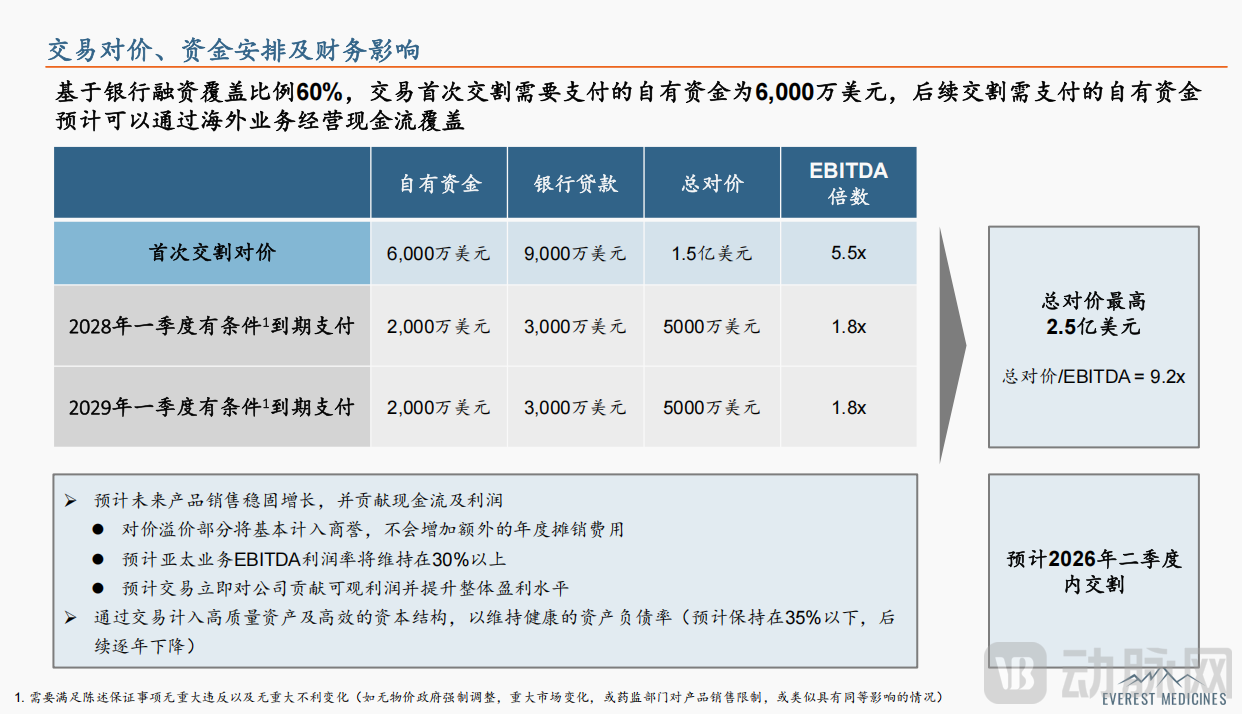

Notably, the fairness of this transaction is safeguarded by multiple mechanisms. First, as an independent appraiser, PG Consulting assessed the value at $320 million based on the market approach and 2025 EBITDA ($27.27 million). In contrast, the maximum total consideration for this deal is $250 million, representing a discount of approximately 22% compared to the valuation, with the transaction price being lower than the independent appraisal. Second, the total transaction consideration of $250 million will be paid in three installments. The initial payment required at the first closing amounts to $60 million in equity capital, while subsequent payments can be covered by the operating cash flow from overseas business operations.

From a market perspective, the value of this acquisition goes far beyond financial returns. According to IQVIA data, the pharmaceutical market in the Asia-Pacific region exceeds $60 billion and is in a period of rapid growth. China's innovative drug assets are flourishing, but the penetration rate of innovative drugs in the Asia-Pacific region remains significantly low, with only about 20%-25% of EMA-approved drugs also approved in the Asia-Pacific. As multinational pharmaceutical companies streamline non-core APAC operations, the first-mover advantage in this fragmented market is rapidly amplifying, and a window of opportunity for strategic positioning is emerging.

In addition, Everest Medicines also provides CSO services for six mature products under Hasten Biopharmaceutical, involving emergency and critical care, cardiovascular, and metabolic fields. On December 11, 2025, Everest Medicines and Hasten Biopharmaceutical officially reached a cooperation agreement. According to the commercialization service agreement, Everest Medicines Limited, a wholly-owned subsidiary of Everest Medicines, will rely on its existing sales and marketing system to provide commercialization services for six mature products under Hasten Biopharmaceutical.

From a strategic synergy perspective, Everest Medicines' Asia-Pacific commercialization has initially taken shape, covering Hong Kong, Macao, and Taiwan regions of China, as well as Singapore and South Korea markets. It is expected to achieve revenue exceeding 30 million RMB by 2025, with a nearly 20-person in-house team that possesses capabilities in registration, market access, marketing, medical affairs, and sales. Meanwhile, the company holds Asia-Pacific rights for nine innovative drugs, three of which—NEFECON®, XERAVA™, and VELSIPITY®—have already been commercialized, while six others are in clinical development.

With the advancement of medical insurance, the three commercialized products will successively enter the medical insurance scaling period in multiple Asia-Pacific markets starting from 2027.

Everest Medicines' acquisition of Hasten Singapore equals gaining full value chain capabilities to drive business growth, marking a crucial step in the "overseas replication" of its commercialization capabilities. Relying on this one-stop platform for innovative drug sales in emerging Asian regions, Everest Medicines can complete the pre-positioning deployment of commercialization capabilities before product launch.

Looking to the Future, "Licensing Collaboration + In-House R&D" Cycle Drives Growth

Commercialization solves the present, but the long-term value of innovative drug companies still depends on pipelines and technology. Everest Medicines' solution is to build a cyclical system of "licensing cooperation + in-house R&D."

Through circulation and collaboration, a sustainable and replicable growth model is formed. Commercialization provides cash flow and validates the product, licensing deal rapidly expands the product matrix, and in-house research enhances long-term value and potential.

On the licensing deal front, Everest Medicines demonstrates a clear and systematic pace of strategic layout. The 2025 annual report shows that in the past six months, Everest Medicines has introduced and collaborated on four innovative drugs and six established original research products, further expanding therapeutic areas and increasing pipeline depth. Meanwhile, Everest Medicines explicitly stated its goal to introduce three to five blockbuster products annually, striving to achieve regulatory approval within two to three years and reach a peak sales of over 2 billion RMB per product within five to six years.

Behind this licensing pace, Everest Medicines is rapidly building a multi-dimensional pipeline matrix across multiple therapeutic areas and product stages. For example, Everest Medicines has introduced VIS-101, a VEGF/ANG-2 bispecific antibody with BIC (Best-in-Class) potential in the ophthalmology field; MT1013, a first-in-class dual-target agonist in the renal field to enhance its chronic kidney disease portfolio; and in the cardiovascular field, it has laid out Etripamil Nasal Spray to fill the gap in out-of-hospital emergency treatment, as well as Lerodalcibep, a next-generation PCSK9 inhibitor.

Wu Yifang emphasized that before the R&D can truly produce products, it is necessary to continuously build a sustainable product pipeline through licensing deals.

After clarifying the licensing pace, Everest Medicines adopts an end-to-end approach, starting from patient needs. It first evaluates the clinical and commercial value of a product before making project initiation decisions. Underlying this concept is Everest Medicines' steadfast "Best-in-Disease (potential for the best solution in a disease area)" DNA.

As Rogers Yongqing Luo explained: "The biggest difference lies in the different ways of thinking. Best-in-Class is about the drug mechanism, while Best-in-Disease starts from the patient's perspective. The concept of Best-in-Disease will run through our entire value chain from R&D to commercialization."

If before 2030, licensing products will be the main growth driver for Everest Medicines. Then, after that, self-developed products are expected to shine. Everest Medicines is not only a company with blockbuster products capable of rapid scaling but also a platform-based pharmaceutical enterprise with systematic R&D capabilities.

Currently, Everest Medicines is focusing on an AI-driven mRNA platform, with its In Vivo CAR-T technology platform ranking among the global leaders. The personalized cancer vaccine EVM16 has completed dose escalation in IIT research and is scheduled to release preliminary data at AACR in April 2026.

The universal tumor vaccine EVM14 has achieved dual IND approval in China and the United States and completed the enrollment of the first patient. The In Vivo CAR-T project EVM18 has completed preclinical proof-of-concept and initiated clinical research in humans, with proprietary intellectual property and a globally leading technology platform.

Everest Medicines clearly stated that it would not "sell the seedlings prematurely" for self-developed assets, but instead seek strategic and capability-complementary partners to jointly develop and realize long-term value.

Ultimately, Everest Medicines' self-sustaining "hematopoiesis" is not just about profitability, but rather the positive cycle being formed among the three pillars of commercialization, licensing deals, and in-house research. In the short term, profitability will be achieved through commercialization, with cash flow supporting licensing deals and R&D. In the medium term, licensing operations will, in turn, nourish the growth of sales operations, creating an internal virtuous cycle. In the long term, independent research will provide more room for imagination and value creation.

At present, the market is more concerned about whether enterprises have real commercialization capabilities, whether they can continuously replenish their pipeline, and whether they can form a closed loop for long-term growth. The path of Everest Medicines offers a possible answer. Instead of relying on a single blockbuster product, they focus on building a replicable commercialization system to form an internal self-sustaining cycle.

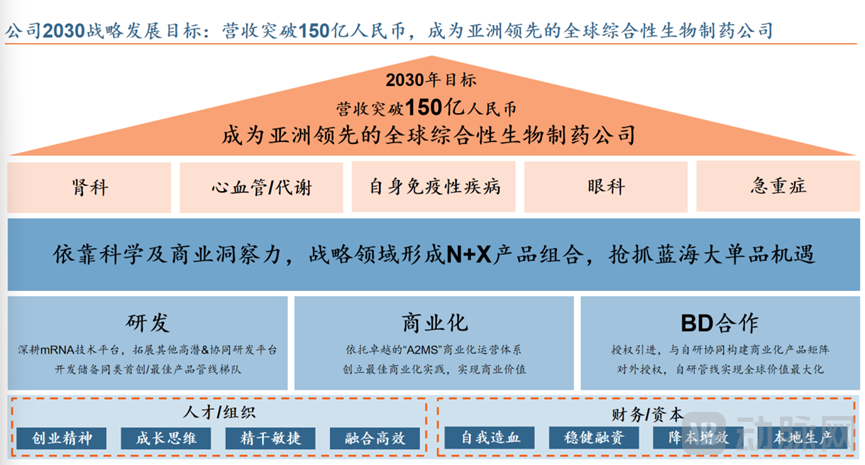

Who can continuously generate revenue and move towards scaled expansion? Everest Medicines is transitioning from a Biotech to a Biopharma with self-sustaining capabilities and is beginning to enter the value realization phase. By 2030, Everest Medicines plans to achieve revenue exceeding 15 billion RMB and will continue to build an "N+X" product portfolio in key strategic areas such as nephrology, cardiovascular and metabolic diseases, autoimmune disorders, ophthalmology, and critical care, seizing opportunities in blue ocean blockbuster products.