New drug priced at 3,000 RMB per box sells out quickly; are young "wind cluster" entrepreneurs making a profitable business?

As the transition from spring to summer arrives, it is once again the peak season for urticaria. At the end of last month, a product named "Rhapsido®" (remibrutinib) tablets quietly launched on JD Health and Alibaba Health. Priced at nearly 3000 RMB per box, yet hundreds of units were sold within days.

Previously, on social media platforms, Rhapsido® had almost become a phenomenon-level new drug. In September 2025, Rhapsido® received FDA approval in the United States for the treatment of chronic spontaneous urticaria that is unresponsive to antihistamines. When the news reached China, the urticaria patient community on Xiaohongshu quickly heated up. "Wait strategies," "medication diaries," and "proxy purchase channels" successively flooded the screen, with the comment section filled with patients who had been waiting for years. One person commented, "I've been taking antihistamines for five years and have been on Omalizumab for two years, but still can't control it—I'm just waiting for this."

For an increasing number of young people trapped in "wheals," Rhapsido®, an oral medication with visibly noticeable effects, has opened the door to a new world. However, behind the heated launch of

Rhapsido® lies a profound transformation in the development logic of the increasingly competitive autoimmune drug market. Rhapsido® has unveiled a corner of a hidden and turbulent track, and this change is redefining the future autoimmune drug market.

Phenomenal "Wind Cluster" New Drug

In China, chronic urticaria is troubling an increasing number of young people.

In the context of Traditional Chinese Medicine (TCM), chronic urticaria is referred to as "wind cluster" (wind rashes). The wind comes, forms rashes, disperses, and then returns. Essentially, urticaria is an allergic skin and mucous membrane disease characterized by wheals and angioedema. Data shows that in China, the prevalence of chronic urticaria is approximately 1%, with a total patient population reaching about 13 million. Among them, young and middle-aged individuals are most susceptible to chronic urticaria, especially young and middle-aged women.

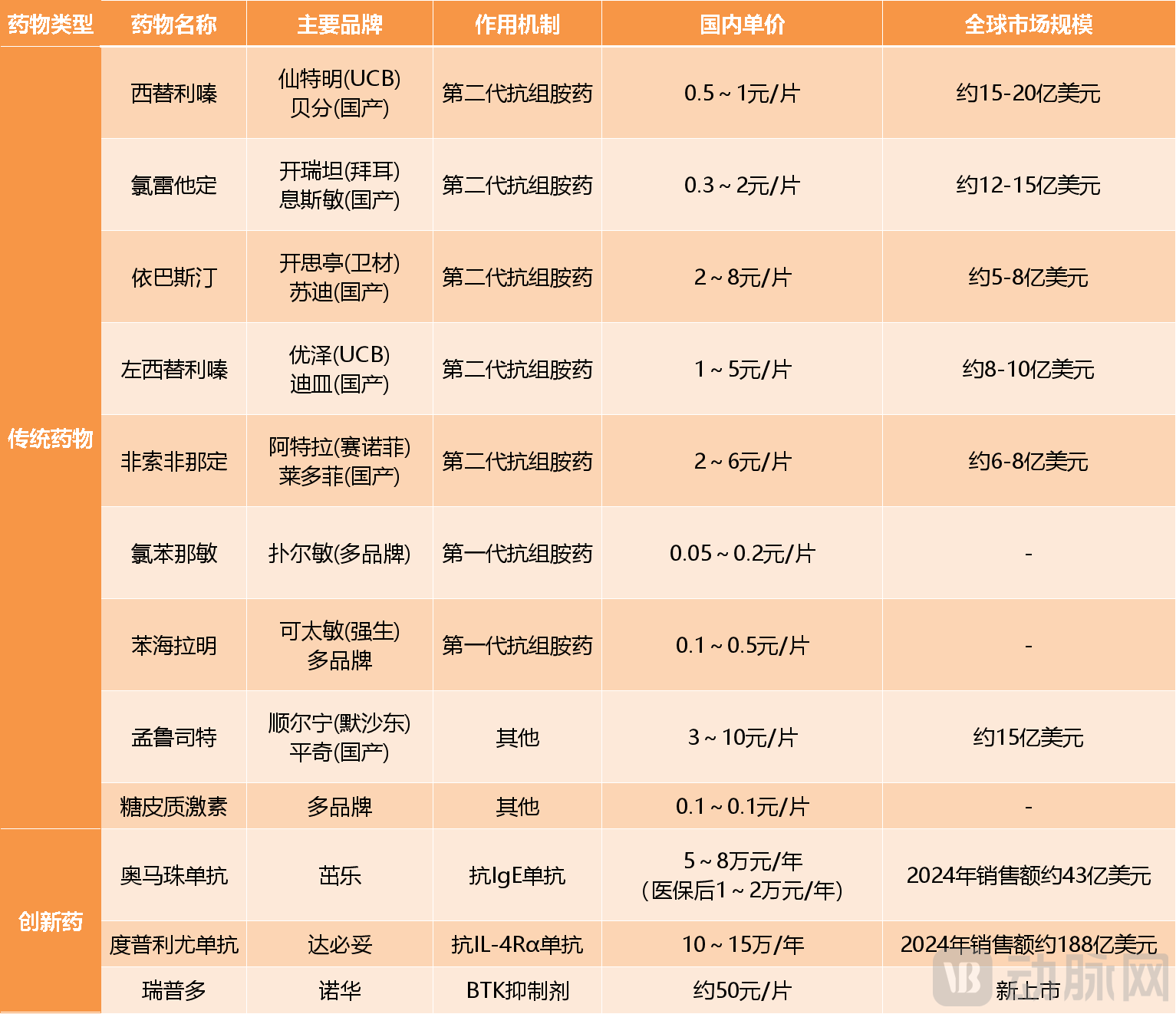

In most cases, chronic urticaria does not receive adequate treatment. At present, the clinical treatment of chronic urticaria is still dominated by traditional second-generation antihistamines. Innovative biologics such as omalizumab are changing the treatment landscape. Typically, chronic urticaria follows a "step-by-step" standard treatment principle. Second-generation antihistamines, such as cetirizine and loratadine, are used at the onset of the disease. If ineffective, the dosage is increased or combination therapy is applied. If still ineffective, the treatment is escalated to biologics such as omalizumab, and finally immunosuppressants like cyclosporine are used.

Common Chronic Urticaria Medications on the Market Data Source: Collated from Public Information

Common Chronic Urticaria Medications on the Market Data Source: Collated from Public Information

But in practice, patients often feel that there are no effective drugs available. The progression of the disease and the ineffectiveness of the drugs tend to exceed expectations, while the complexity and side effects of upgraded drugs increase sharply, with unsatisfactory efficacy. About half of the patients find that standard-dose second-generation antihistamines are directly ineffective. Of these, nearly half also find no effect after increasing the dose or combining antihistamines for a year, and more than 40% of patients still have not achieved effective control after one year. As a back-line treatment option, omalizumab needs to be injected in the hospital, but about 40%-60% of patients experience poor efficacy or are completely ineffective.

Relatively speaking, the change in Rhapsido® can be described as revolutionary. First of all, in terms of efficacy, unlike existing drugs that directly alleviate symptoms, Rhapsido® targets upstream disease mechanisms. Rhapsido® targets Bruton's tyrosine kinase (BTK), a popular target for novel tumor drugs, and inhibits histamine release from mast cells and basophils by blocking the BTK cascade reaction, thereby cutting off urticaria attack signals at the source. Mechanistically, Rhapsido® can be applied to all chronic urticaria patients who are unresponsive under the stepwise treatment system.

Existing clinical data has partially validated this. In the pivotal Phase III trials REMIX-1 and REMIX-2, Rhapsido® demonstrated significant symptom improvement early in treatment for patients with chronic urticaria who were unresponsive to antihistamines, and this effect persisted until week 52. By the week 52 assessment, nearly half of the patients experienced complete absence of itching and urticaria symptoms—a proportion that is quite rare in the history of chronic urticaria treatment.

More importantly, Rhapsido® adopted an oral dosage form. In the past treatment of chronic urticaria, many patients preferred to increase the dose or combine medications after antihistamines failed, or even endure the distress caused by wheals, rather than moving on to the next stage of biologics. This hesitation was mainly due to these biologics being limited to in-hospital injections. However, the trial-and-error cost of Rhapsido® is very low. VCBeat noticed that on internet healthcare platforms like JD Health and Alibaba Health, patients can conveniently access medication through online doctor consultations and prescriptions. Patients take the medication orally twice a day, with necessary guidance provided by online doctors, easily completing the closed loop from diagnosis to treatment.

As a result, this new drug, priced at nearly 3000 RMB, has become a phenomenal product. Of course, since Rhapsido® is currently approved for use in patients who do not respond to antihistamine treatment, there is not yet sufficient clinical evidence to support its efficacy in patients refractory to omalizumab. In addition, although BTK inhibitors have been widely used in the field of hematological tumors and long-term safety data is relatively robust, the long-term safety of Rhapsido® in treating chronic urticaria still needs time to verify.

Ten Years of Dominance, Gritting Teeth to Defend the Throne

In the biologic treatment market for chronic urticaria, Novartis has been unrivaled for over a decade. The aforementioned omalizumab is precisely the first biologic agent for chronic urticaria under Novartis. In 2014, Omalizumab was approved by the FDA for chronic spontaneous urticaria, becoming the world's first approved biologic for chronic urticaria. For the next decade, omalizumab virtually defined this market, with no new biologics for chronic urticaria gaining approval.

The early molecule of omalizumab was proposed by a biotech company named Tanox. After several transitions, a pattern of co-development by Novartis, Genentech, and Tanox was formed, with Novartis responsible for production and global commercialization. From the molecular patent to the approval of the chronic urticaria indication, the three parties cumulatively invested no more than 4 billion US dollars, yet earned over 53 billion US dollars after its market launch. Such an input-output ratio has made omalizumab one of the most successful drugs in the anti-allergy field.

During this period, several MNCs attempted to develop drugs for chronic urticaria but encountered setbacks one after another. For instance, in July 2024, AstraZeneca abandoned its exploration in the chronic urticaria field after a Phase IIb clinical trial showed that benralizumab did not outperform placebo in improving itch severity and urticaria activity. GSK and Johnson & Johnson had already given up earlier. Previously, GSK had evaluated the possibility of using its own mepolizumab for chronic urticaria, but ultimately decided not to enter the market following AstraZeneca's failure. As for Johnson & Johnson, it abandoned the development of an anti-IgE nanobody during the preclinical research stage due to safety concerns.

At that time, these MNCs merely considered chronic urticaria as one of the options for expanding autoimmune indications. The previously mentioned benralizumab and mepolizumab both belong to asthma medications. Even omalizumab was initially developed as an asthma drug. Its mechanism of action involves binding to free IgE, blocking the interaction between IgE and the FcεRI receptor on mast cells, thereby inhibiting the chain reaction that triggers allergic responses. Researchers later discovered that this mechanism is also applicable to chronic urticaria, as its core pathological process similarly involves IgE-mediated mast cell activation.

For a long time, the development of new drugs for chronic urticaria has been extremely challenging, but with a small market scale, the cost-effectiveness of development is not high. Under the traditional development mindset, drugs for chronic urticaria mainly target the abnormal activation of mast cells itself, which may be triggered by multiple pathways, leading to poor effectiveness of specific drugs. Coupled with the extremely complex pathogenesis of chronic urticaria and the high degree of patient heterogeneity, this results in difficult clinical trial designs and high failure risks. Before the launch of omalizumab, the global market size for chronic urticaria was less than 1 billion US dollars. Even during the period when omalizumab had exclusivity, its sales peak was just over 1.5 billion US dollars. MNCs naturally have no reason to force a bet.

But a turning point occurred around 2023, as an increasing number of new targets emerged, reigniting the enthusiasm for the development of new drugs for chronic urticaria. Especially with the approval of Rhapsido®, the possibility of developing chronic urticaria drugs based on new mechanisms was validated, prompting more multinational corporations (MNCs) to return to the battlefield. In the new phase, pharmaceutical companies are breaking away from traditional development logic to design new drugs with better efficacy and safety profiles. The BTK target chosen by Rhapsido® is one such representative example. In addition to Novartis, Roche's BTK inhibitor Fenebrutinib has also advanced the indication for chronic urticaria to Phase III clinical trials. Furthermore, companies like Hengrui, Pfizer, AbbVie, and Eli Lilly are attempting to develop chronic urticaria drugs targeting JAK. Among them, Hengrui's JAK inhibitor Ivarmacitinib is the furthest along in development for chronic urticaria, currently undergoing Phase III clinical trials.

In fact, in April 2025, just before the launch of Rhapsido®, Sanofi's currently popular autoimmune blockbuster Dupilumab gained approval for use in chronic urticaria ahead of its rival. Facing fierce competition, Novartis is encountering greater challenges in defending its position but remains determined to hold its ground. In addition to advancing the oral drug Rhapsido®, Novartis has also invested heavily in more cutting-edge mechanisms. In March 2025, Novartis announced an $830 million licensing agreement with Japan's Kyorin Pharmaceutical to gain global exclusive development rights to KRP-M223, with a $55 million upfront payment. The latter is one of only two MRGPRX2 antagonists worldwide that have entered clinical trials, aimed at controlling urticaria and angioedema.

A $2 billion small market, from easy profits to gritting teeth and holding on, the deeper logic behind it is the intensifying competition in the autoimmune market entering a white-hot phase.

A Turning Point in the History of New Autoimmune Drugs

VCBeat noticed that since 2025, the global autoimmune market has started to explode, with a batch of new drugs that fill decades-long clinical gaps being approved in a concentrated manner, completely rewriting the treatment landscape for multiple diseases. 2026 has become the year of concentrated payoff for innovative autoimmune drugs. As more and more clinical gaps are filled by new drugs, the autoimmune market, considered a highly promising blue ocean, is becoming extremely competitive. More importantly, as indications and end-user groups are being segmented more finely, the conventional competition logic of using newly added indications to build barriers in the autoimmune market is becoming increasingly unsustainable.

From the approach to drug use to the development of new drugs and treatment strategies, the newcomers in the autoimmune market are constantly innovating and changing. New drugs like Rhapsido®, which have quickly gained popularity, are not isolated cases—blockbusters can emerge from every dimension.

First, the treatment approach has shifted from injections to oral drugs. This is what Novartis, a veteran in the autoimmune field, is currently experiencing. In the past, the treatment of autoimmune diseases heavily relied on injectable biologics, which had significant limitations in terms of administration. However, most of the autoimmune drugs approved in the past two years are oral small-molecule drugs. The previously mentioned Rhapsido®, for instance, is an oral small-molecule formulation. Additionally, in 2025, Sanofi's Rilzabrutinib was the first to receive FDA approval, becoming the world's first BTK inhibitor for use in the autoimmune field, primarily targeting Immune Thrombocytopenia (ITP), also as an oral small-molecule drug. In the first quarter of 2026 alone, there was a surge in approvals for new oral autoimmune drugs, with four products launching breakthrough treatments for diseases such as psoriasis, severe psoriasis, and multiple sclerosis.

Oral dosage forms of drugs have greatly improved the treatment experience for patients and are highly likely to become the key to disrupting the existing market. They also represent the most promising entry point for blockbuster products in the autoimmune market. From a longer-term perspective, compared with previous injectable formulations, oral drugs enable diseases like autoimmune conditions, which usually require long-term treatment, to make a leap from passive medical visits to active management, and the market size of autoimmune treatment will expand accordingly.

Secondly, there is a shift in the approach to new drug development, from single-target monopoly to multi-target battle. Previously, the field of autoimmune treatment had long been monopolized by single-target therapies, such as Humira, which targets TNF-α, and Cosentyx, which targets IL-17. These drugs respectively address multiple autoimmune indications, primarily rheumatoid arthritis and severe plaque psoriasis, dominating the market for over a decade. Now, with the continuous advancement in target research, this situation has been disrupted.

In the autoimmune field, more new targets such as IL-4R, TL1A, and BTK have emerged, even multi-target drugs like bispecific and multispecific antibodies. For instance, UCB's bimekizumab, approved in 2025, simultaneously inhibits two inflammatory pathways, IL-17A and IL-17F. In indications such as psoriasis and ankylosing spondylitis, its efficacy is significantly superior to single-target IL-17 monoclonal antibodies, making it a benchmark for multi-target drugs. In China, Simcere Pharmaceutical's TL1A/IL-23 bispecific antibody, Zai Lab's IL-13/IL-31R bispecific antibody, and Akeso Biopharma's IL-4Rα/ST2 bispecific antibody have all entered the critical clinical trial stage. Among these drugs with new targets and mechanisms, disruptive new drugs may also emerge. The immediate commercial success of bimekizumab upon its market launch serves as an excellent example.

The third is the shift in treatment thinking, from lifelong medication to functional cure. For a long time, most patients with autoimmune diseases have faced the dilemma of needing long-term medication. Traditional treatment methods can only control symptoms and are unable to fundamentally repair the disordered immune system. However, this situation is now being changed by cutting-edge biologic treatment technologies.

At the end of last year, Kyverna announced the Phase II clinical data of its CD19 CAR-T therapy for treating Stiff Person Syndrome (SPS). The results showed that among 26 patients who were unresponsive to traditional therapies, 81% experienced significant improvement in walking ability 16 weeks after a single infusion, 67% no longer required walking aids, and more importantly, 100% successfully discontinued immunosuppressants, with good safety observed. This therapy is planned to submit a marketing application in the first half of 2026 and is expected to become the world's first CAR-T therapy for autoimmune diseases. Additionally, explorations using STAR-T cell therapy for refractory systemic lupus erythematosus have also achieved long-term clinical remission in small-scale clinical studies.

The autoimmune market, which has seen frequent blockbuster drugs, is becoming a stage for small and beautiful new drugs. The former autoimmune kings that could dominate for decades might not appear again. For autoimmune patients, this is not necessarily a bad thing.