$15.725 Billion Four-Deal Spree! Gilead Sciences Not Content Being Just the HIV Leader

Gilead Sciences

Innovative Drug Developer, Distributor

Arcellx

Developer of Immunocyte Therapy

Ouro Medicines

Developer of Immune Reset Therapy

Tubulis

Developer of Drug Conjugates

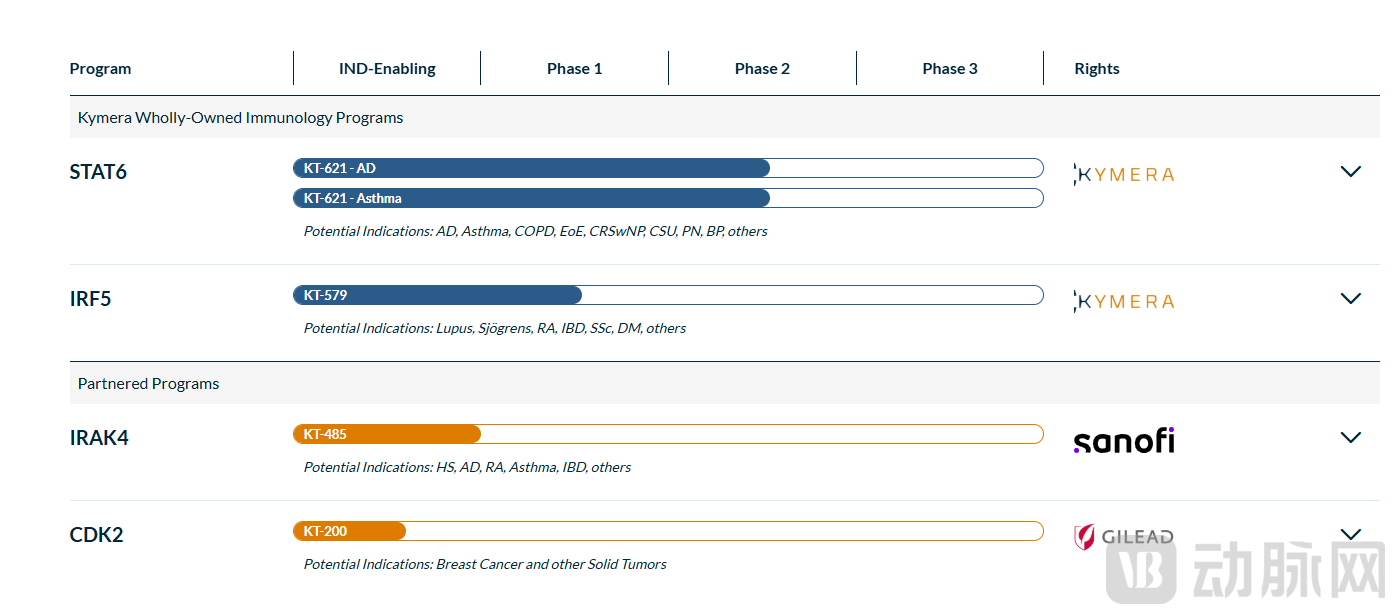

On April 9, Gilead Sciences exercised its exclusive license option to obtain global rights for the development, manufacturing, and commercialization of the first-in-class new drug KT-200, which will advance support.2027 New Drug Clinical Trial Application (IND)The clinical research phase.

As a result, Kymera, the original developer of KT-200, will obtain$45 Million Milestone PaymentAccording to the agreement reached in June 2025, Kymera is eligible to receive up to$750 Million Total Payment, including an upfront payment of 85 million US dollars and potential option exercise payments, in addition to tiered royalties on net product sales.

On the 100th day of 2026, Gilead Sciences has made four moves, with a potential total transaction value of approximately $15.725 billion:

On February 23, Arcellx, a CAR-T company, was acquired for $115 per share in cash and $5 per share in contingent value rights, with an implied equity value of approximately $7.8 billion.

On March 24, with an upfront payment of $1.675 billion, up to $500 million in milestone payments, for a total of $2.175 billion, Ouro Medicines, a Connexions NewCo partner company, was acquired to develop an innovative TCE (T-cell engager) bispecific antibody.

On April 7, a cash prepayment of $3.15 billion and milestone payments of up to $1.85 billion, totaling a consideration of up to $5 billion, were used to acquire Tubulis Technologies, a German next-generation ADC company.

Gilead Sciences remains highly ambitious in the oncology field.

1Acquisition of an Oral Molecular Glue Degrader: TPD Secures Two Deals in One Day

The transaction subject KT-200 was discovered and characterized by Kymera Therapeutics. It is aFirst-in-class, oral, targeted CDK2 molecular glue degrader。

CDK2-Targeted Molecular Glue Degraders Represent a Novel Therapeutic Strategy Designed to Selectively Eliminate CDK2, a Key Driver of Tumor Growth (as the binding partner of cyclin E, driving disease progression in cancers with cyclin E1 amplification and overexpression), Rather Than Merely Inhibiting Its Function While Preserving Other CDK Family Proteins. Traditional CDK2 Inhibitors Lack Specificity, Interfering with Closely Related Proteins and Causing Adverse Reactions.

CDK2Degradation agents have the potential to rely onCDK2 activity in cancers provides a more precise, safe, and effective oral treatment option, with the potential to significantly improve outcomes, including for those with limited treatment options.Patients with advanced breast cancerPrognosis.

In preclinical tests, KT-200 demonstrated low nanomolar degradation capability against CDK2, showed potent activity in CCNE1-amplified and overexpressed cell lines as well as in vivo tumor models, and exhibited significant brain penetration potential with good safety.

Kymera is committed to innovative research in the field of Targeted Protein Degradation (TPD) technology, addressing disease targets and pathological pathways that are difficult to reach with traditional therapies.AsThe world's first company to apply degraders in clinical treatment of immune diseasesKymera has built a pipeline matrix for the development of oral small molecule degraders, providing patients with a new generation of convenient and efficient treatment options.Its proprietary platform Pegasus™ integrates bioinformatics-driven target identification, an E3 ubiquitin ligase library, and predictive models, laying the foundation for the development of PROTACs and molecular glue degraders.

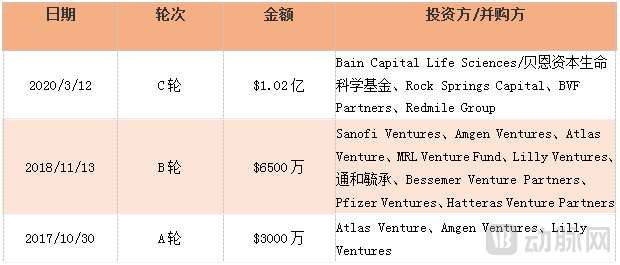

In August 2020, Kymera was listed on the NASDAQ in the United States, issuing 8.68 million shares at an issue price of 20 US dollars, raising 173.6 million US dollars.

Kymera Financing History

In June 2025 (concurrent with the Gilead transaction), Sanofi opted for Kymera's oral IRAK4 degrader KT-485/SAR447971 (for immune-inflammatory diseases) to enter clinical research, with a potential total deal value of $975 million. This agreement builds on the multi-project collaboration targeting IRAK4 initiated in July 2020.

In the细分赛道, Targeted Protein Degradation (TPD) leverages the body's natural ubiquitin-proteasome pathway (UPP) to degrade disease-causing target proteins. Since it was first proposed in 1999, research in this area has now entered its third decade. Kymera and its pipeline KT-200 represent a typical small-molecule approach within TPD — developing highly druggable, orally bioavailable molecular glues that target "undruggable" proteins.

Notably, TPD has not only become a hotspot for small-molecule drug development among major multinational corporations (MNCs), but also serves as a versatile and combinable toolbox to drive innovation in large-molecule pathways.

On April 9, Roche and another TPD leader, C4 Therapeutics, reached a collaboration with a $20 million upfront payment and a potential total value of over $1 billion to jointly advance the emerging research and development of Degradation Antibody Conjugates (DAC). DAC combines ADC and TPD.Combined with TPDSpecificity, catalytic efficiency, and the high-specificity recognition and delivery capability of ADCIn simple terms, this large-molecule drug approach combines the "magic bullet" PROTAC/molecular glue with the "precision guidance system" antibody, offering the potential to address key challenges in the development of small-molecule degraders, such as low in vivo delivery efficiency and significant off-target toxicity.

2Net profit increased by 1673% year-over-year in 2025.

The rush to lay out in the TPD track reflects the global competition among MNCs to "seize territories" — hoping to expand indications and asset types through pipeline BD and M&A, thereby diluting the value limitations brought by the patent cliff and single-domain labels.

Financial reports show that Gilead Sciences' total revenue for the full year 2025 reached $29.443 billion, a year-on-year increase of 2.4%; net profit attributable to shareholders was $8.51 billion, a significant year-on-year increase of approximately 1673%; diluted earnings per share under non-GAAP were $8.15, a substantial year-on-year increase of 77%.

Product sales revenue in 2025 reached $28.915 billion, representing a year-on-year increase of 1%.Excluding the COVID-19 drug Veklury (Remdesivir), product sales increased by 4% year-over-year.Profitability remains stable, with a product gross margin of 78.4%.

On one hand, the antiviral business that the company relies on for its growth continues to expand, with key products effectively offsetting the risks associated with the patent cliff.

In its core business, the HIV segment acted as a stabilizer with annual sales of approximately $20.8 billion, representing a 6% year-over-year increase, primarily driven by growing demand for HIV treatment and prevention. Among its products, Biktarvy achieved sales of $14.3 billion, marking a 7% year-over-year growth, further solidifying its market leadership. Additionally, Descovy's sales grew by 31% year-over-year to $2.8 billion.

In June 2025, Yeztugo (Lenacapavir), the world's first subcutaneous injection for HIV prevention administered twice a year, was approved for marketing. It addressed the adherence challenges in the PrEP (Pre-Exposure Prophylaxis) market and extended its HIV portfolio from "patient treatment" to "high-risk population prevention," forming a dual-driven model of "treatment + prevention." With less than half a year of commercialization, its sales reached $150 million.Management expects Yeztugo's sales to reach $800 million in 2026, with a long-term peak potentially exceeding $5 billion.

Hepatology Business Achieves $3.2 Billion in Annual Sales, a 6% Year-over-Year Increase,Mainly due to the continuous increase in demand for Livdelzi, a treatment for primary biliary cholangitis, as well as the growing demand for chronic hepatitis B virus (HBV) and chronic hepatitis D virus (HDV) products, but partially offset by the decline in the average selling price of chronic hepatitis C virus (HCV) products.

On the other hand, the oncology sector expanded through large-scale mergers and acquisitions generates stable revenue but has limited short-term growth.

Trodelvy sales reached approximately $1.4 billion, a year-over-year increase of 6%. The product originated from Gilead Sciences' $21 billion acquisition of Immunomedics, a leading next-generation ADC company, in 2020.

Cell therapy business sales derived from M&A amounted to 18.39.Billion USD, year-on-year-7%, and it is expected to continue declining by about 10% in 2026; Yescarta, the former star product in oncology, achieved sales of $1.495 billion, a year-on-year decline of approximately 5%.

Looking back at 2017, Gilead Sciences spent $11.9 billion to acquire Kite, obtainingYescarta, propelling it to the forefront of the global cell and gene therapy field. In 2022, its sales exceeded $1 billion for the first time, reaching $1.16 billion.

In 2026, in just six weeks, Gilead Sciences successively acquired CAR-T company Arcellx, Ouro Medicines with its TCE bispecific antibody, and Tubulis Technologies, a developer of next-generation ADCs. Coupled with this potential advancement in late-stage breast cancer.Indications for KT-200, Gilead Sciences' Chief Medical Officer Dietmar Berger stated, the current pipeline is"The richest and most diversified R&D pipeline in the company's history":

l Tubulis

TUB-040 is a NaPi2b-targeted topoisomerase I inhibitor (TOPO1i) ADC, currently in Phase Ib/II clinical trials for platinum-resistant ovarian cancer and non-small cell lung cancer (NSCLC).

TUB-030 is an ADC targeting 5T4, which has shown encouraging preliminary clinical data in multiple solid tumor types.

l Arcellx

The main candidate drug, anitocabtagene autoleucel (anito-cel), is a BCMA CAR-T cell therapy for patients with multiple myeloma.

l Ouro Medicines

The only product CM336/OM336 is an innovative TCE (T Cell Engager) bispecific antibody drug independently developed by Keymed Biosciences, with its active ingredient being a humanized BCMA/CD3 bispecific antibody. The clinical indications are for the treatment of autoimmune hemolytic anemia (AIHA) and primary immune thrombocytopenia (ITP), demonstrating potential best-in-class capabilities.

The underlying logic of anxiety is not only the patent cliff and performance expectations, but also —— MNCs with the world's top funding and clinical resources are simultaneously facing the most intense competition and iteration in cutting-edge therapies.