Ammunition's Second Filing with the Hong Kong Stock Exchange: Anchored by 5 Class III Certificates, the Early Screening Giant’s Breakthrough in the IPO Battle

Ammunition

Early Non-Invasive Testing Product Developer

On April 7, Wuhan Ammunition Life-tech Co., Ltd. ("Ammunition") submitted its second application for a main board listing on the Hong Kong Stock Exchange, with CCB International and BOCOM International remaining as the joint sponsors. This submission follows the expiration of the initial filing six months prior and represents a critical effort by a company that has been deeply engaged in early cancer screening for 11 years, now facing financial strain and fierce competition within the industry.

1No pan-cancer, no NGS

The starting point of the story is a laboratory in Wuhan's Optics Valley in 2015. At that time, the concept of liquid biopsy had just begun to emerge in China. Most companies were clustering around the technically advanced but costly NGS (Next-Generation Sequencing) route, attempting to seize the风口of pan-cancer screening.

But Zhang Lianglu, who had just graduated with a master's degree from Wuhan University (and later obtained a Ph.D. in Cell Biology from Wuhan University), made a counter-intuitive decision: to abandon the pan-cancer hype, focus on DNA methylation testing for high-incidence cancer types, and not complicate things with NGS, instead concentrating on the qPCR (Quantitative Real-time PCR) platform, which has the highest adoption rate in hospitals and the lowest cost.

What he aimed to create was an early screening product that "can enter hospitals, be covered by medical insurance, and be affordable for ordinary people." This decision allowed Ammunition to carve out a differentiated path amid the intense competition in the industry. The advancement of its product pipeline has demonstrated the vitality of this "pragmatic track."

In 2020, against the backdrop of no mature methylation products available in the field of early liver cancer screening, Ammunition decisively launched the development of its core product "Aixin Gan," focusing on addressing the clinical pain points of insufficient sensitivity and high missed diagnosis rates associated with traditional AFP testing.

In 2022, the colorectal cancer detection product "Aichangkang" successfully obtained Class III certification, becoming the company's first commercialized product and providing Ammunition with a stable source of revenue. By 2025, Ammunition will have a "big year" for obtaining certifications, securing three Class III certificates in one year, bringing the total to five, firmly ranking it as the leading enterprise in China’s methylation-based early screening market.

The confidence on the product side led Zhang Lianglu to decide to knock on the doors of the capital market. In September 2025, Ammunition filed its initial submission to the Hong Kong Stock Exchange (HKEX), aiming to leverage capital to accelerate commercialization. However, during the six-month hearing period, the Hang Seng TECH Index (18A sector) remained sluggish, with investors continuously voicing concerns over "small revenue scale and persistent losses."

Ammunition's Updated 2025 Financial Data in Second Filing Shines Brighter: Revenue Doubles, Gross Margin Soars, but Cash Reserve Pressure Remains Real. In Zhang Lianglu's View, Entering the Secondary Market is a Crucial Step for the Company at This Stage, Offering This 11-Year-Old Enterprise an Opportunity to Continue Developing "Practical Products."

25 Class III Certificates Build Barriers

Currently, Ammunition has developed more than 10 early cancer screening products, five of which have been approved as Class III medical devices in China, precisely covering four highly prevalent cancers: colorectal cancer, liver cancer, esophageal cancer, and cervical cancer. In this product launch, "Aixin Gan" and "Aiguang Le" have been positioned as the core pillars, becoming the key to Ammunition's differentiated competition.

First, let's look at "Aixin Gan." It is the world's first Class III medical device for early liver cancer screening based on qPCR technology, approved in January 2025. Clinical data shows that its overall sensitivity reaches 92.33%, with a sensitivity of up to 84.43% for early-stage (Stage I) liver cancer, significantly outperforming traditional AFP testing, which has relatively limited sensitivity for early-stage liver cancer. Currently, Aixin Gan has been successfully included in Beijing's Class A and Shanxi's Class B medical insurance directories, clearing a key payment barrier for commercial-scale adoption.

Next, let's look at "Aiguang Le." This product focuses on the early screening of urothelial carcinoma and is the first to use a new type of methylation biomarker for urothelial carcinoma screening. Only 1 milliliter of urine is needed for non-invasive testing, with a sensitivity of 92.94%, and a sensitivity of 85.45% for early Ta stage urothelial carcinoma. It effectively addresses the industry pain points of painful traditional cystoscopy and poor patient compliance – which often discourages patients and delays the optimal screening window. The product was approved in October 2025 and will also be the key factor for Ammunition’s revenue breakthrough in 2026.

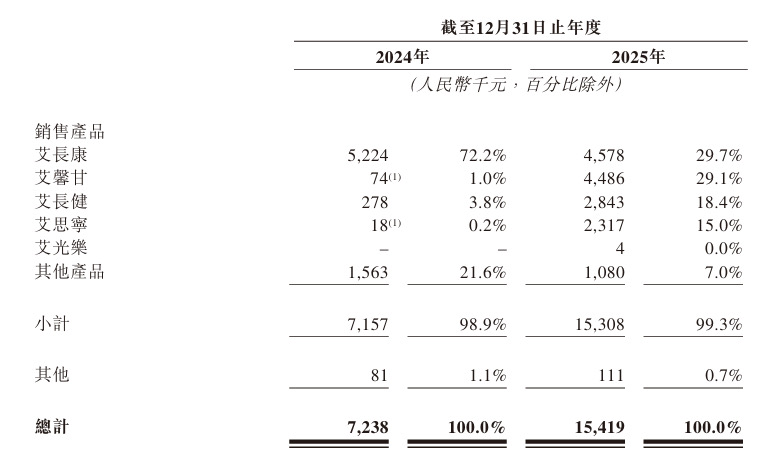

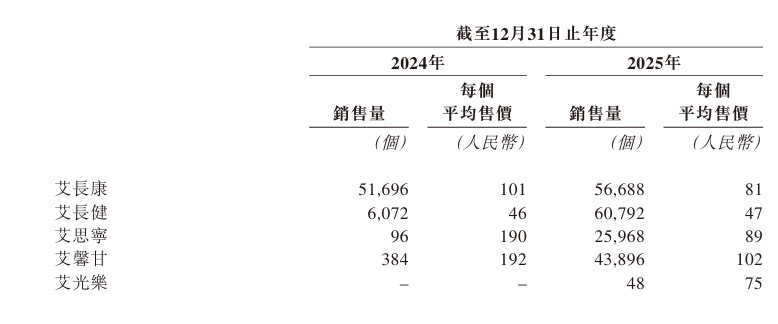

Currently, the company mainly sells five products. The earliest approved early-stage colorectal cancer screening product, Ammunition Changkang, accounted for 72% of the company's main revenue in 2024. As other products were successively launched in 2025, the company’s revenue scale doubled, and its revenue structure underwent significant changes. The revenue share of Ammunition Changkang dropped to 29.7%, while the revenue shares of Ammunition Changjian, Ammunition Sining, and Ammunition Xingan reached 18.4%, 15%, and 29.1%, respectively. Another core product, Ammunition Guangle, was approved at the end of 2025 and did not generate revenue during the reporting period; however, data is expected to improve further by 2026.

In terms of underlying technical support, Ammunition has its own "moat." The company possesses independently developed DNA Methylation Localization Technology (DMLT) and Sensitivity Enhanced Methylation PCR Technology (SEM-PCR). Among these, SEM-PCR technology can increase detection signal intensity by more than ten times. Even when facing target genes with concentrations as low as 1 copy/µL, it still achieves stable detection.

In terms of competitive strategy, Ammunition avoids the hype of pan-cancer screening and focuses on high-incidence cancer types, breaking through with the cost advantage of the qPCR approach. The price for single-person testing of its products is much lower than similar NGS products. According to the prospectus, the average selling price of several core products is less than or just around 100 yuan. Moreover, no special testing equipment needs to be added by hospitals—detection can be directly carried out using existing qPCR instruments, forming a unique advantage in the grassroots hospital market.

How large is the market space? According to data from Frost & Sullivan, the size of China's oncology molecular testing market has grown from 4.3 billion yuan in 2019 to 8.7 billion yuan in 2024, and is expected to reach 38.8 billion yuan by 2033, with a compound annual growth rate (CAGR) of 18.1%. Among this, the early screening market for liver cancer is experiencing the fastest growth: its market size was 197 million yuan in 2024 and is projected to increase to 3.249 billion yuan by 2033, with a CAGR as high as 36.6%.

But the competition in the track is equally fierce. In the field of early liver cancer screening, four companies have been approved for Class III certificates. In the field of early urothelial cancer screening, several companies are competing on the same stage, and in colorectal cancer early screening, dozens of companies are participating. Ammunition, with five certificates in hand, has already started on the path to commercialization.

3Revenue Soars After Second Filing

Compared to the first filing, in 2025, Ammunition's revenue reached 15.419 million yuan, a year-on-year increase of 113%. The gross profit margin jumped from 56.9% to 78.1%, with economies of scale gradually becoming apparent and product pricing power being validated.

Net loss widened from 38.63 million yuan to 48.979 million yuan. There are two reasons: R&D expenses increased to 21.297 million yuan, a year-on-year increase of 42%; administrative expenses rose to 20.05 million yuan, mainly due to IPO intermediary fees and share-based compensation of 17.61 million yuan – the latter being wages paid in equity instead of cash, which does not consume cash but "artificially" inflates losses on the accounting level. Excluding this non-cash expense, the operating loss for 2025 was approximately 31.38 million yuan, narrowing compared to 2024.

At the same time, the financial structure is being repaired. By the end of 2024, the company recorded negative assets of 21.596 million yuan due to a 272-million-yuan bet-related debt; in May 2025, after investors relinquished their preferential rights, the debt was converted into equity, turning the net asset value "positive" to 26.945 million yuan. The proportion of related-party transactions also declined simultaneously— in 2024, the largest client, "Wuhan AINUO Medical Laboratory" (wholly owned by founder Zhang Lianglu), contributed 52.1% of revenue; by 2025, this ratio had dropped to 17.2%.

Revenue Doubled, Gross Margin Improved, Balance Sheet Repaired, Related Party Transactions Converged — Financials Show Genuine Improvement, This Is Ammunition's Determination for Resubmitting Its Listing Application.

4What Does It Take to Run a Commercial Positive Cycle

Ammunition's core team is a typical "technology-oriented" group — with years of deep cultivation in methylation testing and leading the development of multiple core products. This team may not craft "exaggerated stories," but they can uphold the bottom line of "product supremacy."

The shareholder lineup also gives Ammunition confidence. Zhang Lianglu directly and indirectly controls approximately 50.64% of the company's voting rights, making him the controlling shareholder. Backed by industry capital such as Capricorn Bio and JC Zhongmin, this not only brings in funding but also channel resources, providing support for the grassroots implementation of products.

As of the submission date, the company has obtained 82 authorized patents, 59 of which are invention patents, and one is a U.S. patent, forming a strong technical protection barrier. In addition, the R&D pipeline covers gastric cancer, lung cancer, and multi-cancer joint testing, with a clear advancement pace. If successfully implemented, it will enrich the product portfolio and further expand revenue.

The technical school's foundation is solid enough, but the industry's dilemma is equally pressing. Can Ammunition establish a positive commercialization cycle within the cash reserve period? This is a question the company must answer.

5Ammunition's Three Key Questions

In this IPO, Ammunition plans to mainly use the funds raised for core product R&D and commercialization, production upgrades, pipeline expansion, and replenishing working capital. This is a necessary choice for it and also an inevitable path for all unprofitable early screening companies.

In the current Hong Kong Stock Exchange 18A market, investors place more emphasis on "commercialization capability" and "profit potential." The confidence of Ammunition lies in its products' ability to address clinical pain points and reach grassroots levels. However, its challenges are also clear – a still-low revenue base, the need for time to advance commercialization, and profitability that requires a longer cycle. Specifically, the success or failure of the second listing application hinges on three key issues:

First, can the five Class III certificates be quickly converted into sales? Although "Aixin Gan" has been included in the medical insurance systems of two regions, its nationwide promotion in China will require time and continuous investment.

Second, can the low-cost route of qPCR form a sustained advantage in the grassroots market? The cost advantage of this route is currently obvious, but the pace of technological iteration needs to be continuously monitored.

Third, can the model of high R&D investment achieve profitability improvement within the cash reserve period? According to the current growth rate estimation, breaking even will still take several years, during which stable financial support is required.

Ammunition's Journey: A Window into China's Early Screening Industry — After the Capital Retreat, the Industry Returns to Rationality; the Core of Early Screening is Solving Clinical Pain Points and Achieving Widespread Implementation. In Q2 2026, the Hong Kong Stock Exchange Listing Hearing Will Provide Answers. For this early screening giant, going public is not the end point but the starting point of commercialization. Survival and moving forward are the true challenges.