An innovative high-priced skin drug sells like hotcakes on e-commerce platforms in China

CMS

Professional Drug Developer

JD Health

Internet Medical and Health Service Platform Provider

Incyte

Small Molecule Drug Developer

A new breakthrough drug emerges in the dermatological market. The dermatology field has already produced a multi-billion-dollar autoimmune blockbuster, Dupilumab, and this high-potential market continues to yield lucrative opportunities.

In March 2026, the innovative dermatological drug Opzelura® (ruxolitinib phosphate cream) set a sales record for self-funded innovative drugs in China on its launch day, with over 5,000 units sold on JD Health. This drug, from CMS, is the first topical JAK inhibitor in China for the treatment of vitiligo, priced at 5,800 RMB/100g. Within one month of its launch, sales on JD Health alone exceeded 10,000 units.

Behind this blockbuster product lies a self-revolution of CSO (Contract Sales Organization) enterprises. In 2022, Dermavon Pharmaceuticals, a subsidiary of CMS, partnered with Incyte to secure the exclusive rights for the research, registration, and commercialization of Ruxolitinib Phosphate Cream in China and Southeast Asia. CMS has taken vitiligo as a breakthrough point, promoting the approval of Ruxolitinib Cream for use in patients aged 12 years and above with non-segmental vitiligo involving the face.

This model breaks the industry stereotype that CSOs only act as water sellers. CMS has started to "mine" upstream, leveraging capital and channels to extend into upstream innovative assets. The huge success of Ruxolitinib Phosphate Cream is the best testament to this transformation: high-quality innovative drugs supported by strong channel power can surpass expectations in terms of growth speed.

How did CMS uncover the blockbuster drug ruxolitinib? Going back to 2017, at that time, CSO companies primarily engaged in pharmaceutical agency businesses were impacted by the patent cliff of originator drugs, the consistency evaluation of generic drugs, and the pressure of price cuts from centralized procurement, leading to challenges in performance growth. Faced with this growth dilemma, CMS decided to undergo a comprehensive transformation.

In 2018, CMS announced that it would no longer engage in agency business in the future, but instead transition to a model of co-development profit-sharing or direct acquisition of drug assets, aiming to transform into an innovative pharmaceutical company. It also announced its transformation goal: to bring 10 significant innovative drugs to market in China in the future. In 2022, CMS selected Incyte as a partner and reached a collaboration with them, acquiring the rights to Ruxolitinib Cream (Opzelura™/Bai Lu Tuo®) in Greater China and Southeast Asia. Phosphate Ruxolitinib Cream is undoubtedly one of the 10 key products.

The success of Ruxolitinib Phosphate Cream as a blockbuster product is first and foremost a triumph in product selection. Ruxolitinib Phosphate Cream is a topical targeted JAK inhibitor. Its core mechanism of action revolves around inhibiting the JAK-STAT signaling pathway. By precisely blocking abnormal immune signal transmission, it reduces attacks on melanocytes and promotes their functional recovery, ultimately achieving repigmentation of vitiligo lesions. Ruxolitinib cream is effective in reducing the area of vitiligo lesions and restoring skin color, with good tolerability. As treatment time extends, the therapeutic effect will continue to improve.

In a Chinese real-world study, the F-VASI75 response rate (i.e., 75% improvement in facial vitiligo area or repigmentation) for Ruxolitinib Phosphate Cream at 24 weeks was 49.5%.

This product has also been recognized by the guidelines. According to the "Chinese Expert Consensus on Vitiligo Diagnosis and Treatment (2024 Edition)", systemic and topical corticosteroids, as well as JAK inhibitors, are listed as the first-line treatment options. Ruxolitinib is the first JAK inhibitor approved in China for the treatment of vitiligo.

Secondly, the success of CMS's differentiated indication layout. After selecting Ruxolitinib, CMS avoided the crowded atopic dermatitis indication and targeted vitiligo, a high-potential track. CMS has acted as a CSO for multiple dermatology drugs, which has given CMS an intuitive insight into the unmet needs of the vitiligo market.

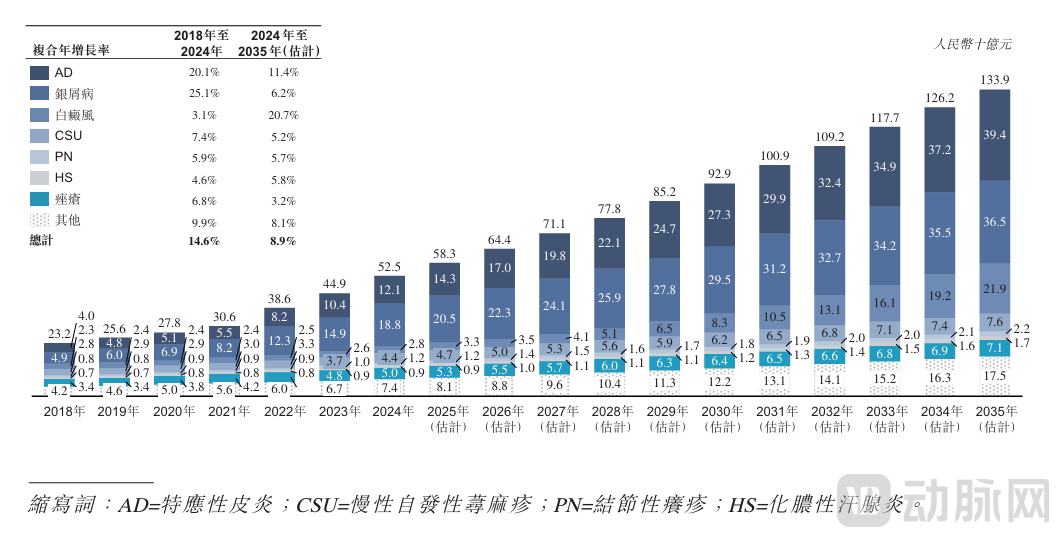

In terms of market size, the vitiligo market remains untapped. In China's secondary dermatology market, according to CIC data, the atopic dermatitis market size will reach 12.1 billion RMB in 2024; the psoriasis market size will reach 18.8 billion RMB; the chronic spontaneous urticaria (CSU) market size will be 4.4 billion RMB; the acne market size will reach 5 billion RMB; while the vitiligo market size in 2024 will only be 2.8 billion RMB.

China Dermatology Treatment Market Size Data Source:

Dermavon

The vitiligo market has a large patient population with urgent needs. Approximately 10 million people in China suffer from vitiligo, of which 8.2 million have non-segmental vitiligo, and the overall prevalence has been increasing in recent years. Vitiligo imposes a significant psychological burden on patients, with 75% experiencing anxiety, depression, and other related conditions, leading to an urgent demand for innovative therapies.

In terms of competition, compared to the fields of atopic dermatitis and psoriasis, which are dominated by mature giants such as Sanofi (Dupilumab) and Novartis (Secukinumab), the barrier to entry in the vitiligo market is lower. Previously, there were no drugs approved by the National Medical Products Administration (NMPA) in China for repigmentation treatment in vitiligo. Several traditional drug therapies have been used off-label. Conventional treatments for vitiligo have significant limitations, making precise repigmentation difficult, and patients have an urgent clinical need for new therapeutic options.

The low competition threshold in the vitiligo field also brings faster hospital admission speeds and greater pricing flexibility.

A senior executive of an innovative pharmaceutical company once stated that a differentiated indication layout also has more advantages in pricing. If the first-launch indication targets a large patient population with many participants, the pricing space for the product will be very narrow. At the same time, a differentiated indication positioning also has greater advantages in terms of market access and hospital entry, allowing for rapid expansion within hospital channels.

In-depth insights into the clinical needs of the large dermatology market, precise product selection, and differentiated indication layout have laid the foundation for the success of Ruxolitinib.

As a veteran CSO enterprise, CMS's strong channel control and operational capabilities were also key to the surge of Ruxolitinib. Its core operational actions can be broken down into three phases:

Before the market launch, preparations must be made in advance—taking the initiative to experiment and accumulate energy. Relying on the "Pilot First" policy in Boao Lecheng, Hainan, Ruxolitinib was able to be clinically applied in China before its official approval. This allowed for the early establishment of expert consensus, enabling more than ten thousand patients to receive the medication in advance. This move not only accumulated valuable real-world data locally but also fostered a strong reputation among patient groups by encouraging them to share their medication experiences and efficacy changes. It achieved the early-stage layout of popular science education and academic promotion. While other innovative drugs are still seeking patients after approval, Ruxolitinib has already been waiting for approval among the patients.

On the day of listing, leverage multi-channel operational capabilities for rapid coverage. The main sales channels for innovative dermatological products include hospitals, offline pharmacies, O2O e-commerce, and other diversified sales channels, requiring enterprises to build comprehensive and multi-level sales capabilities.

And dermatology is precisely CMS's strategic stronghold. CMS has spun off its dermatological health business to be independently operated by its subsidiary, Dermavon. In 2025, Dermavon has filed for listing on the Hong Kong Stock Exchange. Its pipeline targets the dermatological health giant, Galderma. Dermavon's revenue in the first half of 2025 was RMB 498 million. Dermavon's sales network covers over 12,000 hospitals nationwide, more than 150,000 offline retail pharmacies, and major e-commerce platforms.

With the channels fostered by CMS in the dermatology field over many years, Ruxolitinib was rapidly introduced into hospitals upon its launch: offline coverage extended to over 1,000 hospitals across 30 provincial administrative regions in China, and access was established through more than 1,300 retail pharmacies.

In online channels, CMS has also conducted in-depth operations in collaboration with JD Health, launching digital marketing tools such as "Early Bird Coupons," which effectively stimulated patients' purchasing intentions, promoted rapid sales conversion of products, and ultimately achieved explosive market performance immediately after the product launch.

Looking back at the innovative drugs that exploded upon Chinese market entry, the standardized actions for commercializing innovative drugs include pre-approval operations — rapid large-scale hospital entry — indication expansion — and improved medical insurance accessibility.

CMS has established a differentiated advantage in the vitiligo market, a segment with significant demand, and quickly formed dominant track power. However, the challenge has only just begun.

An industry insider stated, "In the innovative drug market for autoimmune skin diseases, accessibility is no longer the key threshold in the current competition for autoimmune drugs. The determining factor for whether a drug is a flash in the pan or a long-lasting blockbuster is whether patients can use it long-term. The key to CMS's competition in the dermatology field lies in ensuring that drug use goes beyond short-term symptom relief and truly alters the disease course."

In addition to CMS, other leading CSOs are also actively acquiring innovative assets. CSO companies are breaking the industry stereotype of "selling water but not mining." In the past, the role of CSOs was to help pharmaceutical companies sell drugs and earn sales commissions. However, CSOs are now extending upstream by investing in incubation, acquiring equity, locking in commercial rights, and other means to bind innovative assets in advance.

For example, Baheal Pharma, a leading domestic CSO, has diversified its investments through incubation, secondary market subscriptions, and commercial cooperation. It has laid out innovative drugs in the fields of osteoporosis, breast cancer, and tuberculosis, covering popular tracks such as RDC, PDC, and small nucleic acids. The most recent investment was 27 million RMB in SicaGene, a small nucleic acid track company, acquiring a 10% stake while securing global priority transfer rights and commercial priority negotiation rights for all of the latter's research pipelines. In the field of medical devices, Baheal Pharma has invested in Zap Medical, the parent company of ZAP Surgical Systems, Inc., a global leader in radiotherapy technology, as well as in China's artificial heart enterprise, BrioHealth.

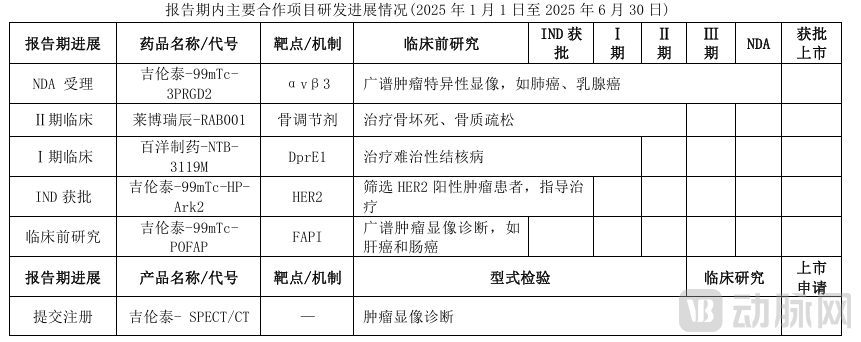

Progress of Baheal Pharma External Cooperation Projects (Innovative Nuclear Medicine Technetium-99mTc-Perritide Injection (99mTc-3PRGD2) Approved)

One of the four major CSOs in China, Edding Pharma, carried out a reverse acquisition of Genor Biopharma through a share exchange. Edding Pharma implemented a share swap merger with a valuation of $677 million against Genor Biopharma's $197 million valuation. After the merger, the focus will be on advancing pipelines such as GB268 (anti-PD-1/VEGF/CTLA-4, a trispecific antibody).

Mirroring the CSO buying spree, Biotech companies are also divesting their sales rights. Recently, Thederma Pharmaceuticals transferred the domestic sales rights of Benvitimod Cream to Jumpcan Pharmaceutical, in exchange for an upfront payment of 190 million RMB and milestone payments; Sciwind Biosciences entrusted the domestic commercialization rights of its core weight-loss drug ecnoglutide to Pfizer.

This shift is driven by two key logics: First, the revaluation of channel value. Companies like CMS, Baheal Pharma, and Edding possess mature hospital networks, academic promotion teams, and experience in gaining access to medical insurance. The value of these commercial infrastructures has been seriously underestimated in the era of an innovation drug boom. CSO enterprises are taking the initiative to use capital to lock in high-quality pipelines.

Second, the premium of certainty. Biotech is in urgent need of commercial certainty. The explosion of innovative drug products in China means that more competition in the future will focus on the commercialization field, and the key to competition lies in how to reach more people through a stronger sales team. Collaborating with companies that have established channels can secure commercial certainty at a lower cost and earlier stage, enhancing revenue expectations. On the other hand, it allows products to reach more patients faster, leveraging product synergy to quickly build competitiveness. In contrast, building an in-house sales team is costly and could potentially drain the cash flow for Biotech firms with a single pipeline.

This model has also been market-verified, and handing innovative products over to pharmaceutical companies with mature channels leads to faster market expansion. Qyuns Therapeutics, a leader in China's autoimmune sector, entrusted the sales of its first commercial product, Sailexin® (a biosimilar of ustekinumab), to Huadong Medicine. In its first year on the market in 2025, domestic sales in China are expected to reach nearly 300 million RMB, achieving rapid market penetration.

At present, China's biotech industry is in the rising phase, growing from weak to strong. Going it alone is unsustainable, and alliances and collaborations will become the norm. In the future, more innovative products will bridge the gap from approval to accessibility through this collaborative model, truly entering clinical practice.