Huayi Taikang's IPO on the Beijing Stock Exchange has been accepted, with high-end formulations + CDMO already generating nearly 100 million in profits.

Visum

High-end Oral Solid Dosage Form Developer

On March 31, 2026, Huayi Taikang Pharmaceutical officially submitted its IPO prospectus to the Beijing Stock Exchange. A Hainan-based pharmaceutical company, over sixteen years, has carved out a path to breakthrough in high-end formulations amidst the triple pressures of a fiercely competitive generic drug market, routine bulk procurement, and the high risks of innovation. What is little known is that this sprint did not begin at the Beijing Stock Exchange—Huayi Taikang initially planned to apply for the STAR Market but ultimately chose to shift to the Beijing Stock Exchange. This critical adjustment in strategy reflects the deep considerations of this SME in aligning with its own development pace and precisely connecting with the capital market.

While a large number of pharmaceutical companies in China are still fiercely competing in the low-price generic drug market, Huayi Taikang chose a more difficult, slower, but higher-barrier track from day one – complex formulations. Instead of opting for quick profits, it placed its bets on areas like controlled-release, extended-release, and poorly soluble drugs, which are challenging to research, difficult to get approved, and even harder to produce. Ultimately, it secured a place for Chinese pharmaceutical companies in the high-end market long dominated by international giants.

1A Group of Chinese Doctorates in the U.S. Betting on the Future of High-End Formulations Made in China

In 2010, Huayi Taikang was officially established in Haikou Pharm Valley, Hainan.

At that time, the landscape of China's pharmaceutical industry was clear: an oversupply of low-end generic drugs led to increasingly fierce price wars, while high-barrier, high-margin advanced complex formulations were almost firmly controlled by foreign enterprises. Controlled-release technology, pellet processes, solid dispersion platforms... these core capabilities that determine drug efficacy, stability, and bioavailability had long been difficult for domestic companies to breakthrough.

A group of Chinese pharmaceutical R&D doctors studying in the U.S. made a somewhat "rebellious" choice at the time: to abandon the quick and easy generic drugs and focus on complex and innovative formulations with high technical barriers. What they aimed to create were not just drugs that "could be marketed," but drugs that could "rival international standards."

Since day one, Huayi Taikang has set its sights on compliance with the dual GMP systems of China and the United States, simultaneously meeting the requirements of China's NMPA Good Manufacturing Practice (GMP) for pharmaceutical production and the more stringent U.S. FDA GMP standards. In 2013, the company's production facilities received certification under China’s revised GMP; in 2016,Once again, it passed the U.S. FDA certification with zero defects, becoming the first oral solid dosage pharmaceutical enterprise in Hainan to pass the FDA audit with zero defects.. This compliance certificate serves as both a quality baseline and a core credential and trust endorsement for the company’s future bids in China’s centralized procurement, international CDMO business, and overseas product registrations.

2Not engaging in price wars, but building barriers, focusing all efforts on R&D.

For a long time, Huayi Taikang appeared to be "out of place."

Many companies in the industry quickly initiate projects, rapidly file applications, and swiftly scale up, relying on scale and low prices to capture market share. However, Huayi Taikang has taken a different approach: nearly all cash flow is continuously invested in R&D, gradually building its own platform around core technologies such as pelletization, matrix tablets, bilayer tablets, solid dispersion, and functional coating.

Its logic is very clear:The endgame for ordinary generic drugs is a price war, while the endgame for complex formulations is technical barriers. Only by deepening and perfecting the technology can profit margins still be maintained when centralized procurement arrives.

After years of deep cultivation, the company has formed a dual-driven model of commercializing self-developed products and CDMO customized R&D and production. Self-developed products focus on essential large fields such as cardiovascular and pediatric medications; CDMO, relying on FDA and China GMP dual-certified capacity, provides one-stop services for domestic and international enterprises from R&D, registration to commercial production. One internal, one external, one stable, one growing, forming its unique risk-resistant structure.

3Centralized procurement is not a winter: For companies with barriers, it becomes an accelerator for growth.

In February 2026, Huayi Taikang reached a critical milestone as its core product, Metoprolol Succinate Extended-Release Tablets, was selected for the continuation of the national procurement agreement, with the procurement cycle extending until the end of 2028.

In the industry's general perception, centralized procurement means price cuts, profit compression, and survival pressures. However, for high-end formulation companies like Huayi Taikang, centralized procurement is more like a "compliant ticket to scaled entry." With stable quality, mature technology, and controllable costs, the company exchanges price for volume, rapidly expanding its presence in the public hospital market and gradually converting shares originally dominated by foreign enterprises into its own solid base.

After the centralized procurement was implemented, the certainty of product sales increased significantly. Large distribution enterprises such as Jiuzhou Tong, Sinopharm Holding, and Chongqing Pharmaceutical became stable partners, and their performance also welcomed a turning point.

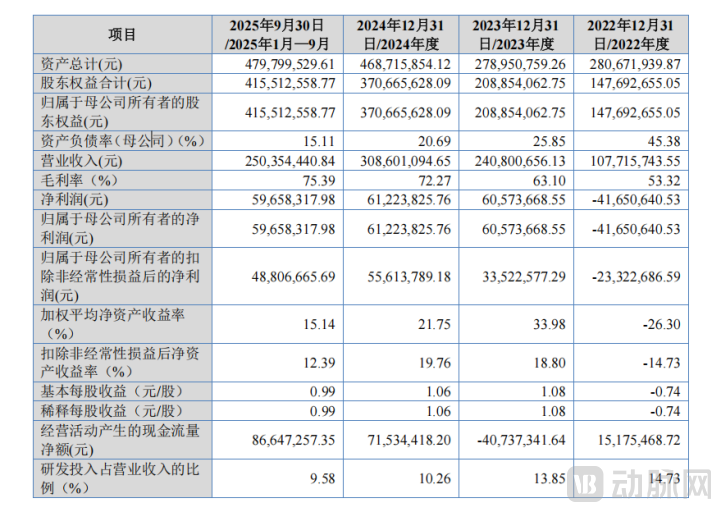

The financial data in the prospectus serves as the best footnote to Huayi Taikang's strategic choices. In 2022, the company was still in the critical period of R&D investment and market expansion, with revenue of 108 million yuan and a negative net profit attributable to parent company. In 2023, with the increase in core product output and the rise in CDMO orders, revenue surged to 241 million yuan, a year-on-year increase of 122.84%, turning losses into profits, with a net profit attributable to parent company reaching 60.5737 million yuan.

In 2024, the business entered a steady growth phase, with revenue reaching 309 million yuan and profitability continuing to be maintained. In the first three quarters of 2025, revenue reached 250 million yuan, with a net profit of 59.6583 million yuan, approaching the level of the entire previous year. Operating cash flow remained positive for two consecutive years.

Source: Huayi Taikang Prospectus

This is a typical "bitter first, sweet later" curve:High R&D investment and low profit in the early stage; product breakthrough and order surge in the mid-term; scale effect becomes evident and profitability continues to improve in the later stage.Supporting all of this are the high profit margins brought by advanced formulations, the cash flow generated by CDMO operations, and the stable sales volume ensured by centralized procurement.

4Strengthening the fundamentals in China, expanding new horizons overseas

Huayi Taikang has not tied its fate to a single market or a single business.

In China, it enters tertiary hospitals and primary healthcare with high-end formulation products, and the volume procurement products provide a stable cash flow;

Overseas, it relies on the production system capacity certified by the FDA to undertake CDMO orders, and has reached cooperation with overseas enterprises such as Oryza Pharmaceuticals, exporting China's high-end formulation capabilities globally.

In terms of production capacity, the company has long completed the layout of "dual R&D centers + dual manufacturing bases." The Haikou Pharmaceutical Valley Manufacturing Center has an annual production capacity of 3 billion tablets, and the Meian Manufacturing Center has an annual production capacity of over 10 billion tablets, which can simultaneously support the scaling up of self-developed products and the growth of CDMO orders.

5From STAR Market to Beijing Stock Exchange, a rational choice in line with the growth rhythm

Huayi Taikang's current push for the Beijing Stock Exchange (BSE) was not part of its original IPO plan — the company had initially intended to apply for the STAR Market but ultimately decided to shift towards the BSE. This adjustment was based on multiple rational considerations, including the company’s stage of development, industry characteristics, and capital market positioning.As a specialized and innovative small and medium-sized enterprise focusing on complex formulations, Huayi Taikang's growth trajectory is highly aligned with the positioning of the Beijing Stock Exchange (BSE) to "serve innovative small and medium-sized enterprises and support specialized and sophisticated enterprises." This alignment has become the core logic behind its adjustment of the listing path.

Compared with the STAR Market, the listing threshold of the Beijing Stock Exchange (BSE) is more in line with Huayi Taikang's current development scale, and the review process is more efficient. From acceptance to listing, the average time taken by the BSE is shorter than that of the STAR Market, enabling companies to secure financing support more quickly to meet their urgent needs for capacity expansion and R&D investment. More importantly, the listing criteria launched by the BSE for innovative small and medium-sized enterprises are more inclusive, especially for pharmaceutical companies that focus on niche markets, possess core technologies, but have not yet reached the scale of leading companies on the STAR Market. These companies do not need to excessively pursue size and can instead concentrate on core technology and main business development.

For Huayitai Kang, listing on the Beijing Stock Exchange (BSE) not only achieves financing goals but also leverages BSE's support policies for specialized and innovative enterprises to further strengthen brand influence, attract high-quality resource alignment, and pave the way for subsequent development. Additionally, the company was listed on the NEEQ in December 2024, completing the preliminary preparations required for BSE listing, which also provides a natural path advantage and compliance foundation for its transition to the BSE.

In contrast, the Sci-Tech Innovation Board focuses more on "hard technology" attributes and scaled-up enterprises. It demands higher R&D investment from companies, larger-scale transformation of innovative achievements, and features fiercer competition, primarily targeting innovative pharmaceutical companies that have already achieved significant scale.

For Huayitai Kang, the shift to the Beijing Stock Exchange (BSE) does not mean giving up innovation. Instead, it represents a choice of a capital market path that better aligns with its growth pace—first leveraging the financing and support from the BSE to strengthen its R&D and production capacity foundation. Once scale and innovative achievements have further breakthroughs, it can then seek higher-level capital market development. This is both a pragmatic choice and a consideration for long-term strategic planning.

In this push to go public on the Beijing Stock Exchange, Huayi Taikang plans to raise 3 billion yuan. The funding will be highly focused, with no cross-industry activities. Of the total, 2.7 billion yuan will be used for the construction of an intelligent manufacturing base: expanding high-end solid formulation production capacity, enhancing automation and intelligence levels, and alleviating capacity bottlenecks; 30 million yuan will be allocated for the construction of an innovation research and development center: upgrading equipment, attracting talent, and strengthening efforts in complex formulations and innovative formulations.

Simple and straightforward: expand production capacity, strengthen R&D. Utilize the power of the capital market to widen and heighten the existing technological advantages, GMP compliance advantages, and large-scale manufacturing advantages.

6China's high-end formulations are moving from "being able to produce" towards "becoming stronger"

Standing at the new starting point of its IPO, Huayi Taikang still faces common challenges in the industry: potential price pressures from the ongoing centralized procurement policy, intensifying competition in high-end sectors, balancing R&D investment with output, and uncertainties in overseas expansion. The adjustment of its listing path also presents new tests—how to leverage the platform of the Beijing Stock Exchange (BSE) for rapid development, and how to further expand scale and enhance innovation capabilities while maintaining its advantages in niche markets.

But its story has proven that Chinese pharmaceutical companies do not have to follow the old path of low-cost generic drugs. On the long and snow-thick track of complex formulations and high-end formulations, adhering to technology, quality, and internationalization can still lead to a sustainable growth path. The adjustment from the STAR Market to the Beijing Stock Exchange also reflects the pragmatism and clarity of this company – not blindly pursuing a "high positioning," but choosing the most suitable development pace, steadily moving forward with the support of the capital market.

From Hainan Pharmaceutical Valley to Beijing Stock Exchange, from loss to profit, from STAR Market planning to Beijing Stock Exchange sprint, Huayi Taikang has provided an answer in 16 years:The real barriers are never price, but technology and time; true growth is never blind following, but rational decision-making and long-term dedication.

Its IPO is just the beginning. In the future, can it continue to make breakthroughs in the high-end formulation sector? Can it gain a larger share in the international market? Can it find a better balance between innovative drugs and generic drugs? And how will the choice to shift to the Beijing Stock Exchange this time bring new development opportunities?

The answer will be written in every approved product, every order, and every technological iteration.