Risk of Death Reduced by 57%! This Company Secures First-Line Treatment for Entire Ovarian Cancer Population Through "Synthetic Lethality," Makes Second Push for Hong Kong IPO

On March 27, 2026, Nanjing Impella Pharma Co., Ltd. submitted an updated listing application to the Main Board of the Hong Kong Stock Exchange, with Goldman Sachs and CICC as joint sponsors. This follows the expiration of the company’s initial filing on September 26, 2025, marking its renewed push for a Hong Kong IPO. Founded in 2009, this biotechnology company, specializing in synthetic lethality precision oncology, is now making another attempt to enter the Hong Kong capital market, backed by the commercial performance of its first marketed product, Senaparib, and a robust R&D pipeline covering all key targets.

At the critical juncture where the global PARP inhibitor market transitions from fierce competition to the next generation of technological iteration, Impella Pharma's IPO this time not only marks a significant debut for China-produced innovative drugs in the synthetic lethality precision oncology track, but also serves as a real-life survival sample of a biotech company moving from clinical trials to commercialization.

116 Years Dedicated to One Thing: China's Commitment to the Synthetic Lethality Track

The starting point of Impella Pharma was rooted in the firm belief in the cutting-edge anticancer mechanism of synthetic lethality. In 2009, when the company was founded, China's innovative drug sector was still dominated by generic drugs and fast-follow strategies. However, the team set its sights on the core track of synthetic lethality, choosing PARP as the central target to build a research and development system. Focusing on the original research and innovative breakthroughs of small-molecule precision anticancer drugs, at that time, the world’s first PARP inhibitor was still in the preclinical stage, years away from validating its commercial value. Choosing to deeply cultivate "synthetic lethality" at this juncture was undoubtedly a bold gamble. Yet, it was precisely this decision that allowed the company to avoid the then-crowded target tracks, while also setting the stage for long-term high R&D investment and slow returns.

In 2012, the team selected Senaparib (IMP4297) as the core PARP inhibitor to advance, dedicating the next five years to preclinical research and CMC development; in 2019, the two pivotal clinical trials FLAMES and SABRINA were initiated; in 2023, entering a period of intensive harvest, the Phase III clinical trial FLAMES for Senaparib used in first-line maintenance treatment for the full population with advanced ovarian cancer met its primary endpoint; the NDA for first-line maintenance treatment of advanced ovarian cancer was accepted by the NMPA.In January 2025, Senaparib was approved by the NMPA for marketing in China, indicated for first-line maintenance treatment in the full population of ovarian cancer patients. It has become the third PARP inhibitor approved for this indication in China., and was included in the national medical insurance catalog in December of the same year. Reimbursement will be officially implemented starting from January 2026.

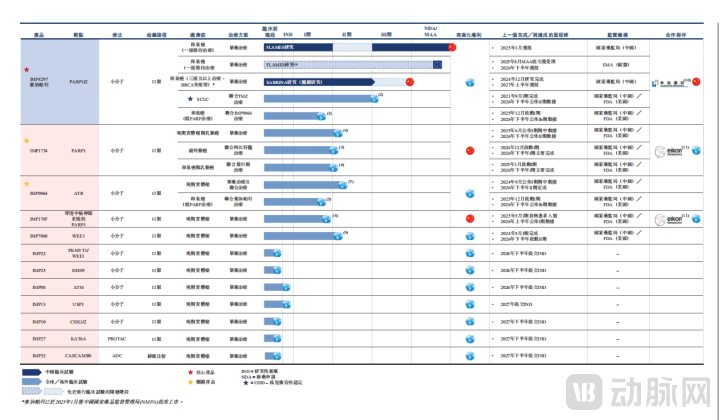

From preclinical to commercialization, Impella has completed the full-cycle development of an original anticancer drug in 16 years. As of the date of the prospectus disclosure, Impella has built a synthetic lethality pipeline consisting of 1 commercialized product, 4 clinical-stage candidates, and 7 preclinical candidates, covering key targets such as PARP1/2, PARP1, ATR, WEE1, and PKMYT1. At the same time, it has laid out emerging technology platforms such as ADC and PROTAC, constructing one of the most comprehensive and advanced synthetic lethality portfolios in China and even globally. This also marks Impella as one of only three companies worldwide to simultaneously possess a commercial-stage PARP1/2 inhibitor and a clinical-stage next-generation PARP1 selective inhibitor.

Source: Impulse Therapeutics Prospectus

In terms of equity structure, the investor matrix includes LAV, Lilly Asia Ventures, Decheng Capital, WuXi AppTec, Tencent, etc., with the LAV entity controlled by Dr. Yi Shi as the largest shareholder, holding approximately 15.62%.

2Core Product Senaparib: 57% Reduction in Disease Progression Risk, Launched in 30 Provinces Across China

As the company's only commercialized product, Senaparib is the cornerstone of IMPACT Therapeutics and its core weapon against market competition.

This self-developed PARP1/2 inhibitor offers the greatest clinical value through its differentiated advantages confirmed in the FLAMES study: as a first-line maintenance treatment for advanced ovarian cancer, it unprecedentedly reduces the risk of disease progression or death compared to placebo, regardless of BRCA mutation status, with consistent benefits observed across homologous recombination subgroups. Compared to placebo,Cynaparib reduces the risk of disease progression or death by 57%, representing an ideal outcome for progression-free survival in the "entire population" of ovarian cancer patients undergoing first-line maintenance treatment with a Chinese PARP1/2 inhibitor, setting a new benchmark in this category.Moreover, a significant progression-free survival benefit of cenersen over placebo was observed in the subgroup of ovarian cancer patients with BRCA mutations, as well as in the BRCA wild-type subgroup and subgroups defined by homologous recombination status.

At the commercialization implementation level, Impa chose to cooperate with East China Medicine's subsidiary, Sinopharm East China, leveraging the latter's sales network to quickly cover the market; as of December 2025, Senaparib has been launched in 30 provinces in China, and the implementation of medical insurance will further improve patient accessibility.

At the same time, Impa advances its global layout. In August 2025, the European marketing authorization application for Senaparib was accepted by EMA, with an expected approval in the second half of 2026. Clinical trials for indications such as combination therapy for small cell lung cancer and monotherapy for later-line ovarian cancer are continuously progressing, further extending the product lifecycle.

In terms of intellectual property, Impulse has built a stringent patent barrier for Senaparib, owning 5 authorized Chinese patents, 8 U.S. patents, 13 patents in other regions, and 38 pending patent applications across China, the United States, and other jurisdictions. These patents cover compounds, crystal forms, preparation methods, and indications, providing long-term protection for product commercialization.

3Under the "3+3" Pattern of PARP Inhibitors: The Breakthrough and Iteration of China-Produced Forces

The global PARP inhibitor market has now entered a phase of both stock competition and technological iteration. The Chinese market, in particular, exhibits a dual-track structure of "imported originals + local innovation," with competition intensity continuously increasing.

According to the prospectus, six PARP inhibitors have been successfully launched in China, forming a clear "3+3" competitive landscape: the imported original research camp consists of AstraZeneca/Merck's Olaparib, GSK/Zai Lab's Niraparib, and Pfizer's Talazoparib; the local innovation camp includes IMPACT Therapeutics' Senaparib, Hengrui Medicine's Fluzoparib, and BeiGene's Pamiparib.

In this competition, the concentration of market share is extremely high. Data from 2024 shows that over 50% of the market share in China is occupied by AstraZeneca/Merck's Olaparib, followed closely by Niraparib, Talazoparib, and others, forming a preliminary situation of "one superpower and multiple strong contenders." As the core of the track, first-line maintenance treatment for the entire ovarian cancer population is a key battleground determining market share ownership. Currently, only three products—Niraparib, Fluzoparib, and Senaparib—are approved for this indication. Yingpai’s Senaparib, with this crucial entry ticket, has secured its place in the first tier of Chinese-produced drugs.

Specifically, Olaparib, the world's first marketed drug of its kind, leveraged its first-mover advantage to achieve nearly 2 billion yuan in sales in the Chinese market in 2024, accounting for approximately 54%. However, its failure to win the centralized procurement bid in 2025 put its market share under pressure. Zai Lab's Niraparib, with the convenience of once-daily dosing and broad population indication coverage, achieved sales of about 1.46 billion yuan in 2024, capturing roughly 40% of the market share. Hengrui Medicine's Fluzoparib, relying on strong sales channels, quickly gained traction, occupying about 5% of the market share in 2024. Meanwhile, IMPACT Therapeutics' Senaparib...Having gained the support of medical insurance policies and leveraging its differentiated safety advantages to overtake competitors, it quickly entered the core market right after its launch in 2025. It successfully became the third "first-line full-population" ticket produced in China, setting the stage for subsequent market share competition.

The hematological toxicity of traditional PARP1/2 inhibitors is a clinical pain point, and PARP1 selective inhibitors have become the next-generation breakthrough direction. IMP1734, developed by Inpac, is 648 times more selective for PARP1 over PARP2, indicating significantly lower hematological toxicity, higher safety, greater drug exposure, and extensive potential for combination with other anti-tumor drugs. It is currently in global Phase I/II clinical trials, ranking in the first tier alongside AstraZeneca's AZD5305 and Hengrui's HRS-1167, representing the company’s future second growth curve.

Meanwhile, IMP9064 is the first ATR inhibitor in China to enter clinical trials, and IMP7068 is a WEE1 inhibitor. Both are developed based on the synthetic lethality mechanism, showing potential for combination with Senaparib and building a "synergistic" pipeline barrier.

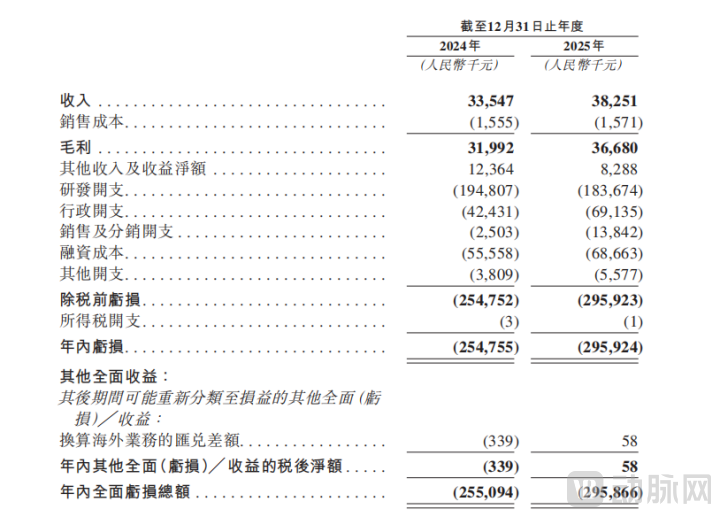

4R&D accounts for over 68%, with 259 million in cash reserves supporting the critical period of commercial scaling.

As an innovative drug company in the early stage of commercialization, Impulse Therapeutics exhibits typical financial characteristics of high R&D investment, stable revenue, and phased losses.

Source: Impulse Therapeutics Prospectus

From the financial data, R&D investment is the company's largest expenditure. In 2024, the company's R&D spending reached 195 million yuan, and in 2025 it was 184 million yuan. The scale of R&D investment over the two years remained basically stable. The core reason for the slight decrease is that Senaparib has completed its core clinical studies and entered the post-marketing clinical closing stage, leading to a reduction in related R&D investment. Meanwhile, funding has shifted focus to advancing the development of pipeline products in clinical stages such as IMP1734 (PARP1 selective inhibitor) and IMP9064 (ATR inhibitor), ensuring continuous iteration of the product pipeline. In terms of proportion, R&D expenses accounted for 81.3% and 68.9% of operating expenses in 2024-2025 respectively. Even in 2025, with the launch of Senaparib and an increase in sales expenses and other operating costs, the proportion of R&D investment still remained above 65%, far exceeding the industry average.

At the cash flow level, as a biotech company in the early stage of commercialization, the company's operating cash flow shows a phased negative growth trend, which is highly consistent with the operating cash flow data disclosed in the financial statements: -81.311 million yuan in 2024 and -95.880 million yuan in 2025. The slight year-on-year expansion of cash outflow is primarily due to the company being in a critical period of commercial investment. On one hand, it needs to continuously invest R&D funds to support pipeline advancement; on the other hand, it must build a sales team and expand market channels. Additionally, non-operating expenses such as share-based payments and financing costs have increased. However, the company’s core product, Cenapli, will not officially launch until January 2025, and its annual sales revenue has yet to reach scale, making it unable to cover the dual investments in R&D and commercialization. This is a typical characteristic of innovative drug companies transitioning from the clinical stage to the commercialization phase.

From the perspective of capital reserves, by the end of 2025, the company's cash and cash equivalents amount to 259 million yuan. Combined with the fundraising plan for this Hong Kong IPO, the proceeds will further replenish the company’s working capital, which is expected to support R&D investment and commercial expansion over the next 2-3 years, effectively alleviating cash flow pressures. It should be noted that although the current operating cash flow is negative, the company has no interest-bearing debt, maintaining an overall robust capital chain. Moreover, as patient accessibility improves following the inclusion of Sinopharm in the medical insurance system, sales volume gradually increases, and subsequent new indications are developed, the future operating cash flow is expected to improve progressively, enabling a transition from losses to profitability.

5Three Tough Battles After IPO: Market, Pipeline, and Globalization Implementation

Impulse Therapeutics' IPO taps into three major industry opportunities: First, synthetic lethality has become the golden track in precision oncology treatment, with transaction activity in the sector continuing to rise. Second, the acceleration of China-produced PARP inhibitors is driven by both medical insurance and clinical guidelines. Third, the company possesses a complete closed loop of commercialized products, a differentiated pipeline, and global clinical trials, which offers a certain level of scarcity.

At the same time, the company also faces common challenges in the industry: fierce market competition for PARP inhibitors, with price pressures brought by centralized procurement and medical insurance cost control; long clinical development cycles, large investments, and uncertain results for innovative drugs; and the ongoing test of continuous operating ability due to initial commercialization losses and cash flow management.

For Innovent, the Hong Kong IPO is not the end point, but the starting line for three tough battles: the market share competition for Senaparib, the clinical realization of next-generation products like IMP1734, and the pace of global commercialization. On the long and snow-covered track of synthetic lethality, whether this China-based biotech company, which insists on original innovation, can grow from a clinical player into a commercial winner with its differentiated products and full industrial chain layout will be the core focus of the industry in the next two years.