2026’s hottest drug asset: with limited clinical data, are pan-KRAS inhibitors overheated?

AstraZeneca

Pharmaceutical Technology Research and Development Provider

Pan-KRAS inhibitors are arguably the most sought-after innovative drug assets in 2026. Deal valuations for clinical-stage pipelines continue to rise, and even quantum computing is being used to screen new drugs. It is no exaggeration to describe pan-KRAS inhibitors as red-hot.

The reason behind this is that the world's first pan-KRAS formulation is poised to enter the market in 2026. According to plan, Revolution Medicines' pan-KRAS inhibitor RMC-6236 will complete the critical sprint of its Phase III clinical trial for the first indication in 2026, stirring up the vast market for KRAS-mutant tumors.

Thus, in early 2026, news of MSD's potential acquisition of Revolution became the hottest topic in the global pharmaceutical industry. Slightly earlier, AbbVie had also been rumored to be considering an acquisition of Revolution. As a result, the multinational pharmaceutical companies' concerted push into pan-KRAS inhibitors began to emerge. Although AbbVie ultimately denied the rumor, and MSD walked away due to the high price tag of approximately US$30 billion, earlier, AstraZeneca had paid a rare high price—over US$2 billion in total—for an early-stage pan-KRAS inhibitor from Jacobio Pharma. Pfizer and Lilly also completed their own early-stage positioning. Additionally, driven by acquisition rumors, Adlai Nortye, a rare clinical-stage pan-KRAS player in the U.S. stock market, saw its share price quadruple within eight days during this period.

However, to what extent can pan-KRAS inhibitors, which have shown slow clinical progress, solve the KRAS-targeted drug development challenge that has plagued the pharmaceutical industry for decades? Given the limited clinical data available, are pan-KRAS inhibitors overheated? These questions are worth considering.

A Blockbuster Drug with an Uncertain Future

To date, the development of KRAS-targeted drugs has not been considered a success.

This is primarily due to the fact that KRAS is a difficult target to drug. The surface of the KRAS protein offers almost no binding sites for drugs, and most early inhibitors also disrupted healthy KRAS. The KRAS protein is present in all human cells and plays a key role in regulating pathways that control cell growth and survival. When it mutates, it can drive cells into a state of uncontrolled proliferation, a key driver of cancer growth. KRAS gene mutations act like an accelerator for tumors, making even initially indolent tumors difficult to control. Approximately 80 percent of pancreatic cancer patients, 40 percent of colorectal cancer patients, and 35 percent of non-small cell lung cancer patients harbor KRAS gene mutations, making KRAS one of the most common oncogenic mutations in solid tumors.

Previously, multinational pharmaceutical companies spent nearly a decade developing the world's first KRAS-targeted drug. In 2013, scientists at Amgen hypothesized whether a drug could be designed to develop KRAS inhibitors, and the following year, the company entered into a research collaboration and worldwide exclusive license agreement with Carmot, formally committing to the development of small molecule inhibitors targeting the KRAS G12C mutation. In 2021, sotorasib, developed primarily by Amgen, received FDA approval for the treatment of adult patients with locally advanced or metastatic non-small cell lung cancer harboring the KRAS G12C mutation, becoming the world's first KRAS inhibitor. The following year, adagrasib, developed by Mirati Therapeutics, was approved, becoming the second approved KRAS G12C inhibitor.

The approval of these two blockbuster drugs sparked a global wave of development for this class of inhibitors. Soon, the first major merger and acquisition deal in the KRAS space emerged. In January 2024, Bristol Myers Squibb outbid Sanofi to acquire Mirati for US$4.8 billion, gaining adagrasib and next-generation pipeline assets such as G12D. Behind this deal was an early, quiet competition among multinational pharmaceutical companies for KRAS pipelines. Initially, Bristol Myers Squibb had offered nearly US$10 billion. In October 2023, Bloomberg reported that Sanofi was exploring an acquisition of Mirati. Additionally, it is speculated that two other multinational pharmaceutical companies were in contact with Mirati during this period. Before the deal was reached, Mirati had been on the market for a year and a half, engaging in 14 formal negotiation rounds with Bristol Myers Squibb.

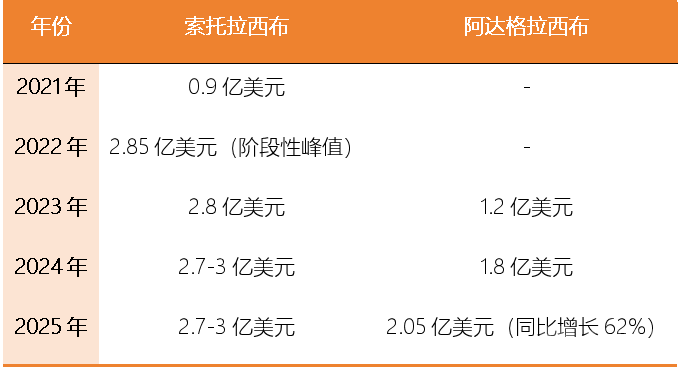

However, the commercial performance of these two drugs has been underwhelming. According to financial reports from Amgen and Bristol Myers Squibb, since its launch in 2021, sotorasib's annual global sales have remained around US$200 million to US$300 million. Adagrasib, launched in 2023, has seen slow global sales growth, with sales of US$120 million, US$180 million, and US$205 million respectively, far below market expectations of a US$1 billion peak sales forecast for these two new drugs.

Commercial Performance of Sotorasib and Adagrasib Data Source: Financial Reports of Various Companies

Consequently, both Amgen and Bristol Myers Squibb quickly began to retreat. In its 2025 financial report, Amgen explicitly removed sotorasib from its list of core growth pillar products. Although sotorasib remains an important cornerstone of Amgen's oncology pipeline, the company is no longer pursuing aggressive expansion. Currently, Amgen has largely abandoned large-scale independent development of sotorasib in other KRAS G12C-mutant solid tumors such as pancreatic cancer and biliary tract cancer, conducting only limited exploration through collaborations or external data. Additionally, in markets outside the United States, Amgen has adopted a more conservative approach to commercializing sotorasib. In the third quarter of 2025, Bristol Myers Squibb announced the termination of the co-development of its SOS1 inhibitor MRTX0902 with adagrasib, which had been the most important early combination development pathway for adagrasib. Furthermore, Bristol Myers Squibb is no longer broadly advancing early pan-tumor exploration or multiple combination trials for adagrasib.

At the same time, the once-fevered development of KRAS G12C inhibitors has been slowed. The most representative example came in June 2024, when Novartis announced it would completely terminate the development of its KRAS G12C inhibitor JDQ443, which had already entered Phase III clinical trials, and fully exit the KRAS G12C space. By the end of 2025, Verastem Oncology also terminated the RAMP 203 Phase I/II trial conducted in collaboration with Amgen, fully exiting G12C combination development. Betta Pharmaceuticals terminated early clinical development of its KRAS G12C inhibitor BPI-421286, completely exiting G12C to focus on other targets. In 2025, AstraZeneca, while terminating development of its KRAS G12D inhibitor pipeline AZD0022, also scaled back its G12C-related exploration. In addition, multiple small biotechnology companies terminated early-stage G12C programs and exited the competition.

However, this wave of high-profile failures has not halted the pharmaceutical industry's pursuit of new KRAS-targeted drugs. More bold attempts are being applied to exploration in this field.

Quantum Computing and Rare High Prices

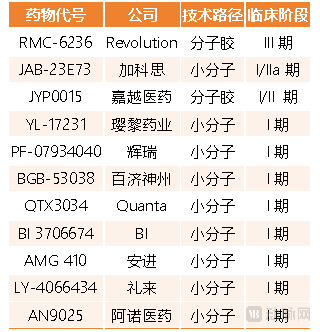

An important reason for the lackluster sales of KRAS G12C inhibitors is that the G12C subtype accounts for less than 20 percent of all KRAS mutations. As a result, the research and development focus has shifted to the G12D mutation subtype, which has a higher prevalence, and to pan-KRAS inhibitors that can cover multiple mutation subtypes, fueling the sudden surge in interest in pan-KRAS inhibitors. Currently, there are more than ten pan-KRAS inhibitors in development worldwide, but most are stalled at the Phase I clinical trial stage. Among these, multinational pharmaceutical companies such as Pfizer, Lilly, and Boehringer Ingelheim have already made early bets.

Interestingly, some pharmaceutical companies have even begun experimenting with quantum computing to assist in pan-KRAS drug screening, and the corresponding research was selected as one of the top ten research advances of 2025 by Nature Biotechnology.

In this study, Insilico Medicine combined quantum computing with artificial intelligence to generate and screen up to one million small molecules targeting KRAS mutations. Using the Chemistry42 platform, Insilico Medicine identified 15 of the most promising compounds. After wet-lab testing, two molecules—ISM061-018-2 and ISM061-022—stood out. Data showed that ISM061-018-2 performed the best, demonstrating dose-dependent inhibitory activity against five common KRAS mutation types (G12C, G12D, G12V, G13D, and Q61H) as well as wild-type HRAS and NRAS, with no significant non-specific cytotoxicity.

Notably, in February 2026, Insilico Medicine nominated ISM6166 as a pan-KRAS preclinical candidate compound. Although ISM6166 is not directly related to the aforementioned study, this cross-disciplinary effort at least demonstrates that pharmaceutical companies are eager to seize every opportunity to board the pan-KRAS inhibitor train. This is evident from recent transaction prices for pan-KRAS assets.

At present, whether through outright acquisitions or pipeline licensing deals, multinational pharmaceutical companies are offering unusually high prices for pan-KRAS inhibitors.

On the merger and acquisition front, in the deal that ultimately fell through, MSD reportedly offered between 28 billion and 32 billion United States dollars for Revolution. This would have ranked as the third-largest merger and acquisition transaction in pharmaceutical history, behind only Bristol Myers Squibb's acquisition of Celgene (74 billion United States dollars) and AbbVie's acquisition of Allergan Aesthetics (63 billion United States dollars). In recent years, although multinational pharmaceutical companies have accelerated their pace of acquiring biotech companies, most acquisition deals have been valued below 20 billion United States dollars. For example, in 2025, Johnson & Johnson acquired Intra-Cellular Therapies for 14.6 billion United States dollars in cash, betting on the central nervous system blockbuster drug CAPLYTA®. That transaction was already one of the largest acquisitions in Johnson & Johnson's history.

On the pipeline licensing front, in the transaction between Jacobio Pharma and AstraZeneca, the latter also offered a high price rarely seen even in the red-hot early-stage clinical asset deal market of recent years.

In December 2025, Jacobio Pharma announced a license and collaboration agreement with AstraZeneca to develop and commercialize the pan-KRAS inhibitor JAB-23E73. Under the agreement, AstraZeneca obtained rights to research, develop, register, manufacture, and commercialize JAB-23E73 outside mainland China. The deal includes an upfront payment of 100 million United States dollars, milestone payments of up to 1.915 billion United States dollars, and subsequent tiered royalties.

The previous time a similarly high-priced early-stage clinical asset deal emerged was in late 2023. In November 2023, AstraZeneca and Eccogene entered into an exclusive license agreement for the oral GLP-1 formulation ECC5004. Both transactions involved early-stage clinical assets and made waves at the time with similarly high price tags. However, upon closer examination, JAB-23E73 commanded an even higher price. After all, when the ECC5004 deal was finalized, the Phase I clinical trial had already produced preliminary results demonstrating differentiated clinical advantages. In contrast, JAB-23E73 was only in Phase I clinical trials in China and the United States, with only early signs of anti-tumor activity observable.

As the most sought-after innovative drug asset this year, the ticket to enter the pan-KRAS inhibitor space is clearly more expensive than that of previously popular target pipelines. Nevertheless, more technological and financial support is undoubtedly a great thing for overcoming the challenges of KRAS-targeted drug development.

New Variables?

Despite being highly sought after, the clinical value of pan-KRAS inhibitors for the treatment of KRAS-mutant tumors remains questionable. Particularly in the face of faster-progressing KRAS G12D inhibitors, the commercial prospects of pan-KRAS inhibitors are not as bright as they might seem.

At this stage, mainstream pan-KRAS inhibitor development follows two technical approaches: molecular glues and allosteric small molecules. Pan-KRAS inhibitors are broad-spectrum targeted drugs that can simultaneously inhibit multiple KRAS mutations. The two technical approaches differ significantly in their targeting logic and development strategies. Overall, more pharmaceutical companies have pursued allosteric small molecule pan-KRAS pipelines, but molecular glue KRAS inhibitors have advanced further in development.

On one hand, the molecular glue approach, represented by Revolution's RMC-6236, is the most clinically advanced pan-KRAS pipeline globally. RMC-6236 blocks the interaction of RAS (in its active state) with its downstream effectors to inhibit RAS signaling, and can simultaneously inhibit three RAS proteins: KRAS, HRAS, and NRAS. In September 2025, Revolution announced Phase I clinical trial data for RMC-6236 in patients with metastatic pancreatic ductal adenocarcinoma. As a monotherapy in both second-line and first-line treatment of metastatic pancreatic ductal adenocarcinoma patients, RMC-6236 demonstrated favorable disease control rates and objective response rates.

On the other hand, many early-stage pan-KRAS inhibitor programs have adopted the allosteric small molecule approach. Examples include Boehringer Ingelheim's BI-3706674, Pfizer's PF-07934040, and Jacobio Pharma's JAB-23E73, all of which fall into this category. Technically, allosteric small molecule inhibitors are highly selective for KRAS and, in principle, offer better resistance to drug resistance. For instance, Jacobio Pharma's JAB-23E73 can inhibit both the active and inactive states of KRAS, but does not significantly inhibit HRAS and NRAS proteins.

An unavoidable issue is that the clinical application of pan-KRAS inhibitors still faces inherent technical challenges. For example, achieving high selectivity for mutant KRAS over wild-type KRAS and other RAS subtypes to minimize off-tumor toxicity remains difficult. Additionally, the short half-life of existing pan-KRAS inhibitors and the unclear mechanisms of resistance also limit their widespread clinical use to some extent.

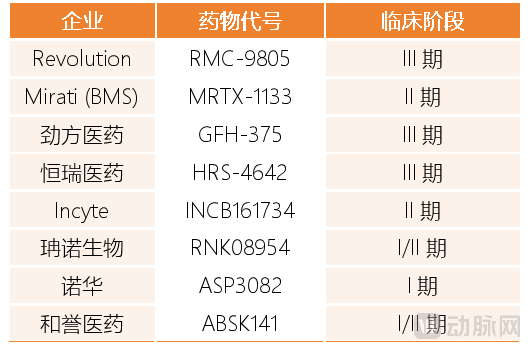

Against this backdrop, KRAS G12D inhibitors have risen to prominence, adding a new variable to the KRAS drug market. In a sense, the development of KRAS G12D-targeted drugs has also entered a critical stage of intensive effort this year. First, Revolution prominently showcased research results for its KRAS G12D pipeline RMC-9805 at JPM 2026. RMC-9805 has already received Breakthrough Therapy Designation from the United States Food and Drug Administration and is planned to initiate two pivotal Phase III studies in non-small cell lung cancer and pancreatic cancer in 2026, moving rapidly from early research into the registration sprint phase. Also entering Phase III clinical development are GenFleet Therapeutics' GFH-375 and Hengrui Pharma's HRS-4642.

Furthermore, multiple KRAS G12D pipelines being developed by pharmaceutical companies, including both multinational pharmaceutical companies and biotechs, are expected to reach key clinical development milestones in 2026. For example, Novartis' KRAS G12D protein degrader ASP3082 is expected to initiate first-in-human trials in 2026, and Mirati's MRTX-1133 is expected to read out Phase II clinical data in 2026 as well.

Nearly half a century after KRAS was identified as a cancer driver mutation, a broadly applicable KRAS-targeted drug has finally entered the eve of truly benefiting clinical practice. The surge of capital and technology brought by fierce competition among major pharmaceutical companies, while capturing attention, has also accelerated the pace at which a growing number of KRAS-targeted agents are poised to change clinical practice.