Breaking the Chronic Kidney Disease Dilemma: These Are the 7 Most Promising Pipelines in China

China's chronic kidney disease market is moving from a silent blue ocean to an innovative风口.

Chronic Kidney Disease (CKD) is quietly evolving into a global public health crisis. In China, this silent killer has affected more than 156 million people, with an awareness rate as low as 12.5%, meaning that nearly 90% of patients are unaware as their kidney function silently deteriorates. More alarmingly, after CKD patients progress to end-stage renal disease (ESRD), over 300,000 new dialysis patients are added annually, and the high cost of treatment places a heavy burden on families and society.

Compared with the rapid advancements in innovative drugs for oncology and cardiovascular fields, the treatment landscape for CKD has remained almost stagnant for a long time. The current standard treatments are still limited to RAS inhibitors (ACEi/ARB) and hormone/immunosuppressants. The former can only reduce proteinuria by 20%~30%, while the latter, although capable of suppressing immune responses, is associated with severe side effects such as infections, osteoporosis, and metabolic disorders. For common primary glomerular diseases like IgA nephropathy and membranous nephropathy, 30%~40% of patients will still progress to renal failure within 20 years under existing treatments.

This treatment dilemma makes it urgent for clinical practice to have innovative therapies that can precisely intervene in disease mechanisms.

A turning point has emerged. With the deepening exploration of the pathogenesis of CKD, a batch of innovative drug pipelines made in China is accelerating towards clinical trials, achieving breakthroughs in key pathways such as immune nephropathy and complement-mediated renal injury. Some have already submitted applications for market approval or entered the late stages of clinical trials. These pipelines not only represent a leap from following to parity in China's biopharmaceutical industry but also herald that CKD treatment is about to bid farewell to the era of "hormones can do everything" and step into a new epoch of precise targeting and combination intervention.

The unique pattern of CKD etiology in China provides a clear direction for precision treatment and differentiated innovation.

Based on the pathogenesis, CKD can be divided into three categories: primary kidney disease, secondary kidney disease, and hereditary kidney disease. The market potential for primary kidney diseases such as IgA nephropathy is astonishing. Everest Medicines' NefIgAcy rapidly gained traction upon approval and even achieved a sales record of 500 million yuan in a single month. Meanwhile, secondary kidney diseases are expanding quickly alongside the growing prevalence of metabolic disorders. Particularly as renal function deteriorates, its progression is associated with various severe complications. For instance, at the stage of renal insufficiency, about 10% of patients develop hyperphosphatemia, which may lead to mineral metabolism disorders and increase the risk of cardiovascular diseases.

According to Frost & Sullivan, the market size of IgA nephropathy treatment drugs in China is expected to grow from US$37 million in 2020 to US$109 million in 2025, with a compound annual growth rate (CAGR) of 24.6%. It is expected to further expand to US$507 million by 2030, increasing nearly 13.7 times over a decade, with a CAGR as high as 36.2%, far exceeding the average level of the pharmaceutical industry.

Despite the huge market potential of CKD, there are obvious shortcomings in the existing treatment options, which is exactly the core value space for innovative drug breakthroughs.

Traditional treatment strategies for CKD rely on controlling blood pressure by blocking the renin-angiotensin system, as well as controlling blood glucose. Such methods can only delay the onset of end-stage renal disease and may be accompanied by significant side effects. Therefore, for a long time, no new therapies for treating CKD have been approved for marketing.

Development History of CKD Drugs, Image Source: Company Prospectus

Early CKD management primarily focused on core renal function tests (e.g., the Jaffe creatinine method). It was not until 2019 that the FDA designated changes in proteinuria levels as a surrogate endpoint for the approval of IgA nephropathy drugs. This move enabled more efficient conduct of key clinical trials for CKD, accelerating breakthroughs in research and development within this field.

Since 2020, the development of various treatments, including non-steroidal mineralocorticoid receptor antagonists (nsMRAs), hemodynamic modulators, IgA proteases, B-cell depletion therapies, and complement therapies, has been accelerating, potentially offering more effective and safer treatment options for CKD. In addition, there is growing attention on the research and development targeting difficult-to-manage CKD complications such as hyperphosphatemia. Continuous innovation in CKD drug development is expected to address significant unmet medical needs, improve patient outcomes, and transform standard care.

CKD drugs are moving towards precision treatment.

Considering the high treatment costs required for end-stage renal disease patients, to evaluate the value of a CKD pipeline, we must not only assess clinical efficacy validation, unmet needs in indications, and commercial certainty but also fully consider whether the pipeline can deliver long-term value, such as reducing hospitalizations or delaying dialysis, and saving the use of medical insurance funds in the long term. This would help achieve a new commercialization path for domestically produced innovative drugs similar to Everest Medicines' NefIkon, which follows a rapid approval-rapid insurance inclusion-rapid scaling model.

Some Potential CKD Pipelines Produced in China, According to Public Data Collection

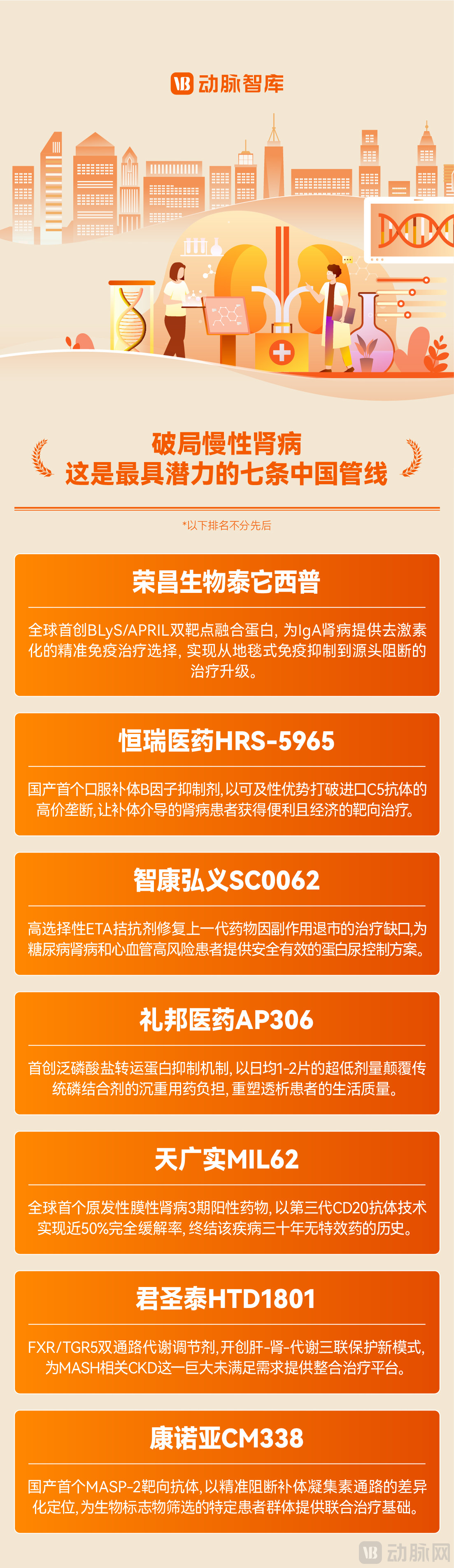

Rongchang Bio Taialup (IgA Nephropathy)

RemeGen's Telitacicept (RC18) Demonstrates Breakthrough Efficacy Data in Phase 3 Clinical Trials in China for IgA Nephropathy, the Most Common Type of Primary Glomerulonephritis. After 39 Weeks of Treatment, the 24-Hour Urine Protein-to-Creatinine Ratio (UPCR) Decreased Significantly by 55% Compared to the Placebo Group (p<0.0001), with eGFR Remaining Stable. This Reduction Surpasses Existing Therapies, While Also Showing Excellent Performance in Maintaining Renal Function Stability, Alleviating Hematuria Levels, and Demonstrating Tolerability and Safety.

As the world's first dual-target fusion protein targeting BLyS/APRIL, it controls disease progression at its source by blocking BLyS to inhibit the maturation of immature B cells, and reduces the deposition of immune complexes in the kidneys by blocking APRIL to decrease plasma cell secretion of Gd-lgA1 and related antibodies. This addresses a significant unmet need in IgA nephropathy, which previously had only two effective drugs, enabling hormone-free treatment with high unmet demand. In terms of commercial certainty, Rongchang Biotech’s Telitacicept has already submitted an NDA and established a mature sales team for autoimmune diseases (with the lupus erythematosus indication already approved and marketed), demonstrating well-validated channels. This pipeline not only represents a pioneering innovation in China but also shows, through actual data, its potential to become the first重磅IgA nephropathy drug independently developed in China.

Hengrui Medicine HRS-5965 (IgA Nephropathy)

Hengrui Medicine's HRS-5965 is a novel oral selective complement factor B (CFB) inhibitor, being developed for the treatment of paroxysmal nocturnal hemoglobinuria, primary IgA nephropathy, glomerular diseases, and hemolytic anemia. Among these, the primary IgA nephropathy indication was included in the breakthrough therapy program by the CDE in March 2025, and paroxysmal nocturnal hemoglobinuria was proposed for priority review by the CDE in October 2025. Its clinical efficacy validation is based on solid phase 2 data and a novel target mechanism. Although the phase 3 results have not yet been unblinded, the inclusion in the priority review has indirectly confirmed its data quality and regulatory recognition.

In terms of unmet needs, targeting the complement lectin pathway differentiates itself from existing therapies (C5 inhibitors are expensive and inconvenient to administer), but competition within the IgA赛道 remains intense. The commercial certainty is Hengrui's advantage, with its nephrology channel being top-tier in China, and its Phase 3 clinical execution and registration progress speed highly reputed. Although it has not yet submitted an NDA, the probability of future approval is extremely high. Hengrui's platform extensibility and market access capabilities make its prospects promising.

ZhiKang HongYi SC0062 (IgA Nephropathy)

SC0062, developed by Zhikang Hongyi, is a novel, highly selective endothelin receptor A (ETA) small molecule antagonist with BIC potential, designed to address the significant unmet clinical needs of various kidney diseases. It is currently undergoing Phase 3 clinical trials for IgA nephropathy. Previously, SC0062 was designated as a breakthrough therapy by the CDE for the treatment of IgA nephropathy with proteinuria and, in June 2025, was again included in the CDE’s breakthrough therapy list for the treatment of diabetic kidney disease (DKD) with albuminuria.

SC0062 by ZhiKang Hongyi Achieves 51.6% Reduction in UPCR at 24 Weeks in Phase 3 Clinical Trial for IgA Nephropathy, Demonstrating Efficacy Comparable to Leading Competitors; Its Unique Mechanism Stands Out in Addressing Unmet Needs, with the ETA Pathway Representing a Differentiated Target in the Nephrology Field, Avoiding Direct Competition with Complement Inhibitors. Additionally, SC0062 Overcomes Key Limitations of Previous-Generation ETA Antagonists, Such as Sodium Retention, Hepatotoxicity, and Poor Proteinuria Control in Diabetic Nephropathy, Exhibiting Excellent Safety Profiles Including When Combined with SGLT2 Inhibitors in Studies. However, Commercialization Certainty is Constrained by the Company’s Size, Despite High Clinical Development Efficiency, Due to the Lack of an Established Sales Network, Requiring External Partnerships for Successful Commercial Implementation.

Libang Pharmaceuticals AP306 (Refractory Hyperphosphatemia)

AP306, developed by Libang Pharmaceuticals, is in the completed phase of a 2a clinical trial. Targeting patients with refractory hyperphosphatemia who are poorly controlled by existing phosphate binders, AP306 is a potential first-in-class (FIC) pan-phosphate transporter inhibitor. It is also the world’s first pan-phosphate transporter inhibitor in clinical development for the treatment of hyperphosphatemia. In June 2024, the Chinese National Medical Products Administration granted AP306 Breakthrough Therapy Designation for treating hyperphosphatemia in CKD patients, providing assurance in terms of clinical efficacy validation.

AP306 Excels in the Dimension of Unmet Needs: Compared with Existing Phosphate Binders (Sevelamer, Lanthanum Carbonate) That Require High Dosages (Approximately 2400mg~4800mg) and Must Be Taken with Meals, AP306 Blocks Phosphorus Absorption in the Intestines with a Daily Dose of Only 225mg~450mg, Offering Better Patient Compliance and Effectively Avoiding Homogeneous Competition. In Terms of Commercialization Certainty, LaboMed Pharma Focuses on Nephrology, and Its Current Nephrology Sales Team for the Marketed Product Meixunluo (AP601) Can Be Reused for AP306; However, AP306 Is Still About Three Years Away from Launch, and the Time Uncertainty Lowers Its Commercialization Score. Notably, AP306 and AP301 (Iron-Based Phosphate Binder) Form an Internal Product Portfolio for LaboMed, Covering Different Patient Groups. If Subsequent Clinical Trials Validate Efficacy in Refractory Populations, Its Market Value Will Far Exceed That of Existing Ordinary Phosphate Binders.

Tian Guangshi MIL62 (Primary Membranous Nephropathy, PMN)

As the world's first drug to achieve positive results in a Phase 3 clinical trial for primary membranous nephropathy (PMN), Tian Guangshi's MIL62 stands out by utilizing third-generation CD20 antibody technology, significantly enhancing antibody-dependent cellular cytotoxicity effects. It achieved a clinical complete remission rate of 49.4% (compared to only 3.9% for traditional cyclosporine) and reduced the median time to remission from several months to 5 weeks, completely reshaping the treatment landscape for PMN, a disease previously lacking an effective global treatment.

Following the successful trajectory of Naifukang in "filling global gaps + breakthrough efficacy + made-in-China identity," the future potential value of MIL62 will be reflected in three dimensions: First, the high certainty of medical insurance access; second, the authority to define treatment standards—as the world’s first drug with positive PMN3 phase data, it has the potential to rewrite the KDIGO international guidelines and establish Chinese companies' voice in the B-cell targeted therapy field; third, the extensibility of the technology platform—its enhanced ADCC antibody platform can be rapidly replicated for other B-cell-mediated autoimmune diseases, forming an indication matrix ranging from nephrology to rheumatology and immunology.

JunShengTai HTD1801 (Cardiorenal Metabolic System Disease CKM)

HTD1801 is a novel ionic compound composed of berberine (BBR) and ursodeoxycholic acid (UDCA), representing a first-in-class new molecular entity (NME). Its uniqueness lies in achieving triple protection for the liver, kidney, and metabolism through the FXR/TGR5 dual-pathway mechanism. Unlike single-target agents such as SGLT2i or GLP-1RA, it not only improves glucose and lipid metabolism but also directly inhibits renal fibrosis progression. Preclinical studies have shown that its combination with GLP-1RA can synergistically reduce weight and reverse muscle loss caused by semaglutide alone, demonstrating potential as an integrated therapeutic solution. It is currently in Phase 3 clinical trials.

Its future potential value is reflected in: First, filling the treatment gap for MASH-related CKD, with the hope of becoming the first approved oral drug for this indication, opening a new interdisciplinary track for metabolic-kidney treatment; Second, its uniqueness makes it likely to gain recognition in medical insurance negotiations; Third, its hub value in combination therapy—its metabolic regulatory mechanism complements SGLT2i and GLP-1RA, potentially forming a "HTD1801+GLP-1RA+SGLT2i" triple therapy for metabolic kidney disease in the future, becoming a cornerstone drug in standard treatment plans for diabetic nephropathy and MASH-CKD; Fourth, the expansion of indications. According to company disclosures, HTD1801 outperformed the current mainstream drug dapagliflozin in head-to-head comparisons for type 2 diabetes—not only showing advantages in reducing glycated hemoglobin (primary endpoint) but also demonstrating statistical superiority in improving multiple cardiometabolic indicators.

Connie CM338 (IgA Nephropathy)

As the first MASP-2 monoclonal antibody in China to enter clinical trials, CM338 from Connomab has demonstrated a novel target advantage upon completion of Phase 1 for IgA nephropathy. It could potentially address current unmet needs in complement drugs, such as their inability to differentiate pathways, the lack of precision treatment for LP-activated patients, and the necessity to combine with C5 inhibitors to achieve full pathway blockade. Although it is difficult to provide a high evaluation of clinical efficacy validation due to its early stage, in terms of unmet needs, it ranks among the leading group globally in the MASP-2 field, possessing the value of being a pioneering product produced in China. The commercial certainty is relatively low due to the long time before market entry. However, this pipeline represents the exploratory spirit of innovative pharmaceutical companies in China targeting cutting-edge renal disease targets. If subsequent Phase 2 data confirms its safety and efficacy, it will have overseas business development potential.

The staggering scale of China's CKD patient population forms the bedrock of the market.

According to data from The Lancet, in 2023, approximately 156.15 million people in China suffered from chronic kidney disease, and about 1.5389 million died from it. The research team found that from 1990 to 2023, the burden of chronic kidney disease caused by type 2 diabetes and hypertension increased significantly. In 2023, the leading causes of death from chronic kidney disease were hypertension (19.6%), type 2 diabetes (18.9%), and glomerulonephritis (10.9%).

Standing at the current juncture, the field of chronic kidney disease treatment is undergoing a leap from symptom delay to precise intervention. The rapid inclusion of Nefecon in medical insurance not only marks the success of a drug but also validates the recognition by medical insurance payers of a model that fills clinical gaps, saves long-term funds, and prioritizes innovation produced in China, paving a replicable access path for subsequent innovative drugs. These potential pipelines, from dimensions such as immune regulation, complement inhibition, metabolic intervention, and complication management, construct a multi-dimensional treatment network covering IgA nephropathy, membranous nephropathy, diabetic nephropathy, and dialysis patients.

Their value lies not only in the breakthrough of individual efficacy data but also in representing a systematic leap in China's biopharmaceutical industry: from following to running neck-and-neck, from single-target to multi-pathway regulation, and from reliance on imports to domestically produced alternatives. In the coming years, as these drugs are gradually approved and included in medical insurance, the treatment landscape for CKD will bid farewell to the old era dominated by the omnipotence of hormones and waiting for dialysis, entering a new epoch characterized by mechanism-based subtyping, precision medication, and combined intervention.

For China's 156 million CKD patients, this means a longer dialysis-free survival period, a higher quality of life, and more affordable treatment options; for the medical insurance fund, it represents a strategic shift from passively paying high costs at the end stage to proactively investing in early precision intervention; for China's innovative drug industry, this is the starting point for establishing standards and exporting solutions in the global chronic disease treatment field. When these pipelines ultimately converge into routine clinical practice, we may witness a new historical moment: Chinese patients benefit first from local innovation, and the world follows China's treatment standards.

References:

- https://doi.org/10.1016/j.lanwpc.2025.101776