Semaglutide Patent Expires Today, 12 Fastest Chinese-Made Needles!

Qilu Pharmaceutical

Specialty Formulations and Active Pharmaceutical Ingredients (API) Developer

On March 20, 2026, the core compound patent for semaglutide held by the Danish pharmaceutical company Novo Nordisk will officially expire in China. This means that pharmaceutical companies in China can now use the molecular structure of semaglutide for production. Previously stalled due to patent protection, the marketing applications for domestically produced generic versions of semaglutide have now entered the formal review and approval process.

Semaglutide, as Novo Nordisk's "star product," generated $36.1 billion in sales in 2025, with a year-on-year increase of over 10%. Due to the highly attractive commercial prospects, the battle for domestically produced semaglutide has just begun, yet is already filled with intense competition.

The Initial Stage of the Battle Situation?

First, clarify one premise: in the generic drug market, securing the first generic often establishes a unique competitive position that is difficult for competitors to shake. However, the semaglutide market will be more complex, as it spans two major indications—diabetes treatment and weight loss. Particularly for weight loss, it remains an untapped market with enormous potential.

VCBeat queried the website of the National Medical Products Administration and found that, as of the time of writing, 12 domestically produced semaglutide generic drugs from 10 pharmaceutical companies in China, including Jiuyuan Gene, Xibeijiang Pharmaceutical (Livzon Group), and Qilu Pharmaceutical, have successively submitted registration applications. Although all are queued up at the starting line, the competition for the first generic drug is relatively clear.

Data Source: National Medical Products Administration (NMPA)

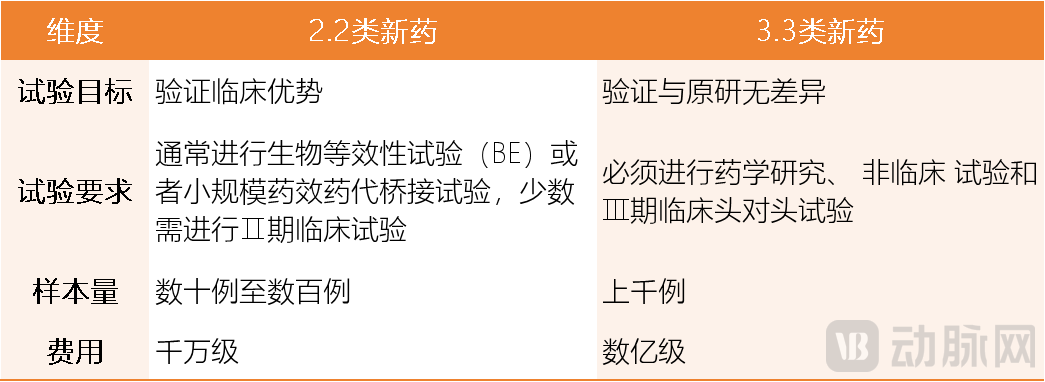

Here, it is important to note the unique phenomenon in the registration of semaglutide. As generic versions of semaglutide, some pharmaceutical companies have opted to file for approval as Class 2.2 new drugs (modified new chemical drugs), such as Qilu Pharmaceutical and Bcht Biotechnology (Shijiazhuang Pharmaceutical Group). Meanwhile, other companies have chosen to apply as Class 3.3 new drugs (generic versions of therapeutic biological products), such as Jiuyuan Gene and Xinbei River Pharmaceutical.

This is because the regulatory approach in China is relatively flexible, allowing structurally defined peptide chemical drugs to be categorized under chemical drug management, bypassing the requirements for Class 3.3 new drugs and instead registering as Class 2.2 new drugs. The latter has significantly lower requirements in terms of trial objectives, trial requirements, sample size, costs, and other aspects compared to the former. Semaglutide, as a synthetic peptide, has its amino acid sequence, modification sites, purity, and other characteristics fully controllable through chemical methods, with its structure also being precisely characterizable, meeting the criteria for biologics to be managed as generic chemical drugs.

Comparison of Different Registration Categories Data Source: Collated from Public Information

Currently, due to differences in registration categories, the position of the first domestic generic version of Semaglutide in China is most likely already directly secured.Qilu Pharmaceutical and Changchun Bcht Biotechnology, which have chosen to file for registration as Class 2.2 new drugs, have entered the final stage of the race to be the first to replicate semaglutide.

Among them, Qilu Pharmaceutical submitted a registration application for semaglutide for type 2 diabetes as early as September 2024, nearly a year ahead of Changchun Bcht Biotechnology Co.'s first indication registration. However, in December 2025, Changchun Bcht Biotechnology Co. filed for a second indication, weight management, while Qilu Pharmaceutical only has one indication that has entered the registration process. It is widely speculated that semaglutide from Qilu Pharmaceutical and Changchun Bcht Biotechnology Co. will be approved for marketing as early as the third quarter of 2026, but it is still difficult to predict which company will prevail.

Typically, generic drugs that flood the market after the expiration of the original drug patent are highly homogeneous. To gain a foothold in the market, they can only compete on price and distribution channels. However, the first-to-market generic drug is different. By leveraging the review gap period between the first-to-market generic and subsequent generics, it can accomplish many crucial tasks such as hospital access, market education, and medical insurance coverage, thereby forming a competitive advantage. As a leading player in China's generic drug industry, Qilu Pharmaceutical has reaped significant benefits from being the first to market with generics. Its earlier product, Oxaliplatin Injection, and its most profitable single product, Bevacizumab Injection, were both the first domestically produced generic versions in China. In particular, Bevacizumab Injection remains the best-selling drug of its kind in China, with a market share that even surpasses that of the original drug manufacturer, Roche.

The Battle for Supremacy in China-Produced Needles

It was mentioned earlier that the battle for semaglutide will be more complex.

On the one hand, it is the pressure from biosimilars,Jiuyuan Gene and Xinbei River Pharmaceutical, which are in line at the NMPA, submitted the registration application for Semaglutide even earlier than Qilu Pharmaceutical. Huadong Medicine, which follows closely behind, is also eyeing the opportunity. Notably, Jiuyuan Gene and its sibling company Huadong Medicine were once considered strong contenders to secure the first generic version of Semaglutide, especially Huadong Medicine.

At first, Zhongmei Huadong attempted to launch its product before the patent expiration by simultaneously challenging Novo Nordisk's core patent. However, the Supreme People's Court of China ultimately ruled in favor of the validity of Novo Nordisk's patent. Subsequently, Zhongmei Huadong fully transitioned to a biosimilar development pathway, but with clear advantages in clinical data, submission quality, and commercialization capabilities, it remains a strong competitor for the first generic drug. Zhongmei Huadong prioritizes speed, while Jiuyuan Gene focuses on stability. In February 2026, Jiuyuan Gene submitted a registration application for the weight-loss indication of semaglutide, challenging the status of being the first Chinese-produced weight-loss injection.

According to external speculation, Jiuyuan Gene may achieve the approval and market launch of Semaglutide for both hypoglycemic and weight-loss indications as early as the first half of 2027, while Zhongmei Huadong might obtain the market qualification for Semaglutide in the second half of 2027. If both companies complete the review process as expected, there will be little time left for Qilu Pharmaceutical or Changchun Bcht Biotechnology Co.

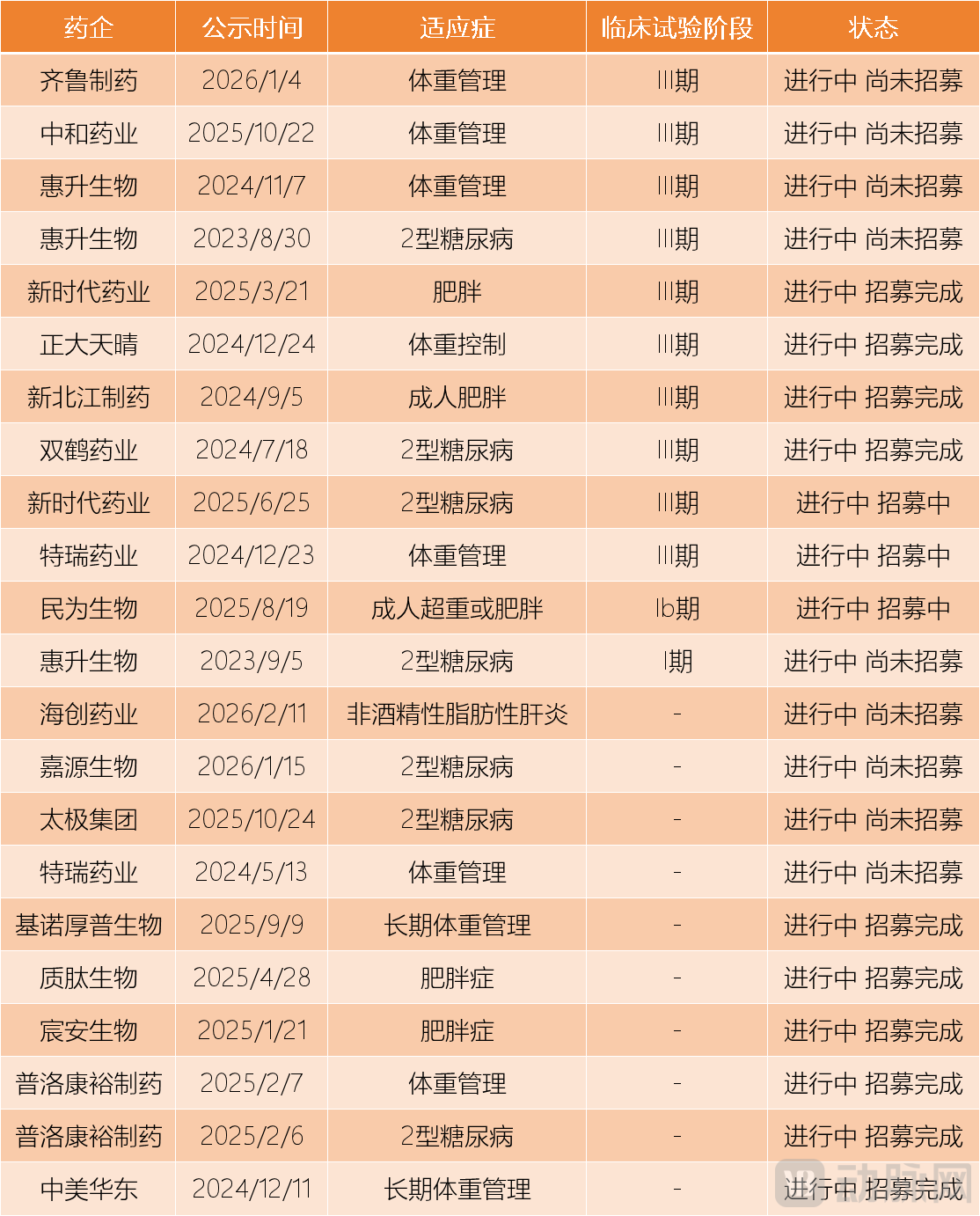

On the other hand, outside the cohort of registration applications, there are more than a dozen companies that have also registered as Class 2.2 new drugs and are currently conducting clinical trials, with registration applications imminent.Especially for pharmaceutical companies like CR Double-Crane and Hanyu Pharmaceutical that started clinical trials earlier. In investor interactions at the end of last year, CR Double-Crane stated that the Phase III clinical trial for the hypoglycemic indication of semaglutide is proceeding as planned and is expected to be completed within 2025, but did not disclose a possible launch time; the weight loss indication is also undergoing internal evaluation. Meanwhile, Hanyu Pharmaceutical confirmed that Phase III clinical trials for both weight management and hypoglycemic indications of semaglutide have been initiated, with all subjects already enrolled, receiving dosing and follow-ups, and entering the final stage, with clinical trials expected to be completed within 2025. Some investors speculate that Hanyu Pharmaceutical's hypoglycemic indication for semaglutide will be approved by the end of 2026 or early 2027.

Some Chinese manufacturers of semaglutide classified as Category 2.2 that are currently conducting clinical trials. Data source: Compiled from public information.

The Year of Weight Loss Market Explosion

The reason why pharmaceutical companies have disruptive power in the weight loss indication is that this imaginative market of weight loss has yet to see a dominant player emerge.

In the stock market, Novo Nordisk previously failed to tap into the domestic weight-loss market. In China, the diabetes indication for the original drug semaglutide was included in the national medical insurance in 2021, but its weight-loss indication has not been covered by insurance to date, focusing mainly on the out-of-hospital self-pay market. According to the latest financial report from Novo Nordisk, in 2025, the sales of semaglutide in Greater China are expected to reach approximately 5.4 billion Danish kroner, equivalent to about 6.7 billion RMB, of which the diabetes version generated approximately 5.645 billion RMB in sales, nearly seven times the approximately 835 million RMB generated by the weight-loss version. Overseas, the sales ratio of the diabetes version to the weight-loss version of semaglutide is 2:1.

In terms of the incremental market, China is poised to experience a boom year in 2026.First, there is a halving of the terminal selling price.According to different indications and medication stages, Semaglutide available for sale in China comes in multiple specifications, including 0.68mg/mL (1.5mL pre-filled), 1.34mg/mL (1.5mL pre-filled), 1.34mg/mL (3mL pre-filled), 2.27mg/mL (3mL pre-filled), and 3.2mg/mL (3mL pre-filled). At its initial launch, the standard hypoglycemic dose of 1.34mg/mL (1.5mL pre-filled) Semaglutide was priced at 1,120 yuan per pen, now reduced to 478.8 yuan per pen. The regular weight-loss dose of 2.27mg/mL (3mL pre-filled) also dropped from 1,893.67 yuan per pen to the current price of 987.48 yuan per pen, with both experiencing a reduction of over 50%.

Industry insiders widely predict that after the clustering market entry of domestically produced semaglutide, the price will further decrease. Calculating based on the maintenance dose for weight loss, the monthly cost of using the original semaglutide is about 1600 yuan. If the domestic pricing is lower, it will already fall within a range affordable to most people.

Secondly, in recent years, weight loss clinics have emerged in China.People have long been reluctant to accept weight loss through injections, often perceiving it as sacrificing health for a slimmer figure. However, in weight management clinics, for patients who meet the clinical criteria for obesity, doctors will require them to undergo relevant examinations such as ultrasound, blood, and urine tests before prescribing weight loss treatments, including medications like Semaglutide or even surgery. During the course of treatment, doctors strictly control dosage and duration, with clear guidelines for regular follow-ups. The involvement of medical professionals makes injection-based weight loss safer both perceptually and fundamentally.

Currently, many public hospitals in China have opened weight loss clinics/centers or formed multidisciplinary consultation teams for weight management. Hospitals without dedicated weight loss clinics can still offer weight management services through related departments such as nutrition or endocrinology. According to statistics from VCBeat, as of 2025, 245 tertiary hospitals across China have established weight management clinics. Taking Guangdong as an example, the target rate for setting up weight management and obesity clinics in secondary-level hospitals and above is set at 50% by 2025, with plans to increase it to over 80% by 2026. This new development in hospital disciplines will, to a certain extent, accelerate the release of demand for weight loss solutions. If domestically produced semaglutide can meet this wave of demand, it will undoubtedly occupy a significant market share.

Finally, with the enhancement of Chinese people's ideal for a healthy life, weight loss has been placed in a more important position.According to the 2023 "Report on the Nutritional and Chronic Disease Status of Chinese Residents," as of 2023, the population of overweight and obese individuals in China has exceeded 530 million, making China the country with the highest number of obese people globally. It is projected that by 2030, the obesity rate among Chinese adults will reach 70.5%. As obesity is a significant risk factor for cardiovascular diseases, diabetes, fatty liver, and various cancers, "weight management" has been incorporated into the national strategy. In April 2025, the National Health Commission released the "Dietary Guidelines for Adult Obesity," sparking nationwide discussions on weight loss. Once weight management becomes a social hotspot, it will also drive the release of demand for weight loss.

Written at Last

However, on the other side of the coin, competition in the weight-loss market is becoming increasingly fierce. Behind semaglutide, there are already three layers of challenging forces, each of which has the potential to become the leader in the weight-loss market.

The first force is the domestically produced semaglutide, which is currently under investigation for weight loss indications. This is the nearest challenger. VCBeat queried the drug clinical trial registration platform and found that there are currently 22 clinical trials involving semaglutide underway, of which 14 clinical trials target weight loss indications, accounting for over 60%. Notably, seven weight loss indication trials have reached Phase III, making the obese population with a BMI ≥ 28 increasingly sought after.

Data Source: Collated from public informationPart of the clinical trials of Chinese-produced semaglutide

The second force consists of other GLP-1 class drugs such as Tirzepatide, Masitide, and Enoglutide. These are the most threatening challengers in the short term. By 2025, Semaglutide has already been dethroned from its position as the top drug by Tirzepatide.

Listed GLP-1 Drugs Data Source: Collated from public information

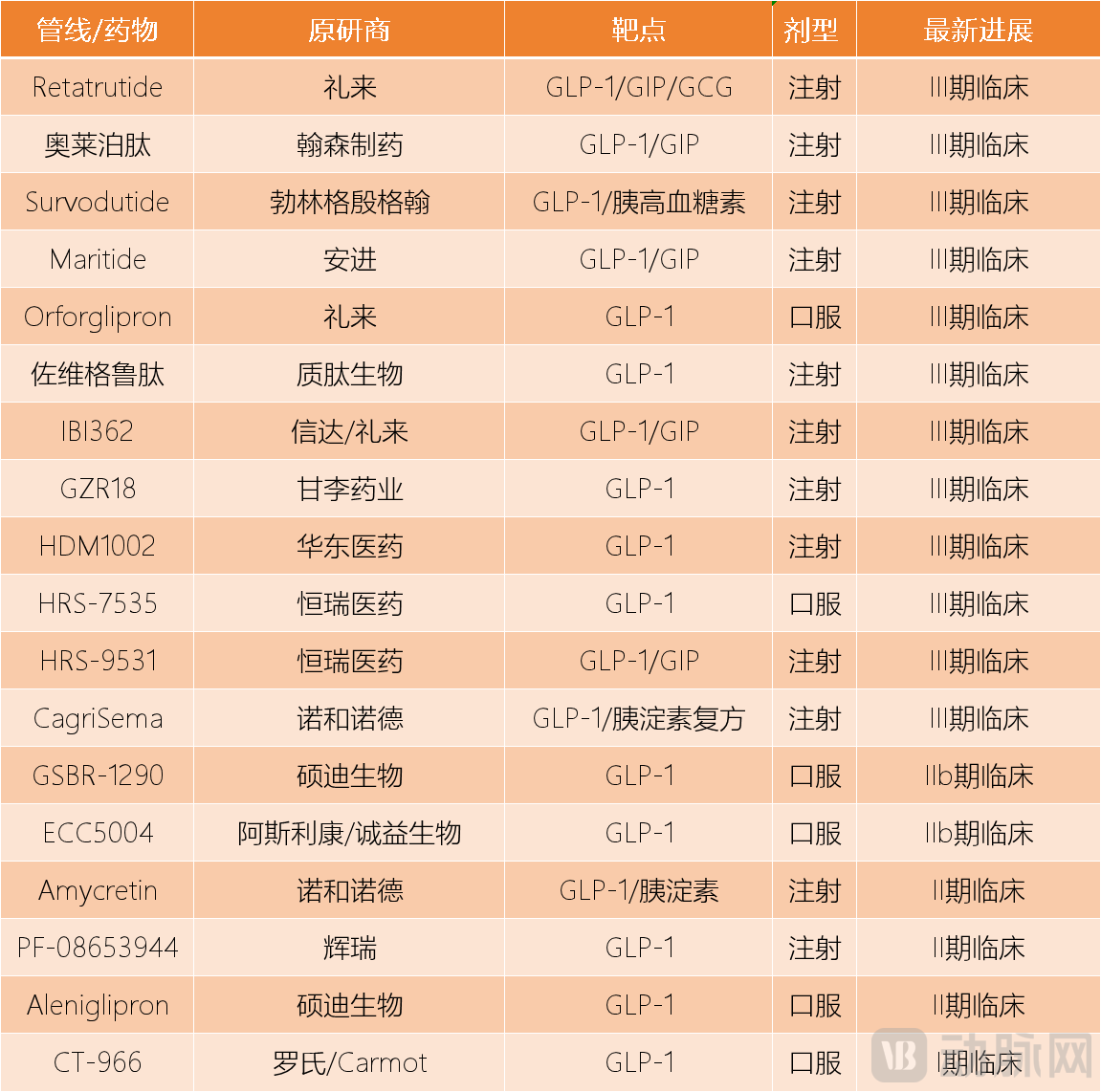

The third force is a large number of GLP-1 iterative drugs under development. These drugs either adopt an oral formulation, target more pathways, or develop long-acting formulations, closely addressing the shortcomings of semaglutide. Most of them have entered Phase III clinical trials and are about to be marketed, posing a long-term threat to semaglutide.

GLP-1 Pipeline in Some Clinical Trials Data Source: Collated from Public Information

Even in this rapidly growing weight-loss market, time is limited for domestically produced semaglutide. An intense battle for brand recognition and the "obesity market" seems imminent.