Puncture Robot Leader TrueHealth Races toward IPO: Valuation Soars 170-Fold in Four Years, Market Share Tops Rankings for Three Consecutive Years

True Health

Medical Surgical Robot Developer

On May 31, 2026, Guangdong True Health Medical Technology Development Co., Ltd. (hereinafter referred to as "TrueHealth") submitted a listing application to the Main Board of the Hong Kong Stock Exchange, with CICC and DBS Group serving as joint sponsors.

A set of figures in the prospectus stands out: TrueHealth's post-money valuation has surged from RMB 13 million in 2021 to RMB 2.23 billion, representing an approximately 170-fold increase over four years.

Why has a non-profitable company secured such a valuation? The answer lies in its market sector. According to data from CIC, the global market size for percutaneous surgical robots is projected to grow from approximately USD 192 million in 2024 to around USD 1.722 billion by 2032, representing a compound annual growth rate (CAGR) of 31.6%. China is the fastest-growing region during this period, with a CAGR as high as 66.1%. This indicates that the industry is entering a critical phase of development.

Just days before TrueHealth filed its listing application, SimpleTouch, a peer in the same sector, also publicly submitted its application for a main board listing. The simultaneous push by these two companies for listings on the Hong Kong Stock Exchange has placed the percutaneous surgical robotics sector at the center of market attention.

1Holding Two First-to-Market Innovations, No. 1 in Market Share for Three Consecutive Years

To understand TrueHealth's valuation logic, one must first answer a question: What makes it the leader in its sector?

TrueHealth, established in 2018 and headquartered in the Hengqin Guangdong-Macao In-Depth Cooperation Zone in Zhuhai, is a nationally recognized "Little Giant" enterprise specializing in sophisticated, unique, and novel products, as well as a high-tech enterprise. It is a rare full-stack player in its sector, not limited to single puncture devices, but covering the entire chain of puncture, ablation, specialized consumables, and ex vivo organ preservation.

The prospectus reveals that TrueHealth holds eight Class III medical device registration certificates and four Class II medical device registration certificates, making it the leading enterprise in the percutaneous puncture surgical robot sector in terms of the number of approved products. It has four models of percutaneous puncture surgical robots, namely TH-S1, TH-S, TH-S Pro, and TH-SA. The TH-S1, TH-S, and TH-S Pro have obtained Class III certification for puncture procedures involving solid organs in the lungs and abdomen, and the application of TH-S1 is currently being expanded to retroperitoneal lesions. The product pipeline also includes the percutaneous microwave ablation surgical robots TH-X MW and TH-X HMW.

Its core product, TH-S1 (Zhenyida® Puncture Surgical Navigation and Positioning System), is the first percutaneous puncture surgical robot approved in China, recognized by the National Medical Products Administration as a "domestic first." Its key product, TH-X MW (Navigation and Positioning Microwave Ablation System), has been acclaimed as an "international first." The former addresses the core pain point of puncture procedures by ensuring "precise positioning and single-pass accuracy," while the latter integrates puncture and ablation—enabling both diagnosis and treatment with a single needle insertion, thereby significantly enhancing diagnostic and therapeutic efficiency.

The ultimate benchmark for technology lies in clinical data. The registration clinical trials for TH-S1 demonstrated a first-attempt puncture success rate of 98.3%, compared to only 15.0% in the traditional manual puncture control group; the average number of needle adjustments per procedure decreased from 1.42 to 0.02; and the complication rate was 6.78%, lower than the 13.33% observed in the control group. This signifies a shift for physicians from "experience-driven iterative adjustments" to "navigation-guided precision in a single attempt," substantially reducing surgical uncertainty.

Leveraging robust product capabilities and clinical validation, TrueHealth ranked first in China's percutaneous puncture and ablation surgical robot market for three consecutive years from 2022 to 2024, according to CIC. To date, the company's devices have been deployed in nearly 100 medical institutions across China, cumulatively supporting over 5,000 procedures. In 2024, TrueHealth achieved 26 trial installations, ranking first nationwide in the number of surgical robots installed for trial use. At a stage when the industry remains predominantly focused on trials and research collaborations, TrueHealth has proactively secured its strategic positioning within hospital channels and among physicians' mindsets.

But the core question for the market arises: Why is the revenue scale so limited despite ranking first in market share and leading in clinical installations?

2Surging Installations, Lagging Revenues: Three Major Bottlenecks Await Breakthrough

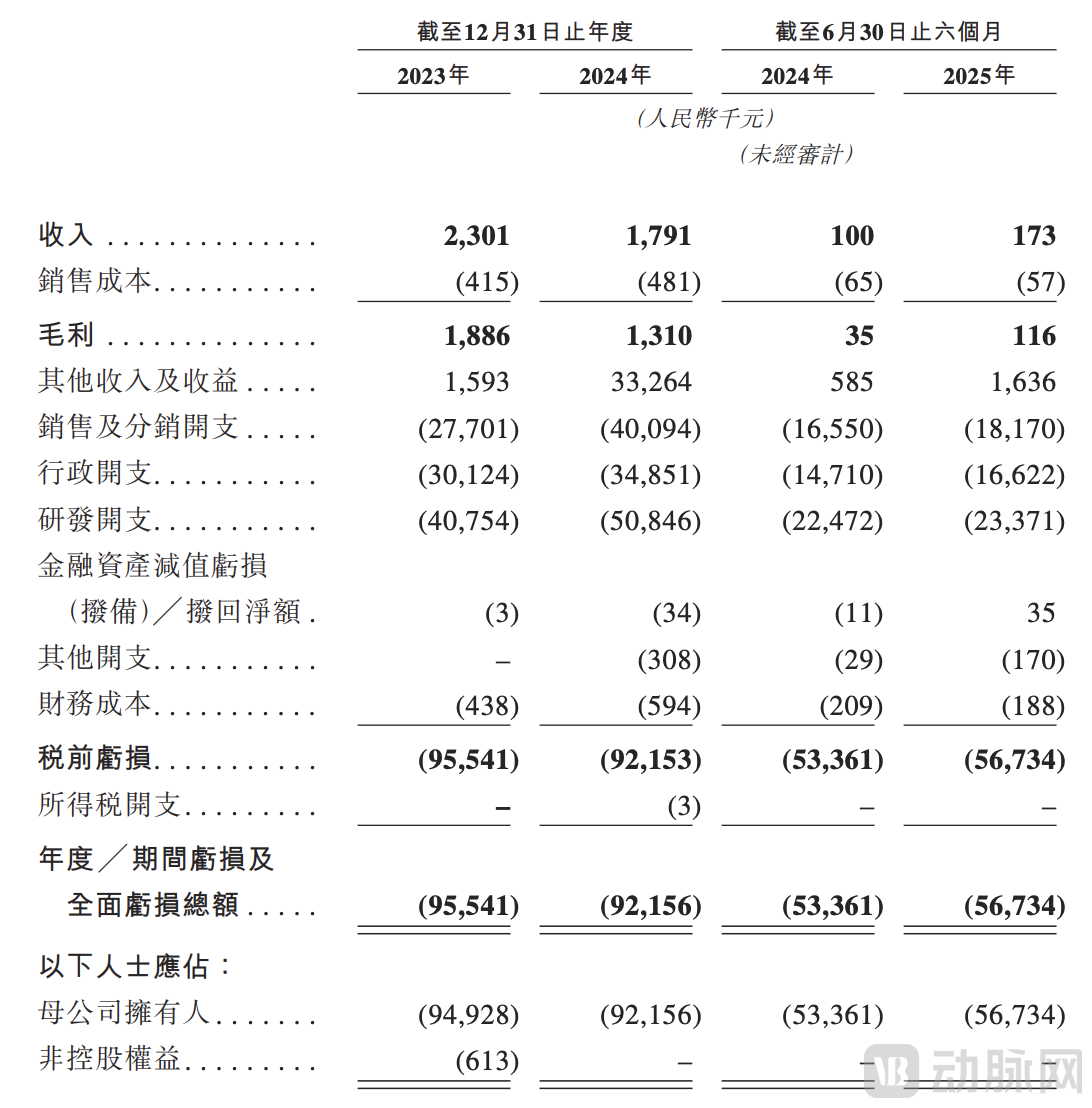

During the reporting period, TrueHealth reported revenues of RMB 2.301 million in 2023 and RMB 1.791 million in 2024, primarily derived from sales of its core products, TH-S1 and TH-S, along with associated consumables. In the first half of 2025, revenue amounted to only RMB 173,000, entirely generated from the sale of disposable specialized consumables, with zero contribution from core product sales during the same period. Net losses for each of these years approached the hundred-million-RMB level, and operating cash flow continued to show net outflows.

Notably, SimpleTouch, a peer in the same sector, finds itself in a similar predicament: ranking second in installed base within the industry, it generated virtually zero revenue for many years prior and has consistently incurred substantial losses. The simultaneous emergence of a disconnect between clinical implementation and commercial monetization among these two leading enterprises does not stem from operational deficiencies; rather, it reflects the current structural characteristics of the percutaneous puncture surgical robotics sector. Publicly available information indicates that the factors constraining commercialization in this sector primarily include the following aspects:

First, the fee structure has long lacked an independent and unified standard. Historically, China lacked a unified fee schedule for robot-assisted surgeries, with pricing models varying across regions. After procuring equipment, hospitals faced a lack of clear and stable billing guidelines, resulting in many devices entering hospitals only through research collaborations or clinical trials, thereby hindering the formation of formal purchase orders.

Second, the procurement cycle for large-scale equipment in public hospitals is relatively long. From clinical trials and departmental evaluations to budget approval and public tendering, the process often takes 2–3 years. As high-value medical equipment, surgical robots involve lengthy decision-making chains and cumbersome procedures, resulting in an inherent time lag between installation and revenue realization.

Third, the replacement cycle for clinical operational habits is long. Freehand puncture is a mature technique that has been applied for decades, with physicians' operational experience becoming entrenched and heavily reliant on tactile feedback. Robot-assisted puncture requires the reconstruction of operational workflows, the implementation of systematic academic training, and the accumulation of sufficient case volumes and clinical reputation; industry education and the cultivation of physicians' mindset are inherently long-term processes.

These three factors explain why TrueHealth holds a leading market share but has yet to see its sales revenue scale up. Notably, these constraints are being broken down one by one—especially the key policy bottlenecks, which saw a fundamental breakthrough in 2026.

3Policy Inflection Point Realized, Fee Structure Gradually Integrated

In January 2026, the National Healthcare Security Administration released the "Guidelines for Establishing Price Items for Medical Services in the Category of Surgical and Therapeutic Auxiliary Procedures (Trial)," establishing a unified charging framework at the national level for the first time. The guidelines set up three price items based on the degree of robotic involvement—navigation, participatory execution, and precise execution—and implement a coefficient-based charging model linked to the primary surgery.

Subsequently, multiple regions, including Hunan and Henan provinces, implemented local detailed rules, specifying the fee ranges and surcharge ratios for robot-assisted navigation and auxiliary operations. Hospitals can reasonably recoup procurement costs through compliant medical service fees, thereby forming a closed-loop policy framework characterized by "national guidelines supplemented by local detailed regulations."

What does this mean for TrueHealth? By the end of 2024, the company had placed 26 devices in hospitals on a trial basis. In the past, due to the lack of unified billing categories, hospitals found it difficult to calculate the payback period for purchasing a device—even when trial outcomes were favorable—resulting in insufficient motivation to procure. With clear billing guidelines now in place, hospitals can accurately assess the return on investment timeline for these devices, increasing the likelihood that TrueHealth's trial installations will convert into formal purchase orders.

Therefore, it is widely believed within the industry that the percutaneous puncture surgical robot sector has passed a policy inflection point. This is precisely the core reason why capital markets are willing to assign a high valuation to TrueHealth, despite its current lack of profitability: present losses stem from investments in R&D and channel development, while future performance growth will be driven by both policy implementation and the conversion of installed systems into clinical use.

417 Products Approved, Competition Shifts Toward Differentiation

Once the policy window opens, who can convert installed capacity into revenue the fastest? This depends on strategic positioning advantages within the competitive landscape.

The competitive landscape of the percutaneous puncture robot sector in China has become clearly defined. The National Medical Products Administration (NMPA) has approved 17 products, including 15 domestically produced and 2 imported. Regulatory approval, patent portfolios, and clinical data collectively establish high entry barriers for the industry, making it difficult for small and medium-sized manufacturers to rapidly achieve scalable breakthroughs. TrueHealth and SimpleTouch have secured their positions in the first tier through first-mover advantages and market performance, while companies such as Tuodao Medical are expanding their percutaneous puncture businesses through multi-sector strategic layouts.

Competitive pathways show significant divergence: TrueHealth pursues an integrated, full-stack "puncture + ablation" strategy, boasting the most comprehensive product portfolio, the widest range of regulatory approvals, and the richest clinical data. It serves both high-end tertiary hospitals and grassroots medical institutions while also venturing into frontier sectors such as organ preservation. SimpleTouch focuses on lightweight, single-needle puncture devices, rapidly scaling up to capture the grassroots market. Meanwhile, companies like United Imaging, CuraWay Medical, and EDDA Jixing leverage their imaging ecosystems or differentiated technological approaches to carve out niche markets and establish their foothold.

The industry has moved beyond the rudimentary phase of prototype piloting, with competition shifting to a comprehensive contest encompassing technological implementation capabilities, accumulation of clinical reputation, and end-user channel development. Leveraging its first-mover advantage in regulatory approvals, vast clinical data, and an integrated product portfolio, TrueHealth has established a significant leading position. The key to realizing future performance lies in the pace of hospital tender procurement execution and the ramp-up speed of associated consumables sales.

5Penetrating Grassroots Markets, Expanding the Pipeline, and Anchoring Future Performance Realization

Since its establishment in 2018, TrueHealth has completed multiple rounds of financing, accumulating approximately RMB 640 million in net cash injections, thereby laying a solid foundation for product development and market expansion. With this listing on the Hong Kong Stock Exchange, TrueHealth will focus the raised funds on product iteration, capacity expansion, sales network deployment, pipeline R&D, and replenishing working capital, further addressing its commercialization shortcomings.

Going forward, the company's growth path is clearly anchored in two main strategic pillars: First, leveraging the miniaturized TH-P robot to penetrate the grassroots market. This product has received regulatory approval for commercial launch and has achieved domestic substitution of small robotic arms. Currently, TrueHealth's products are deployed in nearly 100 hospitals, including multiple county-level institutions. Second, expanding the product pipeline, with cryoablation, ex vivo organ preservation, and related consumables all under development, thereby gradually reducing reliance on a single device category.

It is evident that the simultaneous push by TrueHealth and SimpleTouch for listings on the Hong Kong Stock Exchange is not a sign of industry involution, but rather a landmark signal that the percutaneous puncture robot sector has officially transitioned from the technology validation phase to the eve of commercialization. The current low revenue and high losses across the sector represent an inevitable growth stage for hard-tech medical device enterprises; meanwhile, prerequisite conditions such as the implementation of policy-based pricing, the leadership of domestically produced technologies, and the strategic channel positioning of market leaders are gradually taking shape.

For TrueHealth, the most challenging phases—R&D, regulatory approval, clinical trials, and channel development—have already been completed. What remains is simply waiting for the procurement cycle to unfold and for the consumables loop to drive volume growth. As the leading player in puncture robots with the largest market share for three consecutive years, its current valuation premium does not bet on its meager current revenue, but rather on the certain growth trajectory over the coming years as it transforms from a leader in installed base to a dominant force in orders and consumables sales.

An IPO is not the endpoint, but a new starting point for TrueHealth to transition from technological leadership to commercial realization.