Top 5 Chinese ADC pipelines to watch in 2026

Novatim

Innovative Drug Developer for Tumor Immunotherapy

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Innovent

High-end Biologics Developer

Over the past year, ADCs have continued to reshape the oncology treatment landscape with unstoppable momentum.

From a clinical development perspective, according to data from the DXY Insight database, the number of ADC pipeline candidates in global clinical studies has maintained rapid growth, increasing from 113 in 2016 to 498 in 2025. Currently, 40 ADC candidates are undergoing Phase III clinical trials. It is expected that over the next two to three years, these pipeline candidates will successively receive marketing approvals and enter the commercialization stage. Assuming an 80% success rate for Phase III clinical studies of novel anti-tumor drugs, it is estimated that the number of approved ADCs globally could reach 50 within three years. Meanwhile, a substantial number of ADC candidates remain in preclinical and early clinical stages, forming a rich product reserve.

Market size and transaction data further confirm the robust momentum of this therapeutic area. According to data, the ADC market continued to grow rapidly in 2025, with 20 ADC new drugs achieving combined global sales of $16.51 billion, a year-over-year increase of 27%. Six ADC products achieved blockbuster status with sales exceeding $1 billion, including four super-blockbusters with sales surpassing $2 billion. Additionally, according to a research report released by Orient Securities in January 2026, global multinational corporations are accelerating their R&D investment in ADCs. During the 2025–2026 period, total R&D and licensing expenditures in the ADC field by the top five pharmaceutical companies alone are expected to exceed $20 billion, representing approximately 40% growth compared to 2023–2024. These investments are primarily directed toward pipeline expansion, combination therapy development, and acquisition of innovative assets from China.

Concurrently, Chinese ADCs are playing an increasingly significant role, with China gradually emerging as a global technology hub for ADC development. According to data from Southwest Securities, Chinese domestic ADC out-licensing deals in 2025 generated upfront payments totaling $1.63 billion, a year-over-year increase of 676.2%, and total deal value reaching $21.13 billion, a year-over-year increase of 390.6%. Notably, in February 2025, GeneQuantum and its partners out-licensed an ADC candidate targeting FGFR3 along with its technology platform, achieving a total deal value of up to $13 billion—a landmark transaction for 2025 and a historic milestone in Chinese innovative drug out-licensing. Furthermore, companies such as Novatim Immune Therapeutics with its KY-0301 (a nanobody biparatopic ADC), Hengrui Pharma with SHR-A1811, and Innovent Biologics with IBI3009 have also concluded substantial licensing deals. These high-profile transactions signify a fundamental shift: China's core ADC technology platforms are now transitioning "from import to export."

It is evident that against the backdrop of overall pressure on global innovative drug investment, China's ADC field continues to demonstrate resilience and vitality. The growing recognition from multinational corporations confirms that Chinese ADCs have achieved the core competitiveness required to participate in the global first tier. The ADC field has progressed from early-stage technological exploration to a new phase of large-scale commercial application. Standing at this vantage point, how will the ADC landscape evolve in 2026? Based on continuous tracking of industry trends, VCBeat has distilled the following five trend projections.

① 2026 is poised to be a defining year for first-generation IO in combination with ADCs. The Phase III clinical study of sacituzumab tirumotecan, a TROP-2 ADC developed by Kelun-Biotech, in combination with Keytruda for first-line treatment of PD-L1 positive non-small cell lung cancer, is expected to read out detailed data in 2026.

② Multinational corporations are prioritizing next-generation immuno-oncology agents and ADCs in their oncology strategies, with combination therapy development becoming a core focus. Chinese bispecific antibody companies, represented by Akeso and Junshi Biosciences, are deeply integrating into the ADC space through independent research and development as well as licensing collaborations, emerging as leaders in the next-generation immuno-oncology plus ADC field.

③ The development and innovation of China's ADC sector have evolved from "product export" to "technology system export," with platform value gaining global recognition and bargaining power significantly enhanced.

④ The concept that "everything can be conjugated" is driving ADCs to broadly advance toward XDCs, with certain Chinese companies already pioneering DAC (Degrader-Antibody Conjugate) out-licensing.

⑤ Driven by technological breakthroughs, ADC indications will expand from oncology into broader therapeutic areas including immunology, cardiometabolic diseases, and disease diagnostics.

2026: A Defining Year for Next-Generation IO+ADC

The landscape of oncology treatment is undergoing a quiet yet profound transformation.

It is well established that drug resistance remains a major challenge in cancer therapy. Although ADC drugs have significantly improved patient survival benefits, similar to most chemotherapeutic agents, tumors can still develop resistance mechanisms. As monotherapy, ADCs offer limited patient response rates and duration of response, necessitating combination with other anti-cancer therapies. Immunotherapy and ADCs possess naturally complementary characteristics: immuno-oncology agents such as PD-1 inhibitors can activate immune responses but achieve limited response rates; ADCs directly kill tumor cells while releasing tumor-associated antigens and damage-associated molecular patterns, inducing immunogenic cell death, promoting dendritic cell presentation, and ultimately activating CD8+ and CD4+ T cells. This creates synergistic effects with immuno-oncology therapies, achieving enhanced efficacy, overcoming resistance, and prolonging duration of response.

At the 2025 ASCO Annual Meeting, Gilead and MSD jointly presented results from the Keynote-D19 study. This Phase III, open-label, international multicenter clinical trial evaluated the efficacy and safety of sacituzumab govitecan (a TROP-2 ADC) in combination with pembrolizumab versus chemotherapy plus pembrolizumab in patients with previously untreated PD-L1-positive, locally advanced unresectable or metastatic triple-negative breast cancer. Results demonstrated that the "ADC plus Keytruda" combination outperformed "chemotherapy plus Keytruda" in first-line PD-L1 high-expressing triple-negative breast cancer, marking the first demonstration that an ADC is superior to chemotherapy in the context of combination with immuno-oncology therapy.

In November 2025, Kelun-Biotech announced that the Phase III clinical study (OptiTROP-Lung05) evaluating sacituzumab tirumotecan (a TROP-2 ADC) in combination with Keytruda for first-line treatment of PD-L1 positive non-small cell lung cancer had met its primary endpoint at a pre-specified interim analysis for progression-free survival, as confirmed by the Independent Data Monitoring Committee. The study showed statistically significant and clinically meaningful improvement, with a favorable trend observed in overall survival. This represents the first global Phase III study of an ADC combined with an immune checkpoint inhibitor in first-line non-small cell lung cancer to achieve positive results, with detailed data expected to be read out in 2026.

Additionally, AstraZeneca's study of durvalumab in combination with datopotamab deruxtecan (a TROP-2 ADC) head-to-head against Keytruda plus chemotherapy is also expected to read out results in 2026.

It is evident that, from mechanistic complementarity to clinical validation, first-generation immuno-oncology plus ADC combination therapies are crossing the critical threshold from clinical validation to commercial approval. In 2026, with multiple Phase III data readouts occurring in quick succession, the confirmatory evidence for this combination will become more complete, potentially ushering in a new era of cancer immunotherapy. However, competition in the first-generation immuno-oncology plus ADC space is currently intense, with approximately 23 pivotal clinical trials underway globally according to incomplete statistics. Therefore, in 2026, pharmaceutical companies focusing on this field will need to compete not only on clinical data quality but also on clinical development speed.

Next-Generation IO+ADC: Poised to Be Led by Chinese Pharmaceutical Companies

Next-generation immuno-oncology agents (such as PD-1/CTLA-4 bispecific antibodies, PD-1/TIGIT bispecific antibodies, etc.) may more effectively relieve the suppression of the immune system by tumor cells through simultaneous blockade of multiple immune checkpoint pathways, activating a broader range of immune cells (including T cells, NK cells, etc.) to participate in anti-tumor responses. Therefore, as the immuno-oncology component evolves to next-generation agents, the future combination of next-generation IO with ADCs may become a primary direction of exploration in cancer treatment.

Compared to the first-generation IO plus ADC landscape, which represents a shared opportunity for global pharmaceutical companies, the next-generation IO plus ADC wave may be led by Chinese biotech companies.

The 2026 JPM Conference conveyed a clear signal: multinational corporations are prioritizing next-generation IO agents and ADCs in their oncology strategies, with combination therapy development becoming a core theme, and Chinese innovative assets occupying a significant position. For example, MSD has explicitly positioned sac-TMT (sacituzumab tirumotecan), in-licensed from Kelun-Biotech, as a core focus in its oncology development, having initiated 16 Phase III clinical trials. Pfizer will advance five Phase III clinical trials for SSGJ-707 (in-licensed from 3SBio) this year. BNT327 (in-licensed by BioNTech from Biotheus, which has been acquired by BioNTech) will also undergo multiple Phase III clinical trials this year.

It is evident that bispecific antibodies represented by PD-1/VEGF and PD-L1/VEGF have become important research directions for next-generation immuno-oncology, with Chinese companies including Kelun-Biotech, 3SBio, Akeso, Junshi Biosciences, Hengrui, and Innovent extensively participating and advancing these programs into clinical stages.

This "Chinese supply" is not coincidental. Taking Akeso as an example, its ivonescimab demonstrated superiority over pembrolizumab in a head-to-head trial, becoming the first and only drug globally to prove significantly superior efficacy to Keytruda in a monotherapy head-to-head Phase III clinical study, establishing a critical safety foundation for combining bispecific antibodies with ADCs. Akeso's AK146D1, as the world's first Trop2/Nectin4 bispecific antibody-drug conjugate to enter clinical trials, can potentially be combined with its proprietary cadonilimab (a PD-1/CTLA-4 bispecific antibody) or ivonescimab (a PD-1/VEGF bispecific antibody), creating a composite combination strategy of "bispecific ADC plus bispecific IO." This design transcends the simple "IO plus ADC" additive logic, shifting toward a systematic approach to tumor microenvironment modulation through multi-target, multi-mechanism interventions.

Overall, companies such as Akeso and Junshi Biosciences are deeply integrating into the ADC space through independent research and development as well as licensing collaborations, extending the lifecycle of their core immuno-oncology products while sharing in the growth dividends of the ADC field. They also aim to maintain a leading position in the future development of cancer treatment through combinations of bispecific ADCs with bispecific IO or TCE agents.

China's ADC Advantage Shifts from "Cost" to "Technical Value"

Underpinning the emergence of both first-generation IO plus ADC and next-generation IO plus ADC is technological iteration and optimization. Within this context, the development and innovation of China's ADC sector have evolved from "product export" to "technology system export," with platform value gaining global recognition and bargaining power significantly enhanced.

Previously, Chinese ADC novel drug programs offered advantages in development cost and speed, with clinical quality now aligned with global standards, enabling more rapid generation of drugability data. Cost and efficiency advantages serve as the fundamental foundation for Chinese novel drug programs to participate in global competition. For multinational corporations, early-stage assets carry lower prices with manageable trial-and-error costs, allowing for a "buy more, try more" strategy—hence the phenomenon of multinational corporations sourcing ADCs from China.

As Chinese pharmaceutical companies enhance their innovative research and development capabilities, ADC-related licensing transactions from China have exhibited new characteristics:

① Technology platform licensing has become the new normal: Adagene has licensed its SAFEbody antibody platform to Exelixis; Escugen has out-licensed its EZWiFit next-generation ADC platform technology to ConjugateBio; GeneQuantum has entered into a $13 billion collaboration with Biohaven and AimedBio, leveraging its innovative bioconjugation core platform to enable development across multiple targets and 21 ADC candidates.

② Significant platform technology premium is evident: Minghui Pharmaceutical, with its PD-1/VEGF bispecific antibody combination and B7-H3 ADC advancing to Phase III clinical trials, has secured investment from top-tier institutions including OrbiMed and Qiming Venture Partners. Duality Biotherapeutics, relying on its DIBAC next-generation ADC platform, attracted international industry capital including BioNTech during its cornerstone investment round, highlighting the strategic value of platform-based companies.

③ Diversification of transaction targets underscores differentiated value: Hansoh Pharma's CDH17 ADC was licensed to Roche for $1.53 billion; Novatim Immune Therapeutics' nanobody bispecific ADC was licensed to Radiance Biopharma for $1.165 billion. Targets have expanded from traditional HER2 and TROP2 to differentiated targets including CDH17, FGFR3, and DLL3, moving beyond homogeneous competition and significantly enhancing transaction value.

Vertical: Anything Can Be Conjugated; Horizontal: Broad Indication Coverage

Beyond the aforementioned individual breakthroughs, ADCs are broadly evolving in the direction of "anything can be conjugated."

Following the ADC design paradigm, various payloads beyond small molecule chemical drugs can first be conjugated to antibodies. Subsequently, carriers beyond antibodies can be conjugated to various payloads, creating a diverse and expansive library of novel conjugated drugs. This class of novel conjugated drugs is collectively referred to as XDCs, where X represents the carrier, D represents the payload, and C represents the conjugate.

Globally, there are over 10 types of XDCs in the research and development stage. Antibody-radionuclide conjugates, or RDCs, have already been approved for marketing. Other formats, including antibody immunostimulant conjugates, antibody oligonucleotide conjugates, degrader-antibody conjugates, and peptide-drug conjugates, remain in early-stage development.

Notably, in January 2026, HealZen announced a global partnership with a U.S.-based biotechnology company for a DAC asset. Significantly, this represents China's first DAC asset out-licensing transaction. Beyond HealZen, which achieved this pioneering deal, several other Chinese companies including CSPC Pharmaceutical Group, Kangpu Biopharmaceuticals, FenDi Pharmaceutical, Immunwork, Fapon Biopharma, and Xiling Lab have also established DAC programs, all currently in the preclinical stage.

In the future, the diversity of XDCs will enable the expansion of indications beyond traditional ADC applications in oncology into broader therapeutic areas including immunology, cardiometabolic diseases, and disease diagnostics, further amplifying the value of these technology platforms.

Top 5 ADC Pipelines in China to Watch for in 2026

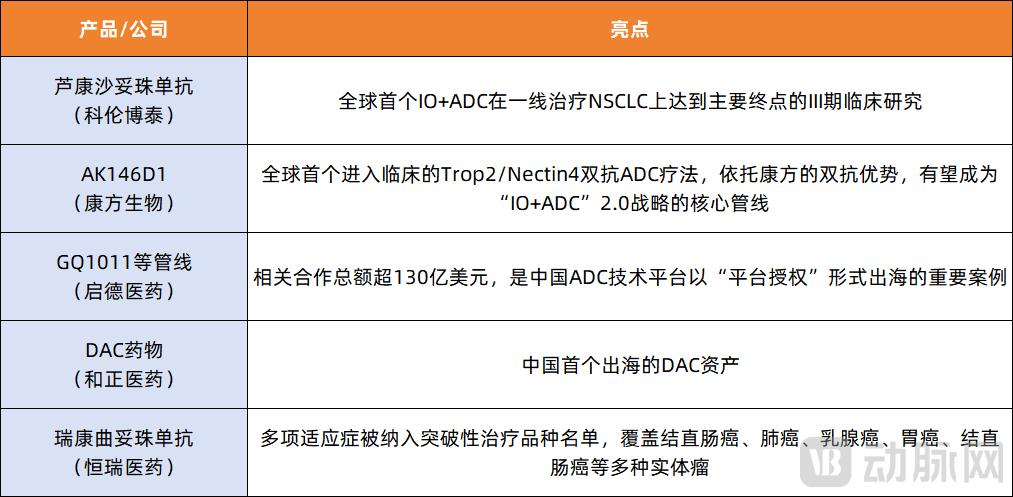

Based on the aforementioned dimensions, which five Chinese pipelines in the ADC field merit attention in 2026? Due to space limitations, one representative Chinese pipeline has been selected for each dimension (first-generation IO+ADC, next-generation IO+ADC, technology platforms, XDC, and indication expansion), listed in no particular order: