After 13 years of no new drugs, gout innovation drugs take off: Firsekibart and Dotinurad spearhead the market, as the first China-made URAT1 inhibitor secures approval

GenSci

Gene Engineering Pharmaceutical and Growth Hormone Producer

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

ApicHope

Innovative Biopharmaceutical R&D Developer

The market for innovative gout therapeutics is beginning to yield commercial returns, delivering its first commercial performance report.

Based on market feedback, two approved innovative drugs for gout have begun to ramp up sales — namely, Eisai's Dotinurad (Youlesi®) and GenSci's Firsekibart (Jinbeixin®).

Dotinurad is a highly selective urate transporter 1 (URAT1) inhibitor indicated for patients with gout and hyperuricemia. Less than a year after its launch on JD Health, its sales volume has already exceeded 80,000 units.

Firsekibart, approved in China in June 2025, is the world's first IL-1β monoclonal antibody for acute gout attacks. As a therapeutic biologic, it features precise and long-acting anti-inflammatory effects and is priced at RMB 9,000 per injection. During its earnings briefing, GenSci reported that Jinbeixin's revenue surged quarter-on-quarter in Q1 2026. GenSci expects Firsekibart to become "the next growth hormone," unlocking a market worth tens of billions of US dollars.

China accounts for 38% of the global gout patient population, making it a key market for gout therapeutics. However, the gout pharmaceutical market is challenging to navigate; its overall scale is relatively limited and has been further compressed by drug price reductions driven by centralized procurement. Consequently, China's gout drug market size has contracted from $500 million in 2019 to $300 million in 2024.

In China, the innovative gout drug market is fiercely competitive. In the URAT1 inhibitor segment, Hengrui Pharma's Class 1 innovative drug Ruzinurad has received marketing approval. Next-generation URAT1 inhibitors from pharmaceutical companies such as ApicHope and New Element Pharma have already entered late-stage development. How will the two innovative drugs — Dotinurad and Firsekibart — achieve commercial scale-up? What implications do they hold for the market?

In recent years, the disease burden of hyperuricemia and gout in China has grown increasingly severe, exhibiting a clear upward trend and a shift toward younger age groups. It has now emerged as another common metabolic disease following diabetes.

The growth rate of China's gout patient population significantly outpaces the global market. According to the prospectus of New Element Pharma, the global number of gout patients stood at 66.2 million in 2024, with a five-year compound annual growth rate (CAGR) of 4.4%; in China, the patient population reached 25.3 million, with a five-year CAGR of 10.7%. Notably, nearly 60% of patients with hyperuricemia and gout fall within the 18-to-35 age group.

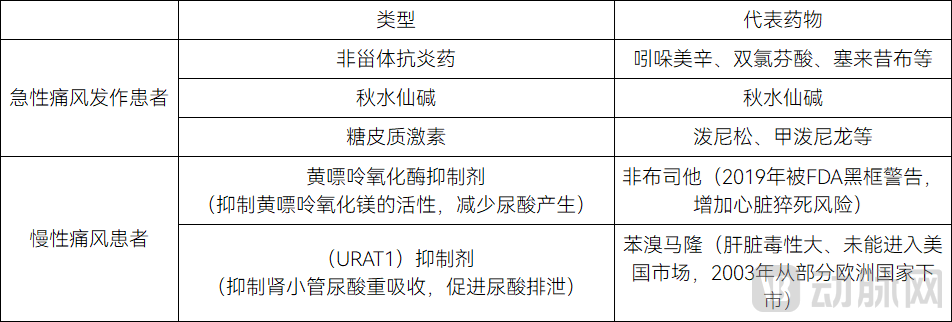

The most commonly used drugs in the treatment of gout are primarily classified into two major categories based on therapeutic objectives:

① Anti-inflammatory and analgesic drugs are aimed at rapidly relieving symptoms such as redness, swelling, heat, and pain during acute flares. These include three classes of analgesic medications for the acute phase of gout — colchicine, nonsteroidal anti-inflammatory drugs (NSAIDs), and glucocorticoids — as well as the recently approved Firsekibart.

② Uric acid-lowering drugs aim to lower serum uric acid levels and prevent uric acid crystal deposition, thereby fundamentally reducing recurrence and dissolving tophi. Uric acid-lowering drugs are primarily classified into two major categories: inhibitors of uric acid synthesis and agents that promote uric acid excretion.

Primary Medications for Gout

Firsekibart is an innovative drug for the treatment of acute gout. Firsekibart belongs to the anti-inflammatory and analgesic class and is the first approved IL-1β monoclonal antibody in China. It is indicated for acute gouty arthritis attacks in adults who are contraindicated to, intolerant of, or have an inadequate response to nonsteroidal anti-inflammatory drugs (NSAIDs) and/or colchicine, and for whom repeated corticosteroid use is not appropriate.

The IL-1β target is implicated in numerous diseases, and GenSci was the first to identify the overlooked market opportunity in gout. Common diseases mediated by IL-1β include rheumatoid arthritis, gout, diabetes, and osteoarthritis. When developing therapeutics targeting this pathway, GenSci initially focused on drug development for juvenile idiopathic arthritis, a globally prioritized indication. During subsequent development, GenSci identified IL-1β as the core mediator of gout-related pain.

Overseas pharmaceutical companies have not prioritized the gout indication, instead directing their development efforts toward cardiovascular diseases and oncology. However, China has a high prevalence of gout and faces significant unmet clinical needs. Driven by this insight, GenSci decided to prioritize the development of the gout indication, securing a first-mover advantage in the market. In June 2025, Firsekibart became the first IL-1β monoclonal antibody approved for acute gouty arthritis.

Firsekibart did not experience an immediate market surge upon launch. The high price posed the greatest challenge to its commercialization. Although a single administration of Firsekibart reduces the risk of relapse by 90% at 12 weeks and 87% at 24 weeks post-dose, requires dosing only once every six months, and its long-acting anti-inflammatory mechanism delivers sustained benefits to the joints, cardiovascular system, kidneys, and other systems, the price of nearly RMB 10,000 per vial and an annual treatment cost of at least RMB 20,000 pose the primary barrier to its commercialization. While the premium pricing reserves strategic room for subsequent national medical insurance negotiations, it impedes early market promotion.

Another major challenge is the insufficient awareness among gout patients regarding anti-inflammatory therapy. Chinese gout patients have long been educated to prioritize "urate-lowering" as the core treatment objective, resulting in insufficient awareness of targeted anti-inflammatory therapy during acute flares and routine inflammation management. As an anti-inflammatory and analgesic agent, Firsekibart must break through the established treatment paradigm to successfully penetrate the market.

To break through this bottleneck, GenSci has stepped up its promotional and market education efforts. Strategically, GenSci has positioned Firsekibart as a key product to break its reliance on a single blockbuster growth hormone, and as a pivotal move in its strategic transformation, has invested substantial resources in its promotion.

In terms of market education, GenSci focuses on highlighting the analgesic and relapse-preventive properties of Firsekibart, addressing the core pain points of patients during acute episodes, and emphasizing the clinical benefits of its targeted anti-inflammatory action.

At the pricing and market access level, GenSci adopted a flexible strategy to offset the market resistance caused by high pricing. During the initial launch phase, an "early-bird subsidized price" was introduced to lower the barrier to first-time purchases. To mitigate purchasing concerns arising from inter-patient variability in therapeutic efficacy, GenSci previously launched a campaign offering a complimentary dose if recurrence occurs within six months, encouraging more patients to try the new therapy. Meanwhile, GenSci is also actively advocating for the inclusion of Firsekibart in the medical insurance reimbursement list.

In terms of channel strategy, GenSci is simultaneously advancing offline hospital coverage and online digital marketing. The company has established strategic partnerships with platforms such as JD Health and AliHealth, leveraging out-of-hospital channels to reach younger patient demographics, thereby forming a comprehensive omni-channel coverage network.

Early-stage market education and channel development have begun to yield initial results, with the commercialization of Firsekibart gaining momentum in Q1 2026. During GenSci's earnings briefing, it was noted that Jinbeixin's Q1 revenue experienced a substantial quarter-on-quarter increase compared to Q4. The preliminary market education has laid a solid foundation for product promotion, and the drug's therapeutic efficacy has gained growing recognition from both physicians and patients.

Dotinurad is an innovative drug for the treatment of chronic gout. Dotinurad, however, is rapidly expanding its market presence by leveraging its safety advantages and broad accessibility. Eisai's commercialization strategy for dotinurad can be summarized as a multi-pronged approach of "differentiated clinical positioning + rapid commercial rollout + swift medical insurance inclusion." The core objective is to capture as much market share as possible prior to the launch of Chinese-made competing products, thereby establishing a brand barrier.

In terms of clinical positioning, dotinurad is the first highly selective URAT1 inhibitor approved in China. Eisai positions it as a next-generation uricosuric agent following benzbromarone. Its core selling point is superior efficacy and a higher safety profile; studies indicate it has minimal impact on liver function, with no significant hepatotoxic adverse effects. According to clinical data, a Phase III trial in China demonstrated that after 24 weeks of treatment with 4 mg dotinurad, the serum uric acid target attainment rate (≤360 μmol/L) reached 73.6%, significantly higher than the 38.1% observed in the 40 mg febuxostat group.

A major strategy in the promotion of dotinurad is trading price for volume to rapidly capture market share. Leveraging Eisai's robust and well-established distribution network, dotinurad was prescribed simultaneously in Beijing and Shanghai on the first day following its approval, with market availability across multiple regions in China within 72 hours, ensuring a highly efficient commercial launch. Regarding pricing strategy, Eisai swiftly advanced dotinurad's inclusion in the national medical insurance program. Just one year post-approval, the drug was incorporated into medical insurance coverage, substantially lowering patients' out-of-pocket burden. Since the implementation of the 2026 medical insurance reimbursement policy, patient reports indicate that the out-of-pocket cost for dotinurad (20 mg × 14 tablets/box) stands at merely RMB 23.36 after reimbursement.

The rationale behind adopting an affordable pricing strategy is, in part, driven by Eisai's assessment that China has a massive base of hyperuricemia patients, with the prevalence of hyperuricemia and gout continuing to rise and the age of onset shifting younger. The financial burden of long-term, standardized treatment remains a key bottleneck limiting patient benefits. A price-for-volume strategy can accelerate market penetration and expand patient coverage.

On the other hand, the URAT1 inhibitor pipeline landscape is facing intensifying pressure from domestic candidates, with at least ten currently in clinical development. The recent approval of Hengrui Pharma's Class 1 new drug Ruzinurad has further compressed the commercial lifecycle of innovative therapeutics. As the market exclusivity window for dotinurad continues to narrow, it is imperative to race against time and maximize its market momentum within this limited period of exclusivity.

The price-for-volume strategy has received positive feedback from the market. Based on online channel performance, dotinurad has grown rapidly. In May 2026, dotinurad's sales volume on JD Health increased by approximately 33% month-on-month.

Firsekibart and Dotinurad are spearheading the charge, with several other promising pipeline candidates poised to enter the innovative gout therapeutics market. The gout market is on the verge of its most intense transformative phase.

The innovative gout drug market is witnessing intense competition, primarily centered on URAT1 inhibitors. Novel domestic gout therapeutics are focusing on the R&D of next-generation URAT1 inhibitors. By employing strategies such as molecular structure optimization and the development of long-acting formulations, they aim to improve drug safety and efficacy.

Multiple domestic gout therapeutic pipelines have entered late-stage clinical development. Hengrui Pharma's Ruzinurad, the first approved China-produced URAT1 innovative drug, demonstrated an sUA target achievement rate of 56.9% in its Phase III clinical data. Approved for market launch on May 28, 2026, it has secured a first-mover advantage. Hengrui Pharma holds strong channel influence in the gout market. With Hengrui's febuxostat approved for launch in China in 2013 and maintaining a leading market share, its robust channel control capabilities will undoubtedly facilitate the commercialization of Hengrui's new gout drug.

ApicHope's AR882 achieves an 89% target rate at 12 months and effectively dissolves tophi, drawing widespread attention. ApicHope disclosed that a superiority trial comparing AR882 against febuxostat, a first-line clinical therapy, has been designed in China. Based on currently available trial data, the product demonstrates superior efficacy compared to competing drugs in its class. Global multicenter and domestic Phase III clinical trials are progressing steadily. The clinical phase of AR882 is expected to conclude by mid-2026. Upon completion of data compilation and reporting, a New Drug Application (NDA) will be submitted. Following successful submission, the NDA review process is anticipated to take approximately 12 to 15 months. The earliest potential market launch in China could be late 2027 or early 2028.

New Element Pharma's ABP-671 demonstrates an outstanding safety profile. ABP-671 features a unique chemical structure that avoids the benzofuran scaffold commonly found in traditional drugs (e.g., benzbromarone), thereby preventing the formation of toxic metabolites associated with liver injury and reducing the risk of hepatotoxicity. In terms of safety, no serious adverse events (SAEs) were reported, and there were virtually no Grade 3 treatment-emergent adverse events (TEAEs); events were generally mild and comparable across groups, with no hepatic or cardiovascular safety signals observed. In terms of efficacy, clinical data demonstrated that after just 4 weeks of dosing, 100% of subjects achieved the target sUA level (<6.0 mg/dL), regardless of whether the regimen was 4 mg BID or 8 mg QD.

ABP-671 is also the core product driving New Element Pharma's IPO push. The drug has entered into a partnership with China Medical System (CMS), whereby CMS will pay upfront and milestone payments to secure exclusive CSO commercialization rights for the product in the Chinese market.

With the launch of multiple drugs sharing the same indication and target, it is foreseeable that the innovative gout drug market will undoubtedly be highly competitive over the next two years. Furthermore, as Eisai's dotinurad has been included in the national medical insurance list, the price anchor it establishes will exert pricing pressure on domestic pharmaceutical companies. Products that demonstrate strong differentiation in safety and clinical value will be better positioned to capture a larger market share.