Bispecific antibodies surge: how a potential BIC candidate challenges for the next ophthalmology blockbuster

Innovent

High-end Biologics Developer

NovaBridge Biosciences

Biological Agent Developer

The ophthalmology market is undergoing a major transformation.

In 2025, Roche's VEGF-A/Ang-2 bispecific antibody, Vabysmo (faricimab), achieved sales of CHF 4.1 billion (approximately USD 5.36 billion), becoming the fastest-growing star product in the ophthalmology market and the world's second-best-selling bispecific antibody.

At this pace, Vabysmo is expected to surpass USD 10 billion in sales within three years. In comparison, the current ophthalmology blockbuster, Aflibercept, took a decade to reach its historical peak of USD 9.647 billion in 2022, after which its growth stagnated and gradually declined under the impact of bispecific antibodies.

With non-inferior efficacy to the ophthalmology sales leader Aflibercept, coupled with a longer injection interval, Vabysmo is regarded as the front-runner to become the next ophthalmology blockbuster. This fully demonstrates the clinical value and commercial potential of the dual-target strategy in the field of fundus treatment.

Of course, pioneers are often the primary target for later entrants seeking to disrupt the market, especially against the backdrop of formidable challengers, making this competition particularly intense.

Not long ago, Innovent Biologics disclosed head-to-head clinical data for its IBI324, issuing a direct challenge to Roche. Meanwhile, NovaBridge Biosciences' VIS-101, with its novel molecular design, has joined the fray and is poised to become the world's second marketed VEGF-A/Ang-2 bispecific antibody. Its disclosed preliminary clinical data are highly competitive, particularly regarding its potential 24-week injection interval, demonstrating a superior patient compliance solution and highlighting its best-in-class potential.

From monoclonal antibodies to bispecific antibodies, from multinational giants to innovative biotech companies, a competition centered on extended duration, patient compliance, and therapeutic innovation is now in full swing within the hundred-billion-dollar blue ocean of the ophthalmology market. Later entrants, represented by companies such as Innovent Biologics, RemeGen, NovaBridge Biosciences, and YZY MED, are stepping onto center stage with an unprecedented proactive stance.

A New Blue Ocean in a Red Sea: Bispecific Antibody Therapy Reshapes the Ten-Billion-Dollar Market Landscape

Ophthalmology, a seemingly niche specialty, has nurtured a ten-billion-dollar "blockbuster" by virtue of its vast patient population and well-defined clinical needs.

In recent years, driven by the rising prevalence of eye diseases and increased health awareness among the population, the global ophthalmic drug market has continued to grow. According to public data, the global ophthalmology market size was USD 77.1 billion in 2024 and is expected to reach approximately USD 144 billion by 2034. Fundus diseases, such as wet age-related macular degeneration (wAMD) and diabetic macular edema (DME), represent significant growth drivers in the ophthalmology market.

DME and wAMD are the leading causes of vision loss among working-age populations and the elderly, respectively. The global patient population affected by these conditions numbers in the tens of millions, creating a mature and continuously expanding market. In China alone, the existing and newly diagnosed patients with wAMD and DME exceed 15 million, with approximately 600,000 new cases added annually.

The core pathological mechanism of these fundus diseases is closely associated with vascular endothelial growth factor (VEGF). Therefore, anti-VEGF therapy is the primary treatment approach for fundus diseases. Although multiple anti-VEGF monoclonal antibodies (such as Aflibercept and Ranibizumab) have been on the market for years, their inherent limitations and the unmet clinical needs they leave behind are equally prominent, providing room for a "value reconstruction" across the entire field.

First, there is an urgent patient need for longer dosing intervals and improved treatment experiences. Anti-VEGF drugs require intravitreal injections monthly or every two months. The long-term, frequent invasive procedures impose significant physical, psychological, and financial burdens on patients, leading to real-world treatment adherence that is far below clinical trial levels and substantially diminishing long-term vision benefits. The CATT study and its subsequent long-term follow-up data revealed that after initial visual gains, treated patients often experience a secondary decline in vision within five to seven years. Furthermore, approximately 30-50% of patients show inadequate response to existing drugs, indicating a clear efficacy bottleneck.

Particularly in the long-term management of fundus diseases, the frequent intraocular injections lead to significantly reduced patient compliance, which adversely affects prognosis and represents the greatest challenge in treatment. Consequently, extending the dosing interval has become the core driver for iterative innovation in ophthalmic products.

Second, there is the emergence of drug resistance and pathological escape. Solely inhibiting VEGF-A can induce compensatory mechanisms in the body, leading to elevated levels of other angiogenic factors and inflammatory cytokines such as IL-6, ultimately diminishing the long-term efficacy of the drug and potentially causing disease progression. This represents a scientific critical point that urgently needs to be addressed.

Roche's Vabysmo (faricimab) pioneered a "dual-target" solution. By simultaneously blocking the VEGF-A and Ang2 (angiopoietin-2) pathways, it not only inhibits neovascularization and leakage while stabilizing blood vessels and reducing inflammation, but also extends the dosing interval to once every four months.

This explains why, despite demonstrating non-inferior efficacy to Aflibercept in multiple Phase III studies for DME and nAMD, it achieved blockbuster sales immediately upon launch. In just four years, its global sales surpassed USD 5 billion, with a formidable growth trajectory.

At this pace, it will soon surpass Aflibercept to become the new "blockbuster" in ophthalmology. This fully validates the clinical value and commercial potential of the dual-target strategy in the field of fundus treatment, positioning it as the core of the next phase of competition in the fundus disease field and continuously reshaping the existing treatment landscape.

In other words, the seemingly red ocean of the ophthalmology field actually harbors a value blue ocean centered on transitioning from monthly injections to quarterly or even longer intervals. This has rapidly intensified interest in the ophthalmic bispecific antibody field, with later entrants accelerating their strategic deployment.

Competing for the Blockbuster: Differentiated Design of Next-Generation Molecules and the Pursuit of Best-in-Class

When the evolutionary direction of a therapeutic field becomes clear, the essence of competition reverts to the deep exploration of underlying technologies and keen insights into clinical nuances. In the race for ophthalmic bispecific antibodies, how can next-generation molecules outperform the pioneer, faricimab? A multi-pronged "challenge" is underway.

Innovent Biologics' IBI324 aims to leverage a smaller protein molecular structure to achieve higher molar dose administration, laying the groundwork for extended treatment intervals, and has demonstrated competitiveness in early head-to-head clinical trials. Meanwhile, RemeGen is targeting the innovative VEGF/FGF pathway, seeking to explore a novel dual-target strategy.

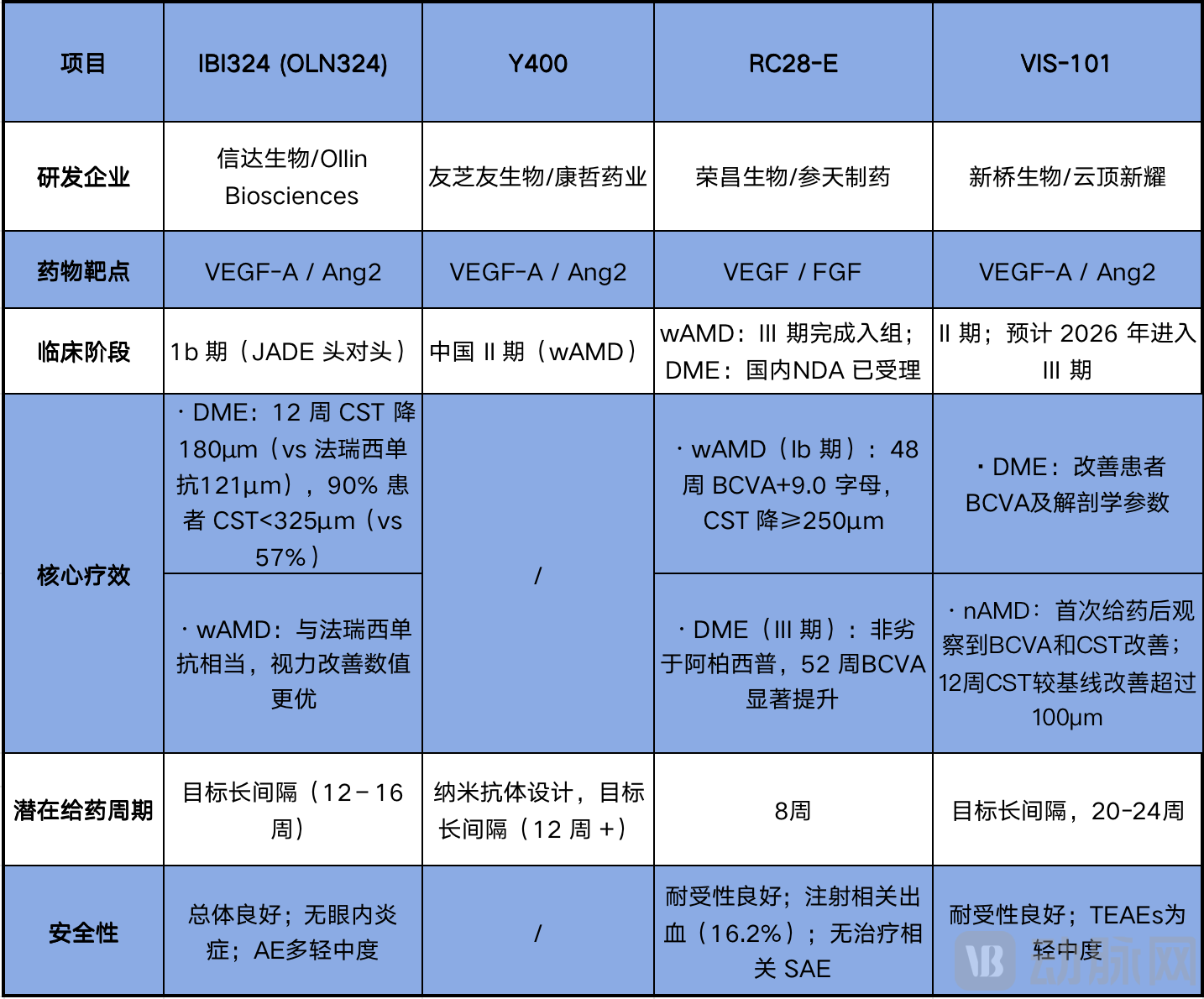

Comparison of New Generation Ophthalmic Bispecific Molecules

VIS-101's competitive edge stems from its next-generation molecular architecture. As the most advanced VEGF-A/Ang-2 bispecific antibody in development following Vabysmo (faricimab), VIS-101 employs a unique tetravalent molecular structure that confers stronger binding and blocking activity against VEGF and Ang-2.

Compared to the benchmark product, VIS-101 demonstrates a 2-fold and 6-fold increase in binding activity against VEGF and Ang-2, respectively; its inhibitory activity is increased by 2-fold and 16-fold, respectively. This suggests it can achieve stronger vascular stabilization, reducing leakage, neovascularization, and inflammation, with the potential to enhance efficacy while extending dosing intervals, decreasing frequent intraocular injections, and improving patient compliance.

This meticulous, fundamental molecular design has translated directly into impressive Phase I clinical data. In the treatment of DME patients, VIS-101 administered via intravitreal injection every four weeks at doses up to 6 mg demonstrated good tolerability and improved patient best corrected visual acuity (BCVA) and anatomical parameters. Following loading doses, the potential for long-interval dosing with VIS-101 was preliminarily observed, with 100% of subjects maintaining a 16-week dosing interval.

In nAMD patients, the treatment was also well-tolerated. Not only were rapid improvements in BCVA and anatomical parameters observed, but treatment frequency was also significantly reduced. After only three loading doses, 78% of patients achieved a treatment interval of ≥12 weeks following the last loading dose, with 44.4% of patients maintaining an interval exceeding 24 weeks.

All this potential points to a core value: extended duration of action. It pushes the possibility of "once every 8-16 weeks" pioneered by Vabysmo (faricimab) towards a future of "once every 20-24 weeks," demonstrating best-in-class potential.

Furthermore, unlike Vabysmo which is primarily indicated for treatment-naïve patients, VIS-101 is also effective in previously treated nAMD patients, expanding its potential applicable population with highly competitive efficacy signals.

Overall, through its specialized bioengineering design, VIS-101 possesses enhanced target neutralization capacity, promising to deliver a novel treatment paradigm for patients. Coupled with its globally leading clinical development pace and the combined efforts of NovaBridge Biosciences and Everest Medicines in advancing the program, VIS-101 is well-positioned to break through in future competition.

The Next Highlight: Why Bispecific Antibodies Are a More Practical Solution Than Gene Therapy

The technological evolution in the ophthalmology field is advancing at a rapid pace. Amidst the surging wave of bispecific antibodies, another potentially more disruptive force for innovation—gene therapy—has also arrived on the scene.

In the third quarter of 2025, Eli Lilly acquired Adverum for up to USD 262 million, securing Ixo-vec, a gene therapy for the treatment of wet age-related macular degeneration (wAMD). The underlying logic behind this move is a bets on the transformative shift in wAMD treatment from "lifelong therapy" to "one-time cure."

Major pharmaceutical companies such as Otsuka Pharmaceutical, Regeneron, and AbbVie are also making substantial investments in multiple AAV gene therapies for common ophthalmic diseases including wAMD and DME. Theoretically, this represents the most perfect solution, yet the significant challenges lurking beneath the surface cannot be ignored.

The first is long-term safety risk. Once an AAV vector enters the human body, can long-term, unknown risks of inflammation or immune activation be completely avoided? Some AAV therapies have already revealed safety concerns in fields such as hematology and neurology. The relatively "immune-privileged" nature of the eye mitigates the risk, but it does not eliminate it entirely.

Second, there are the high costs and commercialization challenges. The research, development, and manufacturing processes for AAV gene therapies are extremely complex and costly, implying that launch prices could reach up to millions of dollars. For common diseases with large patient populations like AMD and DME, integrating such high-priced drugs into mainstream national health insurance systems presents a commercial challenge as formidable as the scientific exploration itself.

Against this backdrop, next-generation ophthalmic bispecific antibodies represented by VIS-101 and IBI324 play the role of an "optimal practical solution." Compared to traditional monoclonal antibodies requiring lifelong frequent injections, they achieve a dual enhancement in both efficacy and compliance: fewer loading doses and longer treatment intervals. This means they significantly improve patient treatment outcomes and reduce treatment burden, while simultaneously circumventing the long-term safety and commercialization risks associated with gene therapy.

More importantly, the hundred-billion-dollar growth story of Aflibercept and the current explosive trajectory of Vabysmo have already demonstrated to the world that innovative ophthalmic therapies with breakthrough clinical value, particularly those extending dosing intervals, can stand out in fierce competition and become "mega-blockbusters" leading the market.

This will define the competitive battleground for next-generation ophthalmic bispecifics. Of course, this places higher demands on later entrants. Beyond efficacy and safety, global clinical development capabilities are also crucial. After all, in innovative drugs, speed is paramount.

In this regard, VIS-101 has also demonstrated strong competitiveness. Visara, a subsidiary of NovaBridge Biosciences, is vigorously advancing the clinical research of VIS-101, led by Dr. Emmett J. Cunningham, Jr., co-founder and Executive Chairman. Over the past 25 years, Dr. Cunningham has served as a physician, innovator, entrepreneur, and investor. He was previously a Senior Managing Director at Blackstone and a Managing Director at Clarus Ventures. Dr. Cunningham is also an internationally recognized expert in infectious and inflammatory eye diseases, with over 450 co-authored academic papers to his name. With exceptional clinical expertise and senior management experience at top-tier global investment institutions, Dr. Cunningham has established a high level of professional credibility and extensive industry recognition in the field of global biopharmaceutical R&D and investment.

This signifies that NovaBridge Biosciences is leveraging top-tier R&D expertise to increase the probability of success in drug development. As the release of Phase II data for VIS-101 approaches, if subsequent data remain consistently positive, it will usher in another highlight moment for the company, following Givastomig.

This will also constitute a highlight moment for the ophthalmic bispecific antibody field, demonstrating that in this second wave of technological advancement, next-generation molecules are continuously driving the iterative evolution of treatment paradigms, bringing longer-acting and superior treatment options to ophthalmology patients worldwide.