ASCO 2026: Alpha radionuclides ignite! From β to α — China's radiopharmaceuticals seize the global momentum

At the globally most anticipated ASCO 2026 Annual Meeting, immunotherapy, ADCs, and bispecific antibodies continue to dominate the headlines, but one relatively niche yet highly technically demanding hard tech sector was repeatedly highlighted—radiopharmaceuticals, i.e., Radioligand Therapy (RLT) and the closely related Radionuclide Drug Conjugate (RDC).

Radiopharmaceuticals use a "guide molecule" (ligand, commonly a small molecule or peptide targeting PSMA or SSTR2) conjugated to a radionuclide (e.g., ¹⁷⁷Lu or ²²⁵Ac), allowing the guide molecule to deliver radiation directly adjacent to tumor cells to trigger localized cell destruction, thereby minimizing damage to healthy tissues. If labeled with an imaging radionuclide (e.g., ⁶⁸Ga, ¹⁸F), the drug acts as a "diagnostic probe" that can "light up" the tumor on PET-CT; if labeled with a therapeutic radionuclide (such as ¹⁷⁷Lu, ²²⁵Ac, or ⁹⁰Y), the drug becomes a "therapeutic warhead." For the same target, the integrated "diagnose first, then treat" pathway is known in the industry as theranostics—the key feature distinguishing radiopharmaceuticals from chemotherapy, targeted therapy, and immunotherapy.

At ASCO 2026, the core narrative for radiopharmaceuticals is that as RLT transitions from beta- to alpha-emitting radionuclides, theranostics targeting PSMA and SSTR2 continue to advance. The strategic direction set for global RLT at ASCO serves as the optimal benchmark for evaluating catch-up opportunities in China's radiopharmaceutical and RDC sectors.

1From β-Radionuclides to α-Radionuclides: Physical Properties Dictate Therapeutic Logic

To understand the positioning of China's radiopharmaceutical sector, one must first clearly discern the signals sent by the global benchmark at ASCO 2026. Novartis presented over 65 abstracts at ASCO 2026, among which the two related to radiopharmaceuticals are the most noteworthy:

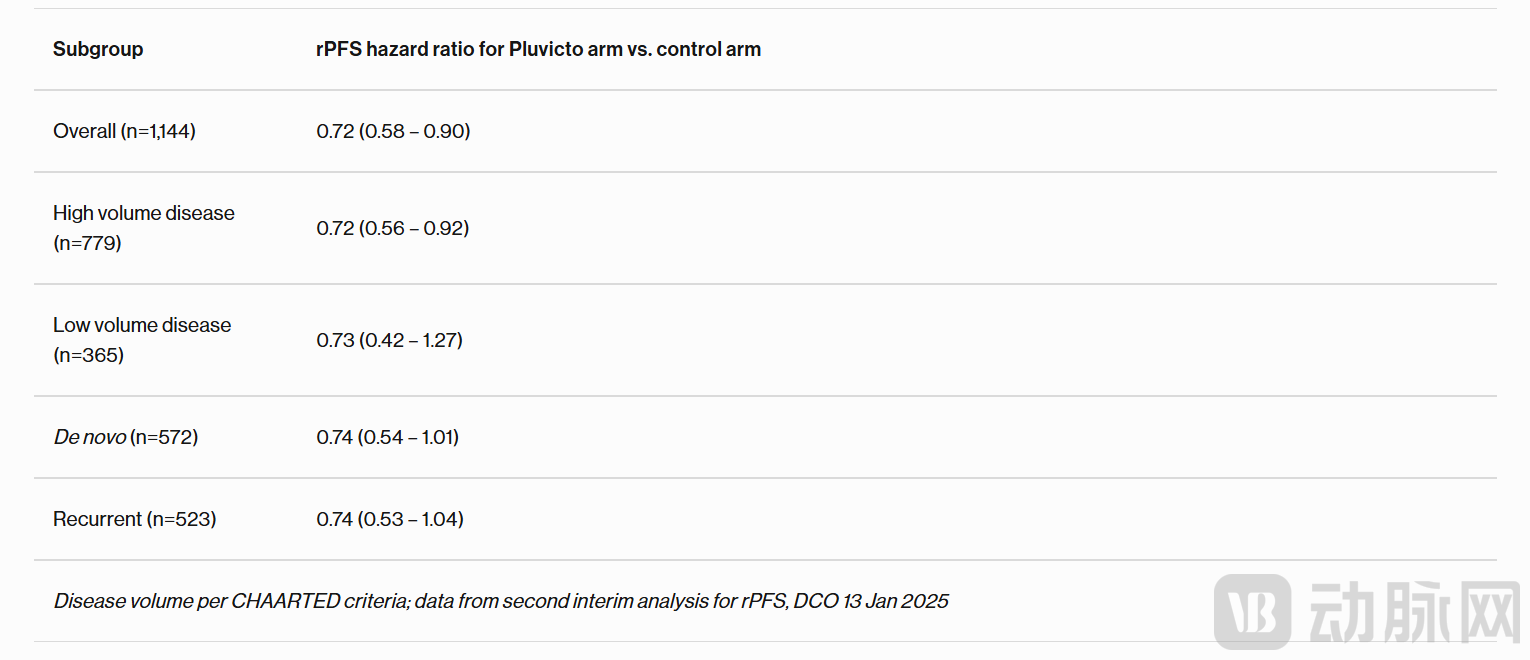

The first item is the PSMAddition oral presentation on Pluvicto (177Lu-PSMA-617)—demonstrating efficacy stratified by disease volume. Pluvicto is the first approved PSMA-targeted 177Lu radioligand therapy, which was previously approved for later-line treatment of metastatic castration-resistant prostate cancer (mCRPC).

This PSMAddition study explores the application of Pluvicto in earlier lines of therapy and indication expansion—stratified by disease burden and subgroup analysis in newly diagnosed or relapsed metastatic hormone-sensitive prostate cancer (mHSPC). Specifically, disease burden stratification refers to categorizing patients into "high tumor burden" and "low tumor burden" groups based on the number and extent of metastatic lesions, to evaluate differences in treatment efficacy, and to analyze the tolerability and benefit profiles of different patient subgroups in response to radiation doses.

Data demonstrate that Pluvicto plus standard of care (SoC) compared with SoC alone shows sustained improvement in radiographic progression-free survival (rPFS) across key subgroups of patients with PSMA-positive mHSPC. Subgroup analyses evaluated outcomes by disease volume (high or low) and disease presentation (de novo or recurrent mHSPC)—Pluvicto exhibited similar rPFS improvements across key subgroups, consistent with the previously reported primary endpoint, which indicated a 28% reduction in the risk of radiographic progression or death (HR 0.72; 95% CI: 0.58, 0.90). The secondary endpoint of disease progression also remained consistent.

Based on the PSMAddition results, Novartis has submitted regulatory applications in the United States, China, and Japan, with initial regulatory decisions expected in the second half of 2026.

The second item is the first-in-human 225Ac-PSMA (alpha radionuclide) dose-escalation results — representing Novartis's first-in-human data for an 225Ac-based alpha radioligand therapy targeting mCRPC. In the Phase I AcTION trial, the therapy demonstrated reductions in prostate-specific antigen (PSA) levels and radiographic responses, with a manageable safety profile. These findings support continued clinical development in patients with PSMA-positive mCRPC. Notably, the patient inclusion criteria allowed enrollment regardless of prior [177Lu]Lu-PSMA radioligand therapy, suggesting that novel alpha-emitting radionuclide therapies hold promise as a differentiated complement to frontline beta-emitting radiopharmaceuticals, potentially facilitating rapid market entry through later-line complementary therapy.

These two data points point to the same industry trend: RLT is transitioning from the beta-emitting radionuclide (177Lu) era to the alpha-emitting radionuclide (225Ac) era. The underlying logic is determined by the physical differences between the two types of radionuclides —

Beta-emitting radionuclides represented by 177Lu emit beta particles: they have a relatively long range (penetrating approximately 2 mm in tissue, equivalent to the distance across dozens to hundreds of cells) and relatively low energy per particle. The advantage lies in the large "coverage" of radiation: for tumor tissues with heterogeneous target expression, the "crossfire" effect can reach nearby cancer cells that are not precisely targeted. The drawback is that surrounding normal cells may also be affected to a certain extent.

Alpha-emitting radionuclides represented by 225Ac emit alpha particles: they have an extremely short range (only a few cell diameters, approximately 50–100 μm), but each particle carries extremely high energy, and their destructive power in inducing DNA double-strand breaks is far greater than that of beta radiation. This means that the cell-killing effect of alpha-emitting radionuclides is more "potent" yet more "precise" — it is activated only in the localized area where targeting molecules bind, minimizing impact on surrounding normal tissue.

Given that Pluvicto has validated the "PSMA target + RLT targeting" logic, switching the warhead from beta- to alpha-emitting radionuclides capable of more precise targeted cell killing is regarded by the industry as a key direction for next-generation radiopharmaceuticals. However, alpha radionuclides impose significantly higher requirements on manufacturing, distribution, dosimetry, and safety windows. The first-in-human data from global radiopharmaceutical giant Novartis serves as the starting point for addressing these challenges.

Meanwhile, alpha-nuclide therapies from Chinese innovative pharmaceutical companies also made their debut at ASCO 2026 — clinical data for the novel alpha-particle radioligand therapy XTR022 ([225Ac]Ac-XT381), independently developed by Sinotau Pharmaceuticals, were presented in poster format.

This study aims to evaluate the safety, tolerability, and preliminary efficacy of XTR022 in previously treated, PSMA-positive mCRPC subjects. Among the 13 subjects with at least one post-treatment PSA assessment, 10 achieved a PSA50 response (76.9%, with one case pending confirmation), and 5 achieved a PSA90 response (38.5%). Among 9 subjects with RECIST-measurable lesions, the objective response rate (ORR) was 33.3% (3 partial responses), and the disease control rate (DCR) was 88.9%. One 70-year-old subject who had previously received four lines of therapy achieved a confirmed partial response (cPR) after completing six cycles of treatment at 50 kBq/kg, with a 97.7% reduction in PSA from baseline.

2Under Triple Industry Chain Barriers: Oligopolistic Landscape and Over 400 RLT Clinical Trials

Radiopharmaceuticals represent a typical high-barrier sector, with entry barriers primarily stemming from three aspects:

The first hurdle: radionuclide supply. Many medical radionuclides (such as Mo-99/Tc-99m, Lu-177, Ac-225, and I-131) require nuclear reactors or high-energy accelerators for production. Among them, the current global annual output of Ac-225 is extremely limited, representing a critical bottleneck constraining the commercial scale-up of alpha radionuclide therapies. Against the backdrop of global supply chain uncertainties, a proprietary commercial supply chain — from upstream manufacturing to downstream clinical application — must be strategically deployed as early as possible.

The second hurdle: radiopharmaceutical manufacturing qualifications. The production, storage, transportation, and use of radiopharmaceuticals require specialized licenses, facilities, and personnel qualifications, and are subject to stricter regulatory oversight compared to conventional pharmaceuticals.

The third hurdle: delivery timeliness. Many radionuclides have half-lives measured in hours — for example, the half-life of ⁶⁸Ga is approximately 68 minutes, ¹⁸F is about 110 minutes, and ¹⁷⁷Lu is roughly 6.6 days. This means the entire workflow, from drug manufacturing to patient administration, must be completed within hours to days, necessitating a nationwide radiopharmaceutical production and distribution network.

It is precisely the compounding of these three barriers that has resulted in a distinctly oligopolistic landscape in China's radiopharmaceutical market, with China Isotope & Radiation Corporation, Dongcheng Pharmaceutical, and Grand Pharmaceutical each holding leading positions. Among them, China Isotope & Radiation Corporation reported an operating revenue of RMB 7.187 billion in 2025, with its radiopharmaceutical business generating RMB 4.020 billion, contributing over 50% of total revenue and nearly 80% of gross profit. Dongcheng Pharmaceutical achieved an operating revenue of RMB 2.741 billion in 2025, of which the radiopharmaceutical segment recorded full-year revenue of RMB 1.136 billion, a year-on-year increase of 12.2%. Its revenue share rose to 41.4%, making it the company's largest source of revenue. Grand Pharmaceutical Group reported operating revenue of HK$12.28 billion in 2025, representing a year-on-year increase of 5.5%.

Reviewing the global radiopharmaceutical market landscape, the oligopolistic structure and the rise of early-stage assets are not only the current landscape of China's RLT and RDC tracks, but also the reality for innovative therapeutic radiopharmaceuticals globally — a rapid expansion phase ahead of the commercialization and licensing surge.

Globally, only Novartis's two therapeutic RLT drugs — [177Lu]Lutathera (targeting SSTR2) and [177Lu]Pluvicto (targeting PSMA) — are approved for marketing. In China, only Pluvicto is approved for marketing. As of July 2025, over 400 RLT/radiopharmaceutical-related clinical trial records were registered on platforms such as ClinicalTrials.gov (as reported in a 2025 review in Cancers, doi:10.3390/cancers17213412), with approximately 65% focusing on the two major targets, PSMA and SSTR. When evaluated based on "clinical-stage independent pipeline assets," approximately 60–80 RLT candidate molecules are currently in clinical development.

Since 2025, multiple innovative therapeutic radiopharmaceuticals in China have achieved key advances:

Serial No. | Developer/Originator | Product | Drug Type - Carrier | Target | Nuclide | # Indications | Clinical Stage | Highlights/Progress |

1 | CrystalCore Biologics | JH02 | RDC | PSMA | 177Lu | Metastatic Castration-Resistant Prostate Cancer (mCRPC) | Phase II | The first company in China to secure dual regulatory approval in China and the United States in the TRT field |

2 | Hengrui Pharmaceuticals | HRS-4357 | RDC | PSMA | 177Lu | mCRPC | Phase II | Validating Hengrui's Platform Capabilities in Radiopharmaceuticals |

3 | Yunnan Baiyao / Yunhe Pharma | INR102 | RDC | PSMA | 177Lu | mCRPC | Phase I/IIa | Benchmark Radiopharmaceutical for a Traditional Chinese Medicine Giant's Transition to Innovative Drugs |

4 | Dongcheng Pharmaceutical / Lannacheng | LNC1011 | RDC | PSMA | 225Ac | mCRPC | Phase I Clinical Trial | China's first domestically developed alpha-particle radiopharmaceutical to enter late-stage clinical trials; the first alpha-particle radiopharmaceutical pipeline to receive FDA IND approval |

5 | Hexin Pharmaceuticals | HX02 | RDC | Integrin αvβ3 + CD13 (Dual-Target) | 177Lu | Integrin αvβ3 and/or CD13 receptor-positive tumors (pancreatic cancer, gastric cancer, etc.) | Phase I Clinical Trial | The world's first dual-target radiopharmaceutical approved for clinical trials, overcoming the challenge of tumor heterogeneity; the dual-target design triples drug penetration efficiency. |

6 | Newray Medical | NRT6020 | RDC | FAP | 177Lu | `FAP-Positive Advanced Malignant Solid Tumors` | Phase I Clinical Trial | China's First FAP-Targeted Theranostic Drug to Enter Clinical Trials |

7 | Baili Tianheng | BL-ARC001 | ARC | Not Disclosed | 177Lu | Advanced or Metastatic Solid Tumors | Phase I Clinical Trial | China's First Class 1 Innovative Antibody-Radionuclide Conjugate (ARC) Drug to Enter Clinical Trials |

8 | Xiantong Pharmaceutical | 177Lu-XT117、XTR017 | PRC | FAP | 177Lu | FAP-Positive Advanced Solid Tumors | Phase I Clinical Trial | An Innovative Global First-in-Class FAP-Targeting Radiopharmaceutical Featuring a Novel Molecular Structure |

9 | Fulian Pharma | FL-020 | RDC | PSMA | 225Ac | mCRPC | Phase I Clinical Trial | Disclosure of a global first-in-class (FIC) target or novel chelation technology; 2024 FDA Fast Track designation; |

10 | Borui Chuanghe | 177Lu-BRP-010 | RDC | FAP | 177Lu | FAP-Positive Solid Tumors | IND Approved | World's first covalent targeted radiopharmaceutical (CTR) approved for clinical trials; utilizes SuFEx "latent warhead" technology to achieve irreversible covalent linkage of the ligand to the target protein. |

11 | Nuoyu Pharma | NY104 | RDC | CA9(CAIX) | 177Lu | Clear cell renal cell carcinoma (ccRCC) | IIT | China's First Theranostic Radiopharmaceutical for Kidney Cancer / World's First CA9-Targeting Small-Molecule Radiopharmaceutical for Renal Cancer |

Beyond catching up at the molecular level, New Radiomedicine Technology targets the upstream radionuclide supply chain bottleneck: the world's second and China's first commercial Cyclone IKON 30 MeV cyclotron, commissioned in January 2026, enables large-scale production of clinically scarce radionuclides such as Ge-68, I-123, Zr-89, and Ac-225 [8]. The key significance of this equipment lies in establishing domestic large-scale manufacturing capacity for Ac-225 against the backdrop of a global shortage of alpha-emitting radionuclides, marking a crucial step for China's radiopharmaceutical industry to catch up with the "alpha era" — a crucial link. Ultimately, competition in radiopharmaceuticals boils down to competition for radionuclide supply capacity — a reality that will be increasingly recognized following ASCO 2026.

3Anchored by ASCO 2026: Four Key Insights into the Development of China's Radiopharmaceutical Industry

On Chinese radiopharmaceuticals/RDCs industry, ASCO 2026 is both a "benchmark" and a "roadmap": Grand Pharmaceutical's theranostic closed-loop, Hengrui's pipeline of Class 1 innovative drugs, Sinotau's sprint in diagnostic radiopharmaceuticals, and New Radiomedicine Technology's radionuclide self-sufficiency are all catching up along this central trajectory.

Direction confirmed:

Novartis confirmed at ASCO 2026 — with earlier-line Pluvicto data and first-in-human results for 225Ac-PSMA — the "PSMA target + from β to α" primary development track. The strategic layout of Chinese enterprises (including Grand Pharmaceutical's TLX591, Hengrui's PSMA pipeline, and Sinotau's diagnostic radiopharmaceuticals) aligns closely with it — indicating that the track chosen by domestic companies is correct. In a field where R&D cycles routinely span several years and investments per drug candidate frequently exceed hundreds of millions, selecting the right direction itself constitutes immense value.

The gap is objective:

Meanwhile, we must objectively acknowledge that the pivotal data readouts for radiopharmaceuticals/RDCs at ASCO 2026 remain predominantly from multinational corporations, with products from Chinese radiopharmaceutical companies mostly at the stage where "diagnostic products lead the way, while therapeutic candidates are either in Phase III or have recently been approved for clinical trials," exhibiting a generational gap compared to the already marketed Pluvicto/Lutathera.

Opportunities upstream and in speed:

The barriers to radiopharmaceuticals lie not only in the molecules, but more critically in the radionuclide supply and the production and distribution network. This represents the most significant difference between radiopharmaceuticals and conventional innovative drugs — even if a traditional chemical drug boasts leading clinical data, it still requires support from manufacturing, sales, and medical insurance reimbursement channels; whereas the manufacturing, sales, and insurance value chains for radiopharmaceuticals are significantly more complex and are inextricably linked to the half-life of the radionuclides. From this perspective, the domestic production of radionuclides, represented by New Radiomedicine Technology's commercial cyclotron, precisely aligns with the next-generation direction highlighted at ASCO 2026 — a landscape of simultaneously advancing "upstream gap-filling and downstream frontier-pursuing."

Breakthroughs in novel targets:

Beyond PSMA, clinical advancements in emerging targets such as FAP, CAIX, and GRPR may give rise to the next generation of star RLT products.

The uniqueness of the radiopharmaceutical sector lies in the fact that, unlike chemical drugs or biologics, it cannot achieve rapid scaling through an "asset-light" model. Instead, it constitutes a tightly integrated industry chain that binds together molecular design, radionuclide production, radiopharmaceutical manufacturing, cold-chain logistics, and clinical application. This "asset-heavy, network-intensive, and supply-chain-reliant" characteristic establishes a deep competitive moat, but equally dictates that no market player can achieve overnight success.

ASCO 2026 has already set the main theme of the transition from β to α. What remains is for Chinese radiopharmaceutical companies to gradually bring this "accompaniment" to completion over the coming years through clinical advancement, radionuclide self-sufficiency, and network development.