From $35M out-license to $2.2B buyout: GSK acquires RAPT, with eye on Chinese-originated allergic drug

GSK

Pharmaceutical R&D Manufacturer

RAPT

Anti-cancer Biopharmaceuticals Manufacturer

On January 20, British pharmaceutical company GlaxoSmithKline (GSK) announced that it has entered into an agreement to acquire the US-based, clinical-stage biopharmaceutical company RAPT Therapeutics, Inc. (NASDAQ: RAPT) for approximately $2.2 billion (approximately £1.76 billion) in cash, at a price of $58.00 per share. This represents a premium of approximately 65% to RAPT's share price prior to the acquisition announcement, reflecting a market re-evaluation of RAPT's core asset.

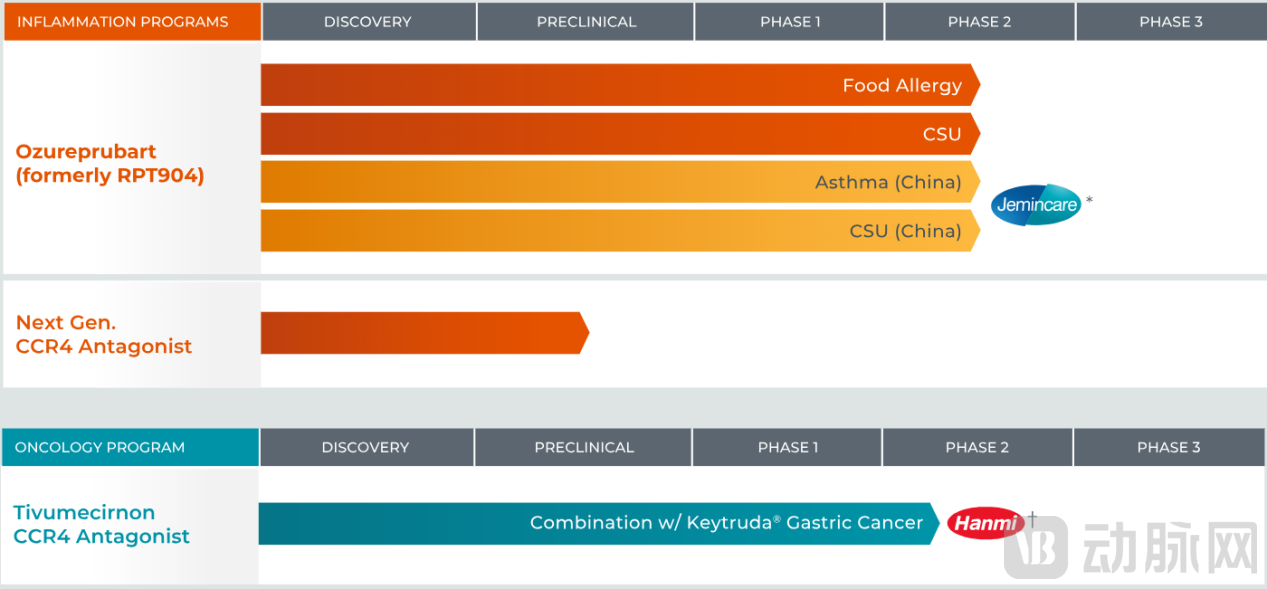

The centerpiece of this transaction is ozureprubart, a long-acting anti-immunoglobulin E (IgE) monoclonal antibody developed by RAPT. The development of this drug originated from the Chinese company Shanghai Jeyou Pharmaceutical.

In December 2024, RAPT licensed the global development and commercialization rights (excluding Chinese Mainland, Hong Kong, Macau, and Taiwan) to the anti-IgE antibody JYB1904 (internal code: RPT904). Under the licensing agreement, Shanghai Jeyou Pharmaceutical received an upfront payment of $35 million and is eligible to receive up to approximately $672.5 million in future success-based milestone payments, along with global sales royalties.

This drug candidate is being developed for the prevention of food allergy reactions and is currently in Phase IIb clinical development. Pursuant to the agreement, GSK will obtain the global rights (excluding Chinese Mainland, Hong Kong, Macau, and Taiwan) to develop and commercialize ozureprubart. Concurrently, GSK will assume the obligations for future milestone and royalty payments due to RAPT's partner, Shanghai Jeyou Pharmaceutical Co., Ltd.

For GSK, this acquisition represents not merely an investment in a single asset but also an adjustment to its long-term strategy. In recent years, GSK has been continuously building its presence in the respiratory, immunology, and inflammation sectors, driving growth through both internal R&D and strategic acquisitions to mitigate potential future patent cliffs. Ozureprubart's long-acting design, with dosing every 12 weeks, has the potential to reduce the treatment burden for patients compared to existing therapies. This holds significant value for the long-term management of chronic allergic conditions.

From a market demand perspective, the global incidence of food allergies is on the rise. According to GSK's epidemiological assessment data, in the United States alone, over 17 million people have been diagnosed with food allergies, of whom more than 65% are children and adolescents. This results in more than 3 million hospital or emergency care visits annually, with an associated economic burden of approximately $33 billion. For GSK, with its global commercial capabilities, the therapeutic area addressed by ozureprubart still presents a substantial unmet medical need, making this a strategically significant investment.

From Shanghai Lab to Global Stage: How RAPT Amplified a Chinese Asset's Value in 13 Months

RAPT Therapeutics is a clinical-stage biopharmaceutical company based in South San Francisco, California, USA, focused on developing treatments for inflammatory and immunologic diseases. RAPT Therapeutics modulates critical immune responses through antibody drug development to address allergic and autoimmune-related conditions. In the capital markets, RAPT's valuation is primarily driven by its core asset, ozureprubart, and its precursor molecules, which form the centerpiece of GSK's acquisition. Beyond ozureprubart, RAPT's pipeline includes products such as next-generation CCR4 antagonists, all targeting high-value inflammatory disease segments.

Overview of RAPT Therapeutics' Pipeline

Ozureprubart originated from the Chinese company Shanghai Jeyou Pharmaceutical. Since its establishment in 2018, Shanghai Jeyou has focused on innovative drug R&D, continuously expanding in antibody drugs and other novel molecular fields, with a strategic focus on a "3+1" matrix of therapeutic areas: oncology, kidney disease, pain, and autoimmune disorders. To date, Jeyou Pharmaceutical has over 40 research projects in its portfolio, including more than 30 small-molecule drugs and over 10 large-molecule drugs. These span nine Phase II clinical trials and ten Phase I clinical trials, with several core projects already achieving global distribution through external partnerships.

Overview of Jeyou Pharmaceutical's Key Core R&D Pipeline

The recent recurring phenomenon of Chinese-originated drug candidates being resold has fueled widespread perceptions that assets are being "sold too early," "undervalued," or that intermediaries are capturing disproportionate value. In reality, the reasons behind such valuation gaps are highly complex.

Two key factors drive this differential: Chinese biotechs' frequent lack of international operational capabilities, and the increased asset value that comes with advancing clinical development.

In the global development of this pipeline, RAPT has acted as a value amplifier. According to disclosures by RAPT Therapeutics, the company has established a globally oriented clinical development pathway for ozureprubart, initiating a Phase IIb clinical trial (pretigE) for food allergy and incorporating indications such as chronic spontaneous urticaria (CSU) into its future global development plan.

Simultaneously, RAPT has been advancing its Chemistry, Manufacturing, and Controls (CMC) system in accordance with the requirements of major regulatory agencies in Europe and the United States, while preparing for international regulatory pathways. These efforts have progressively aligned the candidate drug with global standards in data integrity, manufacturing consistency, and regulatory compliance. It is through this systematic progress in clinical and development activities that ozureprubart has evolved from an early-stage innovative asset originating in China into a candidate project with global development maturity, suitable for acquisition by a multinational pharmaceutical company. This progression forms a critical foundation for the current GSK transaction.

The $35M to $2.2B Leap: Decoding the New Model of Chinese Biotech Globalization

In recent years, Chinese innovative drugs have been undergoing value re-evaluation through a model of "out-licensing for global development + international repackaging." Taking this collaboration as an example, Shanghai Jeyou Pharmaceutical licensed the global development rights (excluding Greater China) to RAPT for $35 million upfront. RAPT then assumed responsibility for international clinical advancement, regulatory communications, and refining the manufacturing system, ultimately leading to its acquisition by GSK for approximately $2.2 billion. On the surface, such transactions can be easily interpreted as overseas intermediaries capturing a premium while Chinese-originated assets are transferred at a low price. However, viewed from a longer-term perspective, the value of China's innovative drugs is not locked in a one-time deal at the licensing stage. Instead, within the framework of international collaboration, their value is continuously amplified and repriced through clinical progress, compliance development, and the refinement of global development pathways.

The logic behind this model is clear: on one hand, Chinese companies have accumulated high-potential assets through differentiated innovation and early-stage R&D. On the other hand, international partners possess expertise in clinical advancement, regulatory strategy, and experience with European and U.S. regulatory bodies, enabling them to repackage these Chinese assets into mature ones that align with global standards and are ready for direct market entry or acquisition by major pharmaceutical companies. GSK's acquisition targets not just a "drug," but the de-risking, time savings, and global readiness that come with it. By acquiring a candidate drug approaching mid-to-late-stage clinical development, GSK swiftly supplements its pipeline and reduces R&D risk.

This phenomenon reveals several industry insights: First, China's domestic R&D capabilities in drug design, molecular optimization, and clinical strategy are approaching globally leading levels, capable of generating assets with global commercial potential. Second, out-licensing is no longer about "selling products at low prices" but about co-creating value: the Chinese R&D partner retains domestic rights and long-term benefits in China while sharing in the global development returns. This model accelerates the globalization of assets and provides Chinese innovative drug companies with a risk-controlled path to internationalization. Third, large international pharmaceutical companies, facing internal R&D pressures, patent cliffs, and growth demands, are willing to pay a premium for assets approaching mid-to-late-stage clinical development with differentiated advantages, thereby enabling rapid pipeline replenishment.

From an industry trend perspective, the global expansion of Chinese innovative drugs is no longer merely about "entering overseas markets" but represents a comprehensive integration spanning R&D capabilities, international clinical advancement, regulatory compliance, and asset pricing systems. This means Chinese innovative drug companies are not only exporting products but also participating in the division of innovation and value distribution within the global pharmaceutical value chain. As more candidate drugs meeting international standards enter global clinical trial systems through licensing and collaborations, this pathway of out-licensing for global development, followed by repackaging and high-premium acquisition, may become a significant paradigm for the global development of domestically developed innovative drugs.