Navigating WuXi AppTec's shadow: how CDMOs are carving a new path with peptides

WuXi AppTec

New Drug R&D and Production Service Provider

ASYMCHEM

Pharmaceutical R&D and Production Outsourcing Service Provider

Jiuzhou Pharma

Innovative Drug CDMO and Generic Drug Manufacturer

Sinopep

Developer, Manufacturer, and Distributor of Peptides and Small-Molecule Chemical Drugs

How to find a path to survival under the shadow of industry giants?

The CDMO industry currently exhibits a competitive landscape characterized by "market concentration at the top, breakthroughs in niche segments, and intensifying divergence." Platform giants like WuXi AppTec, with their strengths in capacity reserves, flow chemistry technology, global layout, and oligonucleotide synergies, occupy a dominant market share.

According to relevant statistics, of the 40 small molecule drugs approved by the U.S. FDA between 2024 and the first half of 2025, 8 were supported by WuXi AppTec's service platforms. This not only underscores the indispensable value of this leading CDMO—making it difficult to replace in the global market in the short term—but also highlights the immense challenges for mid-tier CDMOs attempting to compete directly with it.

Notably, a "high-growth cohort" is emerging by focusing on the peptide CDMO services and achieving growth rates that outpace the industry average. This group includes both technology-specialized firms like Asymchem and Jiuzhou Pharma, which maintain revenue scales around ¥3 billion RMB, and niche experts like Sinopep, ShengNuo Bio, and Medtide.

While industry leaders dominate the core market through their integrated platforms and scale, technical barriers in specialized fields create windows of opportunity for technologically adept players. The future competition in the CDMO sector is likely to evolve from a primary focus on cost advantages to a greater emphasis on technological depth. The rise of peptide CDMO services offers an early glimpse into this shifting industry dynamic.

Peptide-Driven Performance

The expansion of GLP-1 therapies is providing a significant boost to the peptide CDMO services industry.

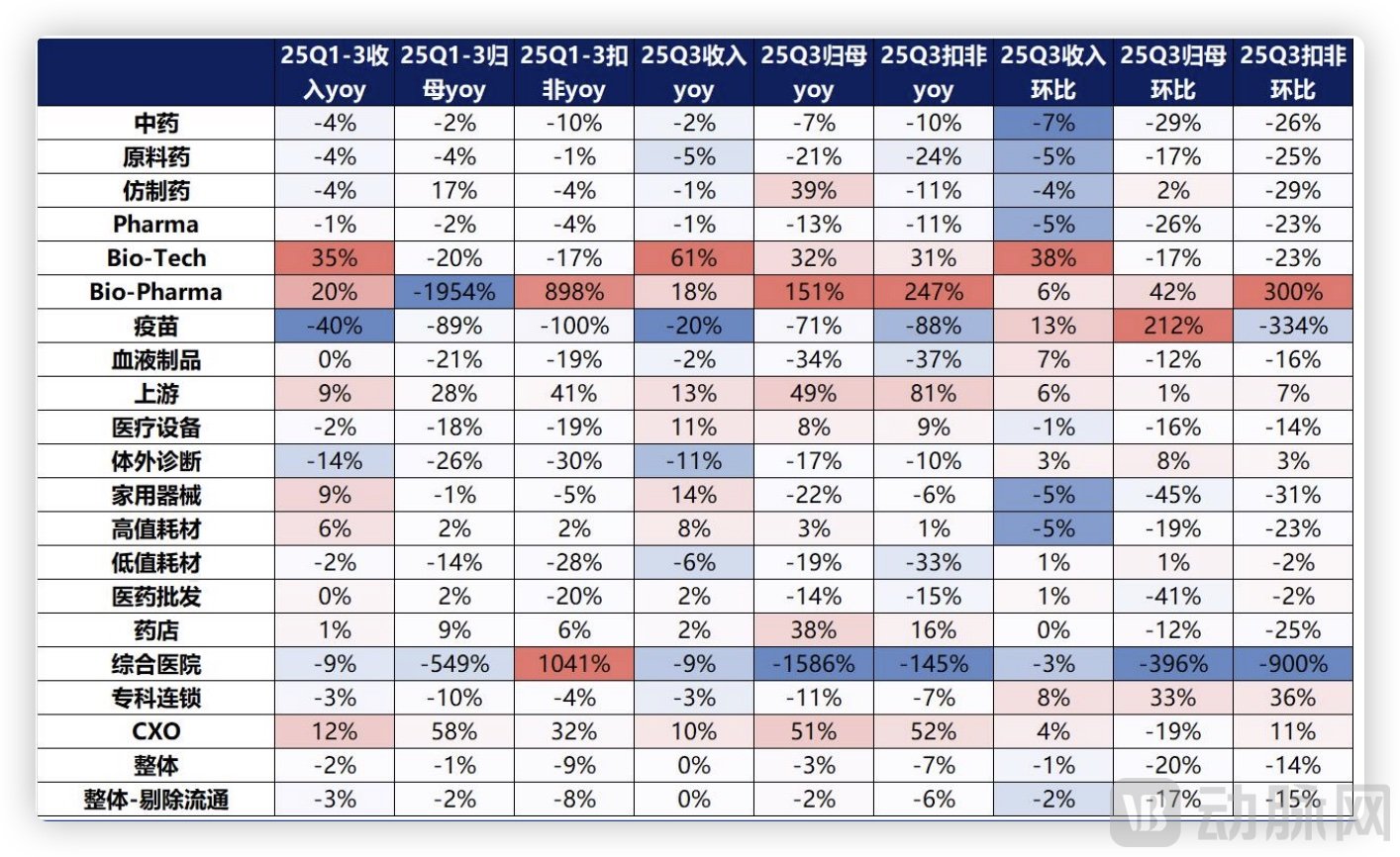

According to data from Huafu Securities, the CXO sector reported a 12% year-on-year revenue increase in the first three quarters of 2025, with net profit attributable to shareholders rising 58%. In Q3 2025 alone, revenue grew 10% year-on-year, with net profit up 51%. While industry leader WuXi AppTec demonstrated strong momentum with a 41% year-on-year increase in orders for the first three quarters, the broader industry recovery is better reflected in the upward trajectory of other CDMO players.

Performance of Pharmaceutical Sub-Sectors, Source: Huafu Securities

Notably, peptide-related business has become a primary growth driver for several CDMO companies.

Asymchem, for instance, achieved total revenue of RMB 4.63 billion in the first three quarters of 2025, an 11.82% year-on-year increase. While its small molecule CDMO services revenue remained largely flat, its emerging businesses – including peptides, oligonucleotides, and ADCs – saw a collective 72% revenue growth. Revenue from chemical macromolecules, led by peptides, surged over 150% year-on-year. With new business orders maintaining double-digit growth and a stronger order backlog for Q4 delivery, the company projects full-year revenue growth of 13%–15%.

ShengNuo Bio reported a 54% year-on-year increase in revenue for the first three quarters, with net profit attributable to shareholders surging 123%, primarily driven by the rapid growth of its peptide business. Similarly, Sinopep achieved revenue of RMB 1.527 billion, a 22% year-on-year increase, and a 27% rise in net profit, also fueled by its peptide segment. Medtide, another player focused on peptide services, also reported a substantial increase in its project portfolio during the reporting period.

This growth is undeniably linked to the global volume expansion of GLP-1 drugs. According to Q3 2025 financial reports, Novo Nordisk's core product, semaglutide, generated approximately $25.4 billion in sales across its three major brands in the first three quarters. Its competitor, Eli Lilly's tirzepatide, achieved sales of approximately $24.8 billion during the same period. Combined, these two giants account for a market exceeding $50 billion.

Inspired by this success, numerous pharmaceutical companies have recently entered the GLP-1 arena. Their participation has not only rapidly expanded the global peptide market but also accelerated the growth of the peptide CDMO services industry. The Chinese CDMO sector has adeptly capitalized on this wave. However, the dominant presence of a giant like WuXi AppTec often overshadows the achievements of other companies.

For these competitors, finding a viable development path amidst this competitive pressure is crucial for the healthy and balanced growth of the entire industry.

The era of scale-driven dividends is fading, giving way to the rise of peptide CDMO services fueled by technological premium.

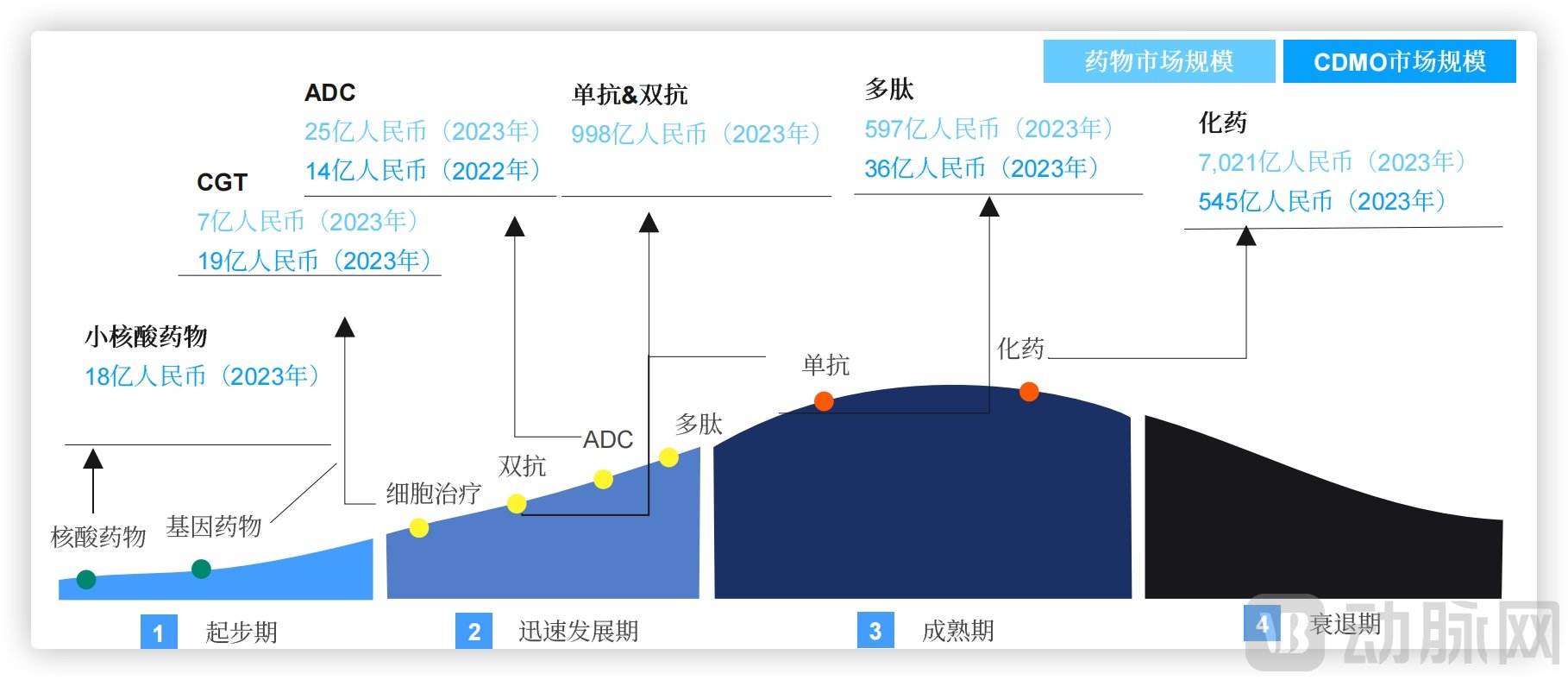

Historically, Chinese CDMOs competed globally primarily through massive capacity expansion to achieve economies of scale. However, in recent years, the rise of various novel therapies has led to a steady annual increase in the number of First-in-Class (FIC) drugs. These new therapies often face complex challenges in process development and scale-up production optimization, creating a shift in market demand. This shift is pushing the Chinese CDMO industry to transition from relying on scale advantages to creating technology-driven value.

Addressing these challenges requires more than just building additional manufacturing plants; it demands breakthroughs at the technological source. This evolution places higher demands on companies, emphasizing deep technical expertise over pure capacity.

Peptides represent a specialized segment within the CDMO industry that is reaching maturity precisely through this move towards greater specialization and technical sophistication.

Life Cycle of China's Biomedical Development, Source: Frost & Sullivan

In recent years, Asymchem has positioned chemical macromolecule CDMO—represented by peptides—as a key emerging business for development. Leveraging its established technological expertise, client relationships, and quality systems from the small molecule CDMO sector, the company is extending and horizontally expanding its capabilities into chemical macromolecules, including peptides.

Asymchem has successfully established multiple advanced synthesis pathways. These include ongoing refinement of traditional Solid-Phase Peptide Synthesis (SPPS), mastering Liquid-Phase Peptide Synthesis (LPPS) to enable efficient synthesis of complex sequences, achieving industrial-scale production of several bioactive peptides through precise regulation of expression and secretion via biofermentation, and developing chemo-enzymatic peptide synthesis routes.

Furthermore, the company applies its deep expertise in Continuous Flow Chemical Technology (CFCT) to peptide synthesis processes. This enhances yield, purity, and production safety. In anticipation of future industry trends, Asymchem is also advancing its capabilities in cyclic peptide synthesis technologies.

Building on its strong reputation and established partnerships with global pharmaceutical leaders in the small molecule CDMO sector, Asymchem has successfully extended these collaborations into emerging areas such as peptides. Currently, multinational pharmaceutical companies are the primary drivers of its peptide business growth. The company anticipates that from late 2025 into 2026, the international market will become the dominant source of its peptide service revenue.

As peptide projects advance to mid and late stages, demand for production capacity increases significantly. Following substantial prior expansion, Asymchem's capacity utilization rate is currently in a ramp-up phase. The company supports over a dozen molecules in the peptide-based weight loss field, with nearly half in Phase 2 and Phase 3 clinical trials. Several projects are expected to enter the process performance qualification (PPQ) stage next year, which will further drive capacity requirements. According to its interim report, the company's total solid-phase peptide synthesis capacity is projected to reach 44,000L by year-end 2025, with construction of a third dedicated peptide facility already underway.

While integrated CDMOs like Asymchem with comprehensive capabilities remain relatively rare, finding the right specialized vertical focus becomes increasingly crucial for other players seeking competitive differentiation in this evolving landscape.

ShengNuo Bio has built its strategy around an integrated API + Formulation model, covering the entire process from peptide Active Pharmaceutical Ingredient (API) R&D and manufacturing to formulation development. The company possesses extensive expertise in peptide synthesis and modification technologies, including long-chain peptide conjugation, large-scale production of mono-thio cyclic peptides (with synthesis purity reaching 95%, far exceeding industry averages), synthesis of multiple disulfide-bonded cyclic peptides, and PEGylation modification.

This technological foundation enables the company to integrate three key business segments across the peptide pharmaceutical value chain: peptide CDMO services, peptide APIs, and peptide formulations. Importantly, GLP-1 related business currently represents only about 30% of its operations, demonstrating that the company has not confined its peptide business solely to metabolic diseases. Among its pipeline of over 40 active projects are early-stage R&D programs from global Top 10 pharmaceutical companies, spanning therapeutic areas such as oncology and anti-infectives.

Such collaborations not only provide stable revenue streams but also enable the company to expand its expertise across the broad peptide landscape. The ability to support potential blockbuster drugs from early development stages can subsequently strengthen its API business through commercial-scale manufacturing. Additionally, ShengNuo Bio has extended its peptide technology platform into the cosmeceutical field, where its cosmetic peptide products - manufactured in compliance with EU EFfCI GMP standards - address various applications including anti-wrinking skin soothing, whitening, eye care, and hair loss prevention, with a portfolio of over 80 distinct products.

Sinopep has successfully overcome the technical bottlenecks in large-scale production of long-chain peptide drugs, establishing a solid-liquid hybrid peptide manufacturing platform. This platform enables multi-kilogram scale production of side-chain chemically modified peptides and long-chain modified peptides. The company has demonstrated capability to achieve single-batch production exceeding 10 kilograms for compounds including semaglutide and tirzepatide.

These technical breakthroughs have driven substantial capacity expansion. Following the operational launch of the peptide innovative drug CDMO Workshop 106 in late 2024, Workshops 107 and 108 commenced operations successively in the first half of 2025. Additionally, the annual production line for 395 kilograms of peptide APIs has been successfully put into operation. Through these manufacturing advancements, Sinopep now provides comprehensive customized services for both innovative and generic peptide drugs, covering the entire spectrum from process route design and process validation to quality studies, drug development, and commercial manufacturing. This end-to-end support spans the complete drug development cycle from discovery and preclinical research through clinical trials to market approval.

Medtide, specializing in peptide CDMO services, leverages its mature and efficient large-scale peptide API production technologies. The company excels in key areas including peptide drug design, modification, and synthesis, with substantial expertise in long-chain peptides and complex modified peptides. Medtide currently maintains an average success rate exceeding 99.95% in synthesizing novel molecules and possesses the capability to handle multiple 100-kilogram scale orders concurrently.

Medtide has further established two specialized technology platforms: PeptiConjuX for peptide-drug conjugates and PeptiNuclide LinkTech for radiopharmaceutical conjugates. The company has synthesized approximately 1,900 peptide precursor molecules, providing critical resources for innovative drug development. These capabilities facilitate the development of complex molecules, helping clients overcome key technical challenges such as product purification and impurity elimination, and have earned recognition from Gilead Sciences.

Jiuzhou Pharma, another CDMO player demonstrating strong growth with an order increase exceeding 20%, has added over 20 new clients for its peptide business this year, securing nearly $10 million in new contracts and successfully delivering more than ten projects. Clients are drawn to its comprehensive peptide synthesis technology platform, which encompasses solid-phase synthesis, liquid-phase synthesis, hybrid solid-liquid phase approaches, and an original non-classical solid-phase synthesis technology.

Notably, Jiuzhou Pharma has successfully synthesized protein fragments containing up to 78 amino acids—significantly longer than current popular GLP-1 drugs such as tirzepatide (39 amino acids) and semaglutide (31 amino acids)—demonstrating its technical capability to handle highly challenging projects.

In summary, companies have developed differentiated advantages in the peptide CDMO services business based on their unique technical strengths. Players like Asymchem leverage their scale and platform effects to rapidly achieve technology transfer and capacity expansion. Companies such as Sinopep and ShengNuo Bio have built their competitive edge by creating deep technical barriers within specific process segments. Meanwhile, Medtide's distinct advantage lies in its early-stage CRO services, which provide access to projects at the source, combined with its highly internationalized operational capabilities.

However, a key question remains: can the now maturing peptide business continue to deliver sustained revenue growth?

Peptides still hold potential, but the era of competing on core capabilities has arrived.

The current prosperity of the peptide CDMO sector is primarily driven by the commercial explosion of GLP-1 drugs (e.g., semaglutide, tirzepatide) for weight loss, a potential already strongly validated by financial performance. While the commercial promise of GLP-1s is being realized, the future growth of peptide drugs is expected to be sustained by diversified drivers, mainly from technological iteration and indication expansion.

The first driver is innovation in peptide technology platforms. This includes the strong emergence of multi-target peptide drugs, exemplified by:

Eli Lilly's Retatrutide (targeting GLP-1, GIP, and GCGR), currently in Phase 3 trials and showing 30-50% greater weight loss efficacy than single-target agents.

Innovent Biologics' Mazdutide, the world's first approved dual GLP-1/GCGR agonist.

Roche's investment in Amylin-based peptides, which aim for both weight loss and muscle preservation.

Amgen's MariTide, a long-acting dual-target agent combining a GLP-1 receptor agonist with a GIP receptor antagonist.

As standard peptide production capacity becomes increasingly commoditized, the next phase of competition will shift toward more technologically demanding areas. These include long-chain peptides, complex modified peptides (such as cyclic peptides with stable ring structures and high target affinity), and advanced strategies like peptide-drug conjugates (PDCs) and peptide-oligonucleotide conjugates (POCs). Crucially, AI-assisted drug design is poised to play an increasingly important role in the discovery and development of PDCs and cyclic peptide therapeutics.

In terms of indication expansion, peptide therapies are demonstrating diversified potential. Beyond the pursuit of MASH approval by GLP-1 drugs, progress is being made in oncology. For instance, PDS Biotechnology's peptide vaccine PDS0101, combined with Keytruda (pembrolizumab), achieved a median Overall Survival (OS) of 39.3 months in a Phase 2 trial for HPV16-positive recurrent/metastatic head and neck squamous cell carcinoma. Similarly, Elicio Therapeutics' ELI-002, a peptide vaccine targeting mutated KRAS, demonstrated a 77% reduction in risk of death and an 88% reduction in risk of recurrence in Phase 1/2 studies involving patients with pancreatic and colorectal cancers.

Furthermore, the application of peptide therapies continues to expand across diverse therapeutic areas. Johnson & Johnson and Protagonist Therapeutics have submitted an NDA to the FDA for their oral peptide therapy icotrokinra, intended for the treatment of psoriasis. Separately, Merck's oral macrocyclic peptide, enlicitide decanoate, demonstrated a significant reduction in LDL-C levels in patients with hypercholesterolemia in a Phase 3 trial. In the rare disease field, Apellis Pharmaceuticals' bicyclic peptide therapy Empaveli and Stealth Biotherapeutics' peptide therapy Forzinity have both received FDA approval.

In summary, peptide-based drugs have emerged as a major R&D direction for treating a wide range of diseases, offering novel treatment options across multiple therapeutic areas. Compared to traditional small molecule drugs, peptide therapeutics are inherently more complex, placing higher demands on multiple stages of the production process. This growing complexity, in turn, elevates the requirements for CDMO partners, necessitating deeper technical expertise and more advanced capabilities.

While current competition still revolves around production capacity and delivery capabilities for popular targets like GLP-1, the demand structure is undergoing a significant shift. In markets such as Europe, the U.S., and Japan, the core patent protection for semaglutide is not set to expire until 2031, leading many CDMO companies to continue stockpiling capacity. However, if companies neglect technological advancement and fail to adapt to industry evolution during this period, they risk severe impact when challenges such as overcapacity, lagging R&D capabilities, and market demand fluctuations inevitably arise.

As the market transitions from shortage to surplus, and competition shifts from capturing new demand to battling for existing market share, the core competencies required for success will fundamentally change.

Peptides represent not just the "present" but also a key "future" for the CDMO industry. However, the source of value creation will inevitably shift from pure production scale toward technological innovation and ecosystem development. Only by focusing on complex process technologies, engaging with projects at early stages, and expanding into new therapeutic indications can companies position themselves to capture sustained value from the next wave of peptide drug development.