From explosive growth to brutal price war: how to navigate the future of China's CBCT market

Meyer

Developer of Core Technologies and Products for Intelligent Recognition

Largev

Medical Imaging Product R&D, Manufacturing, and Service Provider

In recent years, China's Cone Beam Computed Tomography (CBCT) machine market has experienced explosive growth. With the rapid increase in domestic production rates, more cost-competitive products have entered the market, driving rapid penetration. CBCT machines have now become standard equipment in many small and medium-sized private dental institutions.

However, after a phase of intense expansion, an industry crisis centered on price wars has emerged: CBCT manufacturers face operational challenges, downstream dental clinics experience disruptions to daily diagnostics, and upstream core component suppliers are exposed to bad debt risks. This chain reaction makes it imperative for the entire industry chain to seek breakthroughs.

Currently, there are 85 valid CBCT product registrations in China, with domestic products comprising 60% of the total.

When CBCT technology was first introduced to China's dental sector, imported equipment dominated the high-priced market. Purchasing was primarily feasible for well-funded dental hospitals and large general hospital dental departments. Private clinics with limited budgets mainly relied on traditional imaging equipment like dental X-ray units.

The rise of domestic CBCT products in China has gradually broken the price monopoly once held by international brands. Locally manufactured equipment not only offers significant cost advantages but also provides localized after-sales services supported by regional production bases. Consequently, a growing number of private dental clinics are adopting China-made CBCT machines to replace their traditional imaging equipment. Simultaneously, more small and medium-sized institutions now have the capacity to equip themselves with CBCT technology.

Furthermore, China's dental care market continues to expand, with the number of private dental clinics showing an overall upward trend. Particularly following the implementation of policies such as centralized procurement for dental implants, private institutions have emerged as key players, driving increased rigid demand for imaging devices like CBCT.

Overall, in recent years, private dental clinics have become the primary purchasers of domestically produced CBCT devices in China. Additionally, dental hospitals and general hospitals are increasingly recognizing the value of China-made devices, with the proportion opting for domestic solutions rising annually. Together, these trends are accelerating the development of China's CBCT market.

The period from 2021 to 2023 marked the peak for domestic CBCT approvals in China. As an increasing number of new products entered commercial production at scale, market competition intensified significantly over the past two years. With the growing number of market participants, price competition has become the primary strategy for companies to capture market share. Industry data shows that from 2019 to the first half of 2024, the average unit price of CBCT in China dropped substantially from 1.02 million RMB to 572,300 RMB, a decline of over 43%. Annual price reductions for some products even exceeded 20%.

The impact of this price competition has been unavoidable, even for leading companies in the sector.

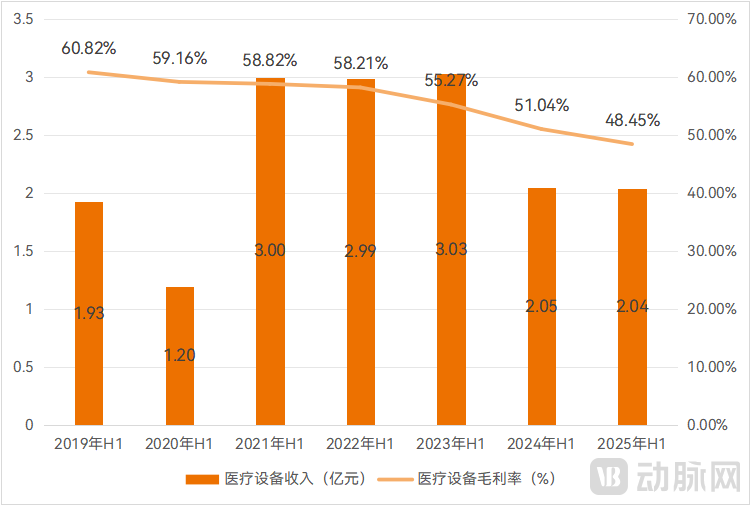

Meyer Optoelectronic, a publicly listed company in the CBCT industry, derives the majority of its medical device segment revenue from CBCT operations. In recent years, this segment has shown noticeable performance volatility: From the first half of 2019 to the first half of 2025, the segment's gross margin consistently declined from 60.82% to 48.45%. In the first half of 2024, revenue from the medical device segment contracted sharply by 32.27%. Despite this, Meyer Optoelectronic has maintained a consistent product development cycle, launching a new product approximately every two years, indicating continued commitment to R&D. The company has repeatedly cited increasingly fierce industry competition and broader macroeconomic challenges as the core reasons for its performance pressure in financial reports.

Revenue and Gross Margin Changes in the Medical Device Segment of Meiya Optoelectronic.

Data Source: Company Financial Reports

LargeV Instrument, in its IPO prospectus, also disclosed a downward trend in its product pricing. The average unit price of its core product line, the Smart3D series, decreased from RMB 224,200 in 2019 to RMB 204,500 in 2021, while the HiRes3D series dropped from RMB 337,700 to RMB 327,600. Market competition was cited as a contributing factor to these price adjustments.

While established market leaders are compelled to adjust prices under competitive pressure, emerging small and medium-sized CBCT companies are adopting even more aggressive strategies. To rapidly capture market share—particularly by penetrating lower-tier markets—some have reduced product prices to approximately RMB 100,000 per unit. More radical sales tactics have also emerged, such as offering "zero-down-payment installment plans" and "buy-one-get-one-free" promotions (where purchasing a CBCT system includes complimentary smaller dental devices or consumables).

In the short term, increased product variety and more affordable pricing have indeed accelerated CBCT market penetration. This has enabled many small and medium-sized private dental clinics to adopt CT-based imaging for accurate diagnosis.

Over time, however, a series of adverse ripple effects have become increasingly evident, suggesting that there may be no real winners in this price war. From dental institutions and equipment manufacturers to upstream supply chain partners, all are caught in a vortex of competition, each bearing the consequences of persistent price erosion.

The most immediate impact has been the erosion of profit margins for equipment manufacturers. This, in turn, raises concerns about potential disruptions in product supply or after-sales service, ultimately threatening their operational sustainability and long-term viability in the market.

For established industry leaders, their substantial financial reserves provide a buffer—they can withstand temporary declines in revenue and gross margin. However, for startups still reliant on primary market financing, the damage from price competition is particularly acute. For example, in 2025, one CBCT manufacturer faced a series of challenges including factory shutdowns, disruption of after-sales services, and lawsuits from suppliers. Although the company has since announced a gradual resumption of production and service operations, its brand reputation has been significantly damaged.

Meanwhile, as a technology-intensive product, CBCT requires continuous R&D investment to enhance imaging precision, optimize software algorithms, and expand application scenarios. Yet under price war pressures, companies are compelled to divert resources toward marketing rather than technological advancement. In the long run, this will weaken the overall competitiveness of China's CBCT industry, hindering its ability to compete effectively with international brands.

On the service front, while healthcare institutions can purchase CBCT at increasingly lower prices, hidden costs may emerge.

Amid intense price competition, some manufacturers sustain operations by cutting R&D budgets, lowering component standards, and reducing after-sales service costs. As a result, certain low-cost CBCT systems exhibit significant functional limitations.

VCBeat has learned from dental institutions that issues with low-cost CBCT primarily include: poor image quality that directly impacts diagnosis and treatment planning; system slowdowns or instability after extended use; delayed technical support responses for critical failures; and premature failure of core components shortly after the warranty period expires, requiring costly replacements. When equipment becomes unusable during emergencies, clinics must refer patients to other facilities, leading to customer loss. If serious problems persist unresolved, clinics are forced to allocate additional budget to replace the equipment.

Consequently, these dental institution managers consider that the low purchase price of CBCT does not equate to high cost-effectiveness.

The upstream supply chain also struggles to remain insulated from this vicious cycle of price competition.

In recent years, China has made breakthrough progress in localizing core CBCT components. In X-ray generators, both medical high-voltage power supplies and X-ray tubes have achieved complete domestic production, breaking international technological monopolies and establishing independent R&D capabilities. For detectors, two major core product categories—dynamic amorphous silicon flat panels and dynamic CMOS flat panels—have entered domestic mass production, with technical specifications now matching those of imported products.

The localization of core components in China has yielded two significant outcomes: a substantial reduction in CBCT production costs, granting China-made devices distinct price competitiveness; and the facilitation of collaborative R&D between equipment manufacturers and component suppliers, accelerating the implementation of new technologies and applications. This has enabled China-made CBCT to achieve leapfrog improvements in critical performance metrics such as imaging precision and scanning speed—a development that initially represented a positive and promising trajectory.

However, the escalating price war is now impacting upstream supply chains. In June 2025, core component manufacturer CareRay Digital Medical filed a lawsuit against CBCT manufacturer DentaFilm for outstanding payments. Recently, CareRay announced a first-instance court ruling awarding nearly RMB 16 million in overdue payments and default penalties. However, with DentaFilm currently operating under abnormal status, CareRay disclosed it has made provisions for bad debt against this receivable. The ultimate financial impact remains uncertain pending final enforcement of the ruling.

Should core component manufacturers face sustained operational pressures, they may be forced to reduce R&D investment, potentially slowing technological iteration. This decline in component quality and innovation would subsequently constrain the performance improvements of CBCT systems, creating a vicious cycle that ultimately undermines the healthy development of the entire industry chain.

The prolonged price war in China's CBCT market has prompted industry participants to recognize the unsustainability of competing solely on price, driving collective efforts to reshape this detrimental landscape.

In early 2025, DentaFilm issued two CBCT product price adjustment announcements, with the first round applying across its entire product portfolio. The company explicitly stated that the price increases aimed to "better deliver high-quality products and services to customers while fostering sustainable market and corporate development."

Beyond establishing rational pricing structures, breaking the current impasse requires CBCT companies to build value through products and services. Recent market dynamics indicate that the industry should focus on three strategic pillars: demand adaptation, technological innovation, and application expansion.

For instance, developing competitively differentiated equipment aligned with the "cost-performance" demands of private institutions.

When procuring equipment, private clinics prioritize cost-effectiveness and often expect these systems to serve as tools for patient acquisition and practice growth. This clearly defines a direction for CBCT product differentiation.

Currently, several companies including LargeV Instrument, Meyer Optoelectronic, and Boen Zhongding Medical have introduced multi-functional CBCT machines. Beyond standard dental CT, panoramic imaging, and cephalometric projections, these devices also integrate intraoral X-ray capabilities. Although priced higher than basic CBCT models, they eliminate the need for separate shielding rooms for dental X-ray units, thereby reducing initial setup costs and ongoing facility expenses for clinics.

Additionally, companies like Boen Zhongding and Yofo Medical have launched mobile CBCT units mounted in vehicles. These systems can operate without lead-lined rooms, enabling deployment in various scenarios such as community health programs, medical check-ups, and mobile dental services. This flexibility effectively addresses the dynamic operational needs of small and medium-sized dental institutions.

Furthermore, CBCT technology demonstrates significant potential for cross-specialty application expansion, creating new growth opportunities.

CBCT's advantages in imaging dense tissues—including superior image quality, lower radiation dose, and cost-effectiveness—make it suitable for extension beyond dentistry into specialties like ENT (Ear, Nose, and Throat). LargeV Instrument's ENT-specific CBCT machine has already received market approval in China through the Innovative Medical Device Special Review Process. This system addresses the limitation of conventional spiral CT in providing sufficient resolution for ENT-specific examinations.

Meanwhile, the potential applications of CBCT in precision radiotherapy and orthopedics are being actively explored. Further technical refinements are expected to unlock additional clinical scenarios.

Naturally, regardless of functional iterations, the core competitiveness of CBCT must remain centered on image quality, acquisition efficiency, and radiation control. Advancements in imaging precision, artifact reduction, low-dose scanning technologies, along with optimization of reconstruction and image processing algorithms, continue to be critical for building sustainable technological advantages.

Given that after-sales support has become a frequently cited concern among dental institutions, manufacturers can also differentiate themselves by providing responsive and efficient services—including consultation, installation, maintenance, and training.

Furthermore, leveraging AI technology to enhance clinical services represents another competitive dimension. For instance, integrated AI-powered oral health reporting features enable clinics to quickly generate intuitive patient reports, improving both diagnostic communication and the overall patient experience.

Indeed, multiple segments within China's healthcare industry have recently undergone phases of increasing localization rates and intensifying market competition, often accompanied by varying degrees of price erosion.

The experience of the CBCT sector serves as a clear reminder that competing primarily through price—at the expense of product quality, service delivery, and corporate profitability—is an unsustainable strategy. As the industry dynamic shifts from oversupply to a scarcity of high-quality solutions, more companies are recognizing the critical importance of quality. Moving forward, only by focusing on clinical needs, building differentiated value through technological innovation, application expansion, and service enhancement, and establishing a virtuous cycle of high-quality products and scalable revenue can companies—and the industry as a whole—achieve sustainable, long-term growth.