Why US dollar funds are betting big again on China biotech

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Braveheart Bio

Precision Therapy Developer for Cardiovascular Diseases

In September 2025, Hengrui Medicine completed another NewCo deal, signing an exclusive licensing agreement with U.S.-based Braveheart Bio for its self-developed small-molecule inhibitor of cardiac myosin, HRS-1893. The agreement includes an upfront payment of $65 million and a total potential transaction value of up to $1.013 billion. Notably, this marks Hengrui's fourth such licensing deal of the year, with the cumulative value of these four transactions now exceeding $15 billion.

This is undoubtedly an impressive figure. However, in an era of frequent high-value deals in the pharmaceutical industry, it is the investors behind them that are drawing greater attention. Reports indicate that, aside from the deal with Germany's Merck, the other three of Hengrui's out-licensing transactions this year were backed by U.S. dollar-denominated funds. This trend underscores an increasingly noticeable shift in the industry: US dollar funds are making a concerted push back into China's innovative drug sector.

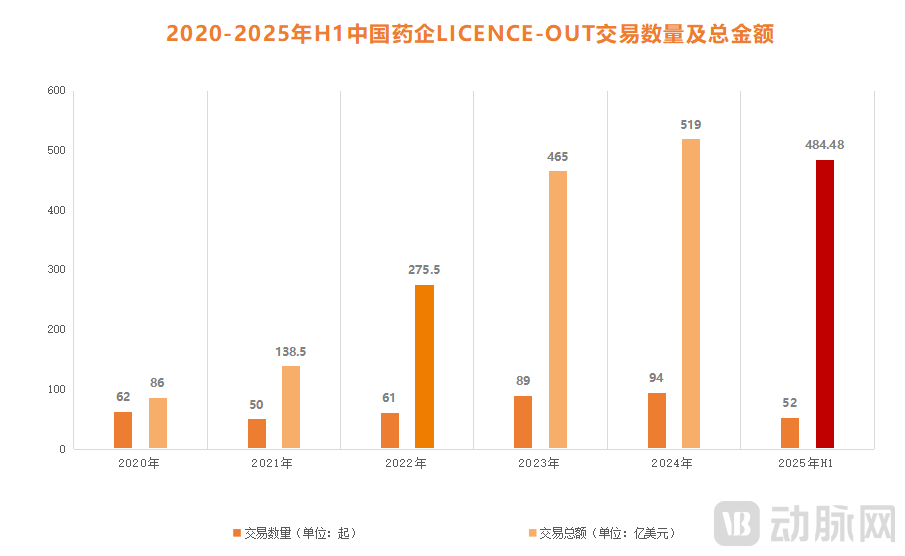

Figure 1. Number and Total Value of China's Pharma Out-Licensing Deals (2020 - H1 2025). Data Source: PharmaCube

This trend is well-founded. As early as the JPM Healthcare Conference in January this year, numerous US dollar funds expressed their intention to increase investment in China's innovative drug market. The reality has borne this out. Taking the most direct indicator—business development deals—as an example, according to incomplete statistics from VCBeat, the total value of China's out-licensing deals in H1 2025 reached $48.448 billion. This figure is approaching the total for the entire year of 2024 ($51.9 billion), with US dollar funds participating in over 80% of these transactions.

Furthermore, US dollar funds have shown a strong presence in cornerstone investments. Since the Hong Kong Exchanges officially launched the "Technology Enterprise Pathway" in May 2025, the Hong Kong stock market has experienced a long-awaited surge. To date, 18 healthcare companies have successfully listed, with their stock prices largely showing substantial upward trends. Throughout this rapid growth, cornerstone investors have been a key driving force. A report by Goldman Sachs indicates that cornerstone investors accounted for 42% of the total funds raised in HKEX IPOs this year. Among these, overseas investors contributed a significant two-thirds, predominantly comprised of US dollar funds.

This clearly indicates that after the large-scale retreat of recent years, US dollar funds have now aggressively returned with even greater momentum. So, what is the strategy behind this renewed push, and what changes will it bring to China's innovative drug market?

Why Are US Dollar Funds Focusing on China's Innovative Drugs Again?

Around 2010, a wave of US dollar funds, including Hillhouse Capital, Lilly Asia Ventures, and Fidelity Asia Ventures, began making early-stage investments in innovative drug companies such as BeiGene, Innovent Biologics, Junshi Biosciences, and Ascentage Pharma. This period is widely regarded as the starting point for dollar funds scaling up their investments in domestic innovative drug companies.

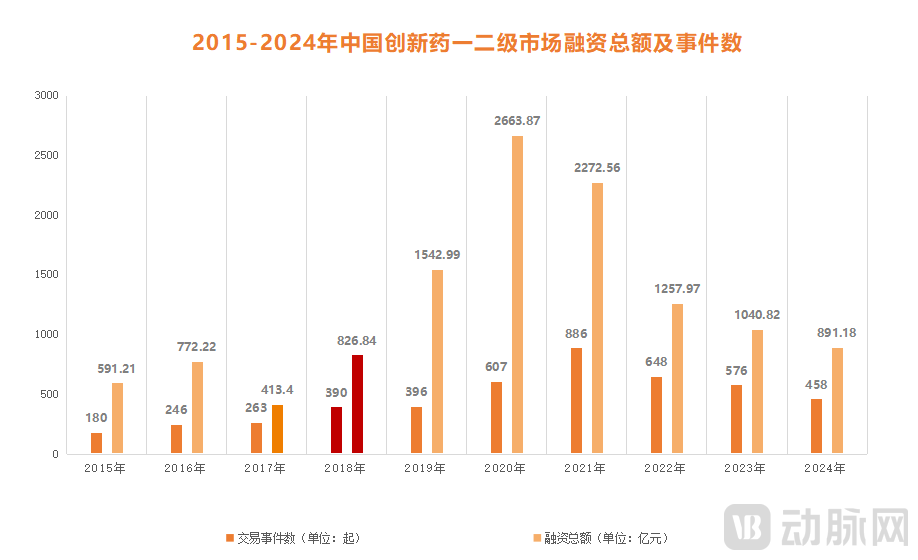

Figure 2. Total Financing Amount and Number of Deals in China's Innovative Drug Primary and Secondary Markets (2015-2024). Data Source: PharmaCube

Figure 2. Total Financing Amount and Number of Deals in China's Innovative Drug Primary and Secondary Markets (2015-2024). Data Source: PharmaCube

By 2018, with the official launch of the HKEX's Chapter 18A, investments from dollar funds into China's innovative drug sector entered a phase of explosive growth. According to data from PharmaCube's InvestGo database, the total financing in China's innovative drug sector across primary and secondary markets reached RMB 82.684 billion in 2018—a figure significantly higher than the previous three years combined. During this period, dollar funds contributed over 60% of the capital, emerging as the core driver behind the surge in financing for innovative drugs.

However, prosperity inevitably wanes. Beginning in 2022, as innovative drug stocks frequently broke their IPO prices and the high-valuation bubble burst, the once-booming biotech sector rapidly cooled, ushering in a capital winter. Data indicates that the total financing in China's innovative drug primary and secondary markets plummeted to RMB 125.797 billion in 2022—just half of the 2021 peak. During this period, the proportion of capital from dollar funds fell below 25%, with over half allocated to follow-on financing rounds rather than new projects. Consequently, a "great retreat" accelerated among dollar funds, manifested through either reduced investments or the outright dissolution of their China teams.

This downturn, however, proved short-lived. Starting in early 2024, US dollar funds made a vigorous comeback. What, then, are the underlying drivers behind this accelerated return?

The explanation lies in three key dimensions. First, it originates from the dollar funds themselves and their core investors. Taking multinational pharmaceutical giants—which demonstrate the strongest demand for Chinese innovative drugs—as an example, under immense pressure from the "patent cliff," increasing investment in China's innovative drug sector represents the optimal strategy to fill pipeline gaps and sustain revenue growth.

According to Bloomberg estimates, between 2024 and 2030, approximately $360 billion in annual sales from major pharmaceutical companies in the U.S. and Europe will face competition from generics due to patent expirations. This will inevitably create a significant revenue gap that internal R&D cannot fill in the short term. However, by engaging in licensing deals or acquiring Chinese innovative drug assets, particularly late-stage assets and mature pipelines, these companies can offset the impact on their growth timelines. A managing partner at a dollar fund commented on this strategy: "When R&D risks are too high and internal output is limited, external acquisitions have clearly become a necessary means for multinational pharmaceutical giants to sustain innovation vitality and capital returns."

Of course, such transactions have prerequisites. A key reason behind the dollar funds' current aggressive bets is the significant improvement in the overall quality of China's innovative drugs.

Figure 3. China's 14 Globally First-in-Class Bispecific ADC Drugs

Figure 3. China's 14 Globally First-in-Class Bispecific ADC Drugs

According to an exclusive analysis by Bloomberg in July 2025, the number of China's innovative drugs in development surpassed 1,250 in 2024, closely approaching the U.S. figure of approximately 1,440. Moreover, in terms of pipeline innovation, Chinese pharmaceutical companies are leading the way globally with innovative therapy models represented by "bispecific ADC." Currently, 14 first-in-class bispecific ADC drugs from China have entered clinical stages, with four advancing to Phase II or III trials—including Baili Pharmaceutical's BL-B01D1 and Alphamab Oncology's JSKN003.

Beyond overall quality improvements, the gradual return of China's innovative drug sector to reasonable valuation levels has also made the current investments by US dollar funds more cost-effective and strategically certain.

The final key factor lies in fundamental shifts in the global capital markets. From a pure business perspective, during the golden decade of venture capital in China's biotech sector, China stood out as the most profitable market for international investors outside the United States, bar none. Now, with its vast market scale for innovative drugs and a stable political and economic environment, China remains the optimal choice for dollar funds seeking high investment returns.

The landscape, however, has shifted. While US dollar funds once dominated the scene, capital from Europe, the Middle East, and East Asia is now pouring into Chinese innovative drug assets at an unprecedented scale. Take Japan for example: Takeda alone has deployed $15 billion through licensing deals into Chinese innovative assets over the past three years.

This surge of global capital has created unprecedented competitive pressure for dollar funds, compelling them to adopt more aggressive strategies to secure high-quality Chinese biopharma assets ahead of rivals worldwide.

Overall, the return of dollar funds represents a case of "strategic mutual need". On one hand, Chinese biotech companies at critical development stages require the capital infusion from these funds to overcome immediate financial constraints and support overseas expansion. On the other hand, amid a rapidly evolving global competitive landscape, dollar funds urgently need to identify new growth drivers—and the steadily improving Chinese innovative drug sector perfectly aligns with their pursuit of high-return, high-potential assets.

From "Global Layout" to "Certainty First"

When discussing the shifts in this wave of returning US dollar funds, many industry insiders have pointed to a consistent observation: the overarching strategy of these funds is evolving—from chasing globalization opportunities to pursuing more guaranteed outcomes.

How should this be understood? Through case analysis and synthesis of expert opinions, VCBeat has detailed this shift across three key dimensions, the first of which is the change in investment targets: US dollar funds are now focusing more on pipelines and products rather than the companies themselves.

Specifically, in their early involvement with China's innovative drug sector, dollar funds primarily engaged through direct equity investments, tying their capital to a company's overall development prospects and enterprise value. Now, however, their participation has shifted significantly toward licensing deals. Accordingly, their focus has moved toward specific pipelines and products—reflecting a preference for targeting concrete, high-potential drug candidates or individual assets rather than making broad bets on any single company as a whole.

This change, of course, has its reasons. In the past, dollar funds favored direct investment based on the pursuit of a "high growth, high return" macro narrative for China's innovative drug industry, believing that pharmaceutical companies would eventually go public, leading to an overall surge in equity value. However, now, the uncertainty of this model has increased, and the level of involvement has become more significant. Focusing on a single pipeline and product, on the other hand, can confine "certainty" and "risk control" within quantifiable transaction terms.

This shift is driven by clear rationale. Previously, dollar funds favored direct investments based on the macro narrative of "high growth, high returns" in China's innovative drug sector, betting on biotech companies eventually going public to drive substantial equity value appreciation. However, this model now faces greater uncertainty and requires heavier capital commitment. In contrast, focusing on specific pipelines or products allows funds to contain both certainty and risk control within quantifiable transaction terms.

The second dimension of change lies in the investment strategy: US dollar funds are transitioning from a "casting-a-wide-net" approach to "targeted fishing" in China's innovative drug market.

As is widely known, in their early involvement, dollar funds leveraged their global perspective and capital strength to adopt a "wide-net" approach in China's innovative drug sector. They targeted multiple promising fields and rapidly invested in numerous startups within each, hoping to identify dark horses. While this model did yield notable successes, its drawbacks became increasingly apparent: excessive concentration in specific segments meant that a downturn in one could lead to widespread losses; moreover, the highly variable quality of projects complicated subsequent exits. These issues have become particularly pronounced in the current complex environment.

In response, dollar funds have adapted. As Andrea Li, a partner at LongRiver Capital focused on innovative drug investments, stated in a recent interview, "Since 2022-2023, our requirement for almost every investment is that it must have a clear 'global expansion' positioning. To be acquired by multinational pharmaceutical companies or compete globally, a product must offer global innovation." Another fund manager expressed a similar view, noting that their selection criteria for innovative drug targets are now strictly twofold: "First, does the team have a proven track record of successfully out-licensing assets? Second, is their execution capability strong? Everything else is secondary." This reflects how dollar funds are now operating with heightened purpose, and how their core investment logic is increasingly aligned with "certainty first."

The third dimension of change lies in the form of involvement: US dollar funds are gradually shifting from purely financial investments toward an ecosystem-building approach characterized by hands-on involvement and long-term strategic partnerships.

Take the increasingly common NewCo model as an example. This model creates a deeper binding between US dollar funds and Chinese biotech innovators—transforming the relationship from a simple investment into a collaboration where both parties co-manage pipeline and product development, drive subsequent commercialization, share risks, and distribute returns more equitably. Data shows that in the first quarter of 2025 alone, Chinese innovative drug companies completed 13 NewCo deals, with a cumulative value exceeding $10 billion.

A senior investor focused on NewCo transactions commented: "The popularity of the NewCo model stems from two key factors. First, most dollar funds maintain close communication with multinational pharma giants and have a clear understanding of the targets, indications, and technology pathways these companies need. Second, in today's increasingly complex market environment, funds have realized that only by truly aligning capital, technology, and commercialization on the same platform can they both dilute early-stage high risks and amplify later-stage high returns. Clearly, the NewCo model offers a more rational and pragmatic pathway for such collaboration."

Beyond the NewCo model, the deep involvement of US dollar funds in China's biopharma ecosystem is also reflected in their earlier entry into the R&D process. This includes extensive research collaborations with Chinese academic institutions and direct investment in the translation of early-stage laboratory discoveries. Additionally, these funds have established or significantly expanded their on-the-ground investment teams in China. The goal is to stay closer to the local market and build an end-to-end ecosystem that spans research, translation, and industrialization—enabling them to identify and incubate breakthrough innovative drug projects at the earliest stages.

Looking back, it is clear that US dollar funds are no longer passive financial spectators, but have become co-creators deeply embedded in China's innovative drug landscape. This shift in role reflects a more profound understanding of the Chinese market and signals that China's biopharma sector itself has entered a more rational and mature phase of development.

Do the Benefits Outweigh the Drawbacks?

During the era of US dollar funds making direct investments in China's biotech sector, we witnessed the rise of companies like BeiGene, Innovent Biologics, and Junshi Biosciences. These firms have now become pillars of China's biopharmaceutical industry, embarking on a second growth curve driven by differentiated innovation and global expansion.

Today, however, US dollar funds have diversified their approach—shifting from direct investment to a mix of licensing deals, acquisitions, cornerstone investments, and increased positions in secondary markets. What, then, will this new wave of capital bring to China's innovative drug sector?

On one hand, it provides crucial financial support. According to incomplete statistics from VCBeat, from January 2024 to June 2025, the upfront payments from out-licensing deals secured by Chinese innovative drug companies exceeded $10 billion. Amid a capital winter, challenging IPO conditions, and intense commercial competition, this capital serves as a vital lifeline—not only enabling more biotech firms to survive but also fueling further pipeline development and commercialization.

Indeed, many innovative drug companies have already reaped significant benefits from this trend. For example, DualityBio, founded just six years ago, has generated over $6 billion through out-licensing deals, which helped fuel its successful listing on the Hong Kong Stock Exchange this year. Its stock price surged by 113%, setting a record for the highest first-day gain among Chapter 18A companies. Another notable example is Baili Pharmaceutical. Through a landmark out-licensing deal in 2024, the company not only turned a profit but also saw its net income soar by 575% to RMB 3.708 billion.

On the other hand, this trend is enabling more Chinese innovative drugs to "ride on others' ships to go global." Amid the reshaping of the global pharmaceutical market and intensifying pressure from domestic volume-based procurement and internal competition, the need for Chinese innovative drugs to expand overseas has never been greater. However, companies commonly face challenges such as limited international experience, lack of overseas registration and clinical resources, weak commercial channels, and cultural and compliance risks. Deep collaboration with US dollar funds has become an effective way to resolve these hurdles.

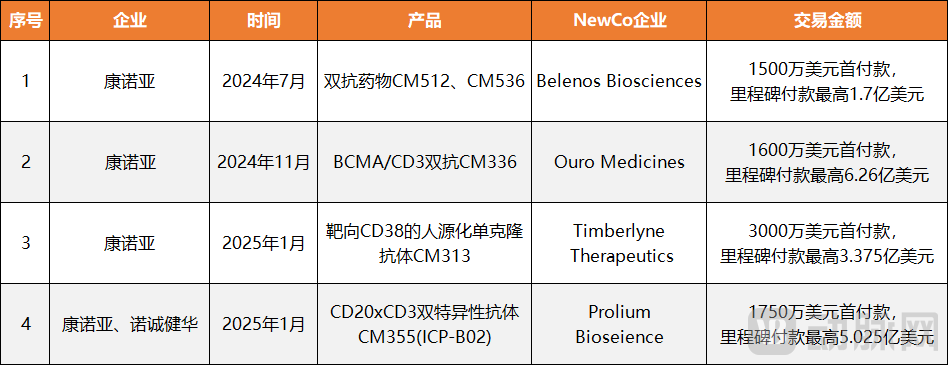

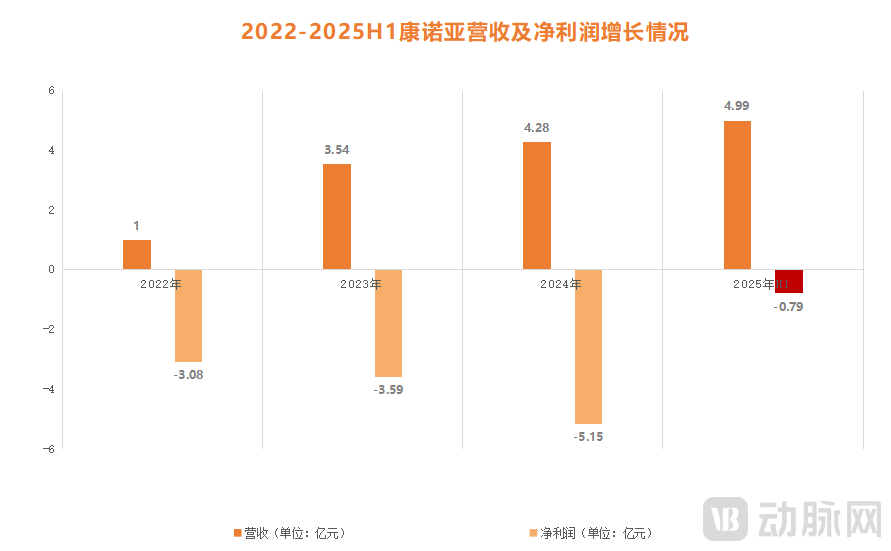

Figure 4. Keymed Biosciences' 4 NewCo Deals and the Company's Revenue & Net Profit Status

Take Keymed Biosciences as an example. In less than half a year, the company rapidly completed four NewCo deals, securing over $100 million in upfront payments. This significantly helped cover its net profit shortfall. Furthermore, through these NewCo transactions, Keymed successfully advanced five early-stage clinical assets into the global market, while also acquiring equity stakes in the newly established overseas companies—thereby expanding its international footprint and capital operation flexibility. According to its 2025 interim report, Keymed's net loss narrowed to $79 million, a year-on-year improvement of 76.59%, indicating a strong possibility of achieving profitability by year-end.

However, every coin has two sides. As licensing, NewCo, and M&A activities intensify, concerns are growing that the aggressive bets by US dollar funds might be leading to the "undervalued sale" of promising Chinese biotech assets—or even causing a significant drain of high-quality innovative drug resources from China.

These concerns are not unfounded. On one hand, some innovative drug companies, eager to secure deals, have indeed sold their assets at relatively low prices. On the other hand, there have been cases where US dollar funds, due to strategic shifts, misjudgment, or market changes, have left acquired Chinese drug assets shelved for extended periods, eventually turning them into "dormant assets."

Therefore, for Chinese biotech firms seeking to maximize returns in collaborations with US dollar funds, several principles are crucial. First, they must focus on pioneering innovation and continuously enhance the value of their pipelines and products. Second, they need to learn how to better align with US dollar funds to achieve a synergistic effect where 1+1 > 2. Finally, it is essential to secure greater decision-making power, establish clear boundaries of rights and responsibilities, and develop flexible exit mechanisms—ensuring a sustainable balance between leveraging capital support and maintaining autonomous development.

The founder of a well-known dual-currency fund shared with VCBeat: "In the first half of the year, US dollar funds were essentially in a trial phase—overall, the approach was quite cautious. But now, with tariffs largely stabilized and the market landscape relatively clear, their commitment to the Chinese market will grow even stronger."

Therefore, for more Chinese innovative drug companies, this undoubtedly represents another critical strategic window of opportunity. Those who can seize this momentum may gain a decisive edge in the increasingly competitive market.