The ophthalmology M&A spree: where are giants betting big?

Alcon

Ophthalmic Pharmaceuticals and Medical Devices Manufacturer

EssilorLuxottica

Eyewear Products Sales, Manufacturer

Carl Zeiss

Manufacturer of Optical Systems, Industrial Measurement, and Medical Devices

The ophthalmology sector has been abuzz with activity lately.

Since Alcon's announcement in August of a 51% premium acquisition of STAAR Surgical, related reports have dominated industry headlines. Simultaneously, two optical giants—Zeiss and EssilorLuxottica—along with prominent investment firms KKR and Jana Partners, have unveiled major acquisition deals. Within just two months, the global ophthalmology market witnessed five mergers and acquisitions, including several blockbuster transactions.

In reality, despite broader market headwinds, the ophthalmology industry has maintained notable dynamism and activity in recent years. Thus, this year's surge in M&A can be viewed as a continuation of earlier industry consolidation waves. Yet, within this new wave, has a fresh narrative emerged in global ophthalmology M&A? What distinct characteristics and development trends are taking shape?

To find answers, VCBeat has compiled and analyzed global ophthalmology M&A transactions announced to date in 2025.

Up to 10.7 Billion! Ophthalmology Giants in China and Abroad on a Buying Spree

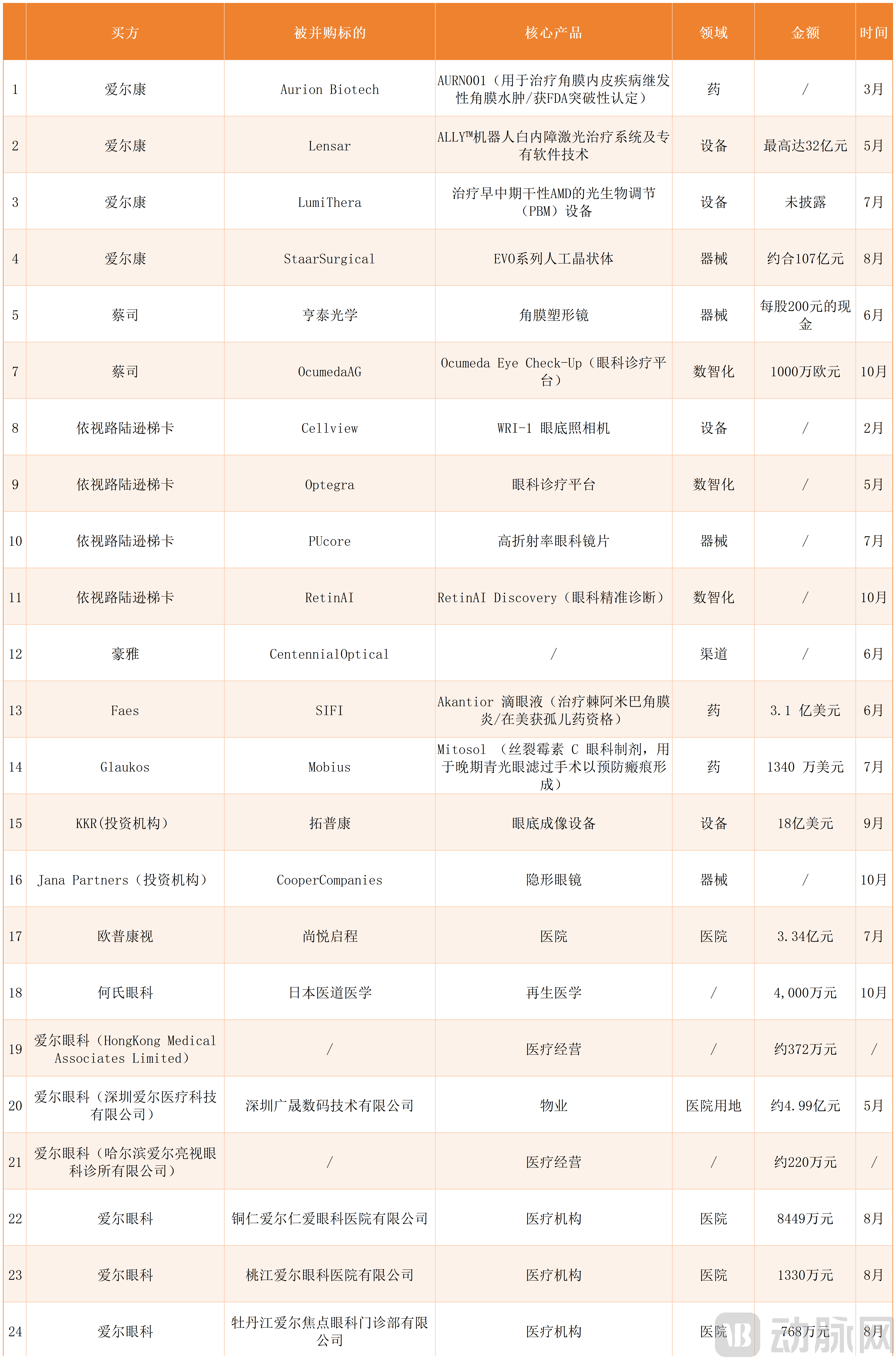

According to VCBeat's incomplete statistics, as of October 21, a total of 24 ophthalmology M&A transactions have occurred globally, with 15 disclosing deal values. Among these, if Alcon's acquisition of STAAR Surgical proceeds successfully, it is poised to set the year's record for the largest ophthalmology transaction—reaching approximately CNY 10.7 billion.

From the buyer's perspective, Chinese companies participated in 8 of these M&A deals (including 3 healthcare institution acquisitions, 1 medical land acquisition, and 2 healthcare business acquisitions by Aier Eye Hospital Group). The remaining 16 transactions were initiated by international ophthalmology giants or investment firms.

Regarding the significant disparity in M&A volume between China and the global market, industry analysts view this as both expected and reflective of current realities.

Several factors contribute to this gap. Firstly, China's ophthalmic services market is nearing saturation, compounded by a temporary consumer spending slowdown, which has led to declining revenue and profitability for service providers. In this context, listed Chinese ophthalmic service providers are showing greater interest in acquiring targets in international markets.

Secondly, China's ophthalmic pharmaceutical and device sectors are still in the early stages of domestic substitution, lacking the global presence and platform capabilities necessary for international M&A. Currently, these segments primarily attract venture capital funding rather than facilitating large-scale mergers and acquisitions. In contrast, international ophthalmic pharma and device companies operate at a significantly larger scale, making them more viable and valuable acquisition targets.

However, it is crucial to emphasize that although the number of Chinese ophthalmology M&A deals has been limited so far in 2025, their individual transaction values have been substantial.

China's orthokeratology lens leader, Ovctek, invested heavily by acquiring a 75% stake in Suqian Shangyue Qicheng Hospital Management Co., Ltd. for CNY 334 million, continuing its strategic expansion into ophthalmic service providers. While He Eye Specialist Hospital's acquisition of Japan's IDO MEDICAL required only CNY 40 million, this amount represented nearly the entirety of He's net profit for the first half of 2025.

Whether through major capital commitments or allocating virtually all available earnings, these moves demonstrate Chinese ophthalmic companies' strong confidence in the growth potential of both domestic and global markets. If Chinese firms express their market optimism with relative restraint, international ophthalmology giants display theirs unequivocally: Alcon executed four acquisitions, including this year's highest-value transaction; Zeiss acquired Brighten Optix at a 25.4% premium with a cash offer of CNY 200 per share; and EssilorLuxottica completed two deals within two months.

Beyond corporate acquisitions, two significant transactions led by investment institutions occurred this year: KKR's announced acquisition of Topcon in September, and Jana Partners' acquisition of Cooper Companies in October. The KKR-Topcon deal alone reached a value of USD 1.8 billion.

The diversity of acquirers, the frequency of transactions, and the substantial deal values collectively attest to the current vibrancy and significant future growth potential of the global ophthalmology market. This raises a pivotal question: what new narrative about the industry's evolution are global giants scripting through this latest wave of consolidation?

Betting on Refractive Correction

In 2025, "bolstering" product portfolios remains the core narrative behind M&A activities among ophthalmology giants.

Alcon continues to enhance its comprehensive ophthalmology portfolio through the acquisitions of Lensar, LumiThera, and STAAR Surgical; Zeiss's acquisition of Brighten Optix is aimed at strengthening its competitiveness in the ophthalmic consumer healthcare segment; while EssilorLuxottica's purchase of PUcore is driven by the intent to further solidify its moat in the lens sector.

Taking the two largest M&A deals by transaction value in the first and second half of this year as examples, we can further analyze the product expansion strategies of these global ophthalmology leaders.

Coincidentally, both of these major acquisitions were made by Alcon. As a global leader in eye care, Alcon has built a comprehensive product ecosystem spanning surgical procedures and vision care. Its portfolio ranges from ophthalmic diagnostic and surgical equipment—including Centurion phacoemulsification systems, Constellation vitreoretinal platforms, microscopes and laser devices—to innovative intraocular lenses for cataract and refractive correction, along with various contact lenses, lens care solutions and dry eye treatments. This integrated system already covers pharmaceuticals, consumables and ophthalmic diagnostic equipment, addressing the full spectrum of ocular diseases including cataracts, glaucoma, corneal conditions and retinal disorders.

Cataract treatment has consistently been Alcon's core strength. In addition to its competitive portfolio of intraocular lenses, the company's LenSx® laser-assisted cataract surgery system remains a cornerstone product in this therapeutic area.

In recent years, femtosecond laser-assisted cataract surgery (FLACS) has been emerging as the mainstream choice and prevailing trend for premium cataract procedures, owing to its significant advantages over traditional cataract surgery in precision, safety, and postoperative visual quality. Consequently, it has become a strategic focus for leading ophthalmology companies.

Among these platforms, Alcon's LenSx® system offers advantages in total ocular docking duration, ease of contact, femtosecond laser performance, and energy precision. Since its introduction into the Chinese market in 2013, the LenSx® system has been upgraded to its third generation, with installed units in mainland China reaching 200.

However, in the FLACS market, Alcon faces a direct challenge from its formidable competitor Johnson & Johnson. Following the resolution of their patent dispute—which concluded with Alcon paying nearly USD 200 million in compensation—the company urgently needs technological upgrades. The answer to this need appears to be Lensar's ALLY Robotic Cataract Laser Treatment System.

Reports indicate that acquiring the Lensar ALLY system would provide Alcon with at least three key advantages in the FLACS segment:

The first is the enhancement of core therapeutic performance. Specifically, the system's integrated dual-modal laser technology enables simultaneous tissue cutting and real-time imaging, operating at speeds up to four times faster than conventional equipment. Furthermore, combined with iris registration technology, it automatically calculates corneal incision angles, achieving an error rate below 0.5 degrees and a remarkable 95% accuracy in postoperative visual acuity prediction. Finally, the system is particularly suitable for patients with narrow palpebral fissures—common in Asian populations—and when paired with the newly launched oval-shaped patient interface in China, improves surgical comfort by 60%.

The second is the advancement in automation. The ALLY Robotic Cataract Laser Treatment System is the world's first surgical robotic platform capable of performing the entire FLACS procedure within a single sterile environment. It integrates steps that previously required multiple devices—including incision, capsulorhexis, and lens fragmentation—onto a unified platform, thereby reducing procedure time by 30%. Industry analysts suggest that enhancing FLACS automation was a primary driver behind Alcon's acquisition of Lensar.

The third is accelerated penetration into target markets. The system's "AI Mentor" mode shortens the training cycle for novice surgeons from six months to just three, while increasing procedural standardization by 50%. It also reduces the risk of secondary surgery for complex cases, such as traumatic cataracts, from 3% to 0.8%. Combined with its particular suitability for treating patients with narrow palpebral fissures—a common anatomical feature in Asian populations—the system holds significant potential for adoption in grassroots healthcare markets, especially in China.

As for Alcon's acquisition of STAAR Surgical, the move aims to strengthen its competitive edge in the refractive correction market.

Although Alcon has established a relatively comprehensive refractive product portfolio, it has not yet offered phakic intraocular lenses (pIOLs). Phakic IOL implantation is currently one of the primary refractive surgery techniques. Unlike corneal refractive procedures such as LASIK and SMILE—which use lasers to reshape the cornea and permanently alter its refractive power—phakic IOL implantation involves no corneal cutting. Instead, a removable artificial lens is implanted between the iris and the natural lens, preserving corneal integrity and avoiding irreversible side effects.

This has prompted numerous companies worldwide to actively enter this segment. Among them, STAAR Surgical's Evo ICL stands out as the most competitive offering.

The reasons are multifaceted. First, its core material, Collamer™, is highly distinctive. Composed of 60% poly-HEMA, 36% water, 3.8% benzophenone, and 0.2% porcine collagen, it makes the lens lighter and more hydrophilic while facilitating better exchange of gases and nutrients. More notably, although the related patent expired as early as 2014, no company globally has yet been able to replicate its proprietary manufacturing process or produce a material with comparable performance.

Secondly, the Evo ICL series continues to innovate and iterate, forming a comprehensive product portfolio. For instance, in 2020, the innovative presbyopia-correcting EVO Viva™—indicated for correcting or reducing presbyopia and myopia in phakic and aphakic eyes—received market approval. In 2022, both the EVO/EVO+ ICL for myopia correction and its toric version for astigmatism received FDA approval in the United States.

Finally, the commercial value of the Evo ICL series has been validated by the market. Taking China—a key focus market—as an example, STAAR Surgical's financial reports indicate annual growth rates of 50%, 38%, and 25% for the years 2021 to 2023, respectively. It should be noted that although revenue in the Chinese market began to decline sharply from Q4 2024, many industry analysts view this as a temporary effect of macroeconomic softness and weakened consumer confidence, with a high likelihood of recovery ahead. Alcon's premium-priced acquisition offer and the subsequent public opposition from STAAR Surgical's shareholders following the announcement serve as strong testaments to the industry's confidence in both the growth potential of China's refractive correction market and STAAR Surgical's future performance.

Furthermore, it should be emphasized that while Alcon's acquisition of STAAR Surgical was also motivated by the latter's well-established market channels and commercial presence in China—built over years of dedicated operation—this in no way diminishes the fact that the Evo ICL series itself possesses substantial market competitiveness.

Based on Digital Intelligence, Achieve Deep Integration of the Entire Ophthalmology Industry Chain

The continued emphasis on ophthalmic digital-intelligent diagnostics and treatment, aimed at achieving integrated hardware-software-service solutions across the entire industry chain, represents another underlying driver of M&A in the ophthalmology sector in 2025.

To date in 2025, global ophthalmic giants have initiated three digital-intelligence-related acquisitions: EssilorLuxottica's acquisitions of Optegra and RetinAI, and Zeiss's acquisition of Ocumeda AG. A common characteristic across these deals is the strategic "identity shift" of the acquirers.

Let's first examine EssilorLuxottica's two acquisitions. Although also a renowned brand in the global eye health landscape, EssilorLuxottica differs from Zeiss, Alcon, and Johnson & Johnson in that its historical strength lay in the more consumer-oriented eyeglass lens segment. However, since 2019, this optics-focused company has embarked on a strategic expansion into serious ophthalmic medicine, executing over ten acquisitions within six years.

Among these, the July 2024 acquisition of an 80% stake in Heidelberg Engineering provided capabilities in optical coherence tomography, real-time image processing analysis, and digital surgical navigation. The December 2024 acquisition of Espansione supplemented its expertise in diagnosing and treating dry eye, ocular surface diseases, and retinal disorders. In February 2025, the purchase of Canadian startup Cellview further enhanced its capabilities in ultra-widefield retinal diagnostics.

More recently, EssilorLuxottica announced the acquisition of RetinAI to further strengthen its capabilities in ophthalmic digital precision diagnostics. Specifically, RetinAI's flagship platform, RetinAI Discovery, leverages AI technology to rapidly process and analyze large-scale retinal image data, effectively assisting healthcare professionals in more accurately diagnosing and monitoring blinding eye diseases such as age-related macular degeneration, glaucoma, and diabetic retinopathy.

However, as EssilorLuxottica deepens its presence in serious ophthalmic medicine—particularly in precision diagnostics—through these acquisitions, a pressing question emerges: how can it secure clinical adoption channels for these diagnostic products and other ophthalmic offerings to rapidly penetrate the serious ophthalmic medicine market?

Moreover, if this "channel" could simultaneously provide clinical expertise, efficient patient communication capabilities, and the ability to accumulate and capture patient insights, it would not only enable EssilorLuxottica to enter the market swiftly and precisely but also furnish valuable data insights and real-world testing scenarios for future product development.

Optegra emerges as the platform that aligns perfectly with these requirements. Public information indicates that Optegra operates in five key European markets—the UK, Czech Republic, Poland, Slovakia, and the Netherlands—managing over 70 ophthalmic hospitals and diagnostic centers. This infrastructure provides essential clinical deployment channels for EssilorLuxottica's eye care products. Furthermore, Optegra's network of experienced ophthalmologists offers crucial clinical capabilities, while its direct patient access creates a vital channel for gathering patient needs and feedback.

According to numerous industry observers, the acquisition of Optegra marks EssilorLuxottica's formal, large-scale entry into serious ophthalmic medicine, signaling its transformation from a publicly recognized eyewear company into a global medical technology leader redefining future eye health.

Zeiss is undergoing a similar "identity shift." In the Chinese market during 2024, Zeiss launched a myopia management platform and partnered with Shanghai Health Cloud to initiate a hospital management remote connectivity project. These initiatives aim to channel high-quality medical resources to broader populations through innovative digital telemedicine models, delivering efficient, high-quality, and accessible ophthalmic care.

More recently, Zeiss Vision Care announced it has entered into a definitive agreement to acquire a 10% stake in Ocumeda for €10 million, with an option to increase its holding to 25% in the future.

Similar to EssilorLuxottica's rationale for choosing Optegra, Zeiss selected Ocumeda for its ability to facilitate pan-European scalable expansion and integrate service pathways connecting patients, optometrists, opticians, and ophthalmologists.

Specifically, Ocumeda is a leader in European tele-ophthalmology, having built an extensive and diversified network for ophthalmic screening and care. This network comprises over 300,000 active patients, 700 optical retail stores, professional ophthalmologists, and insurance providers such as CSS Health Insurance. By incorporating platform screening services into insurance coverage and implementing digital tiered diagnosis and treatment systems, Ocumeda continuously expands its reach within target user groups—laying the market foundation for Zeiss's product expansion.

Furthermore, Ocumeda's imaging data and remote diagnostics capabilities can achieve deep interoperability and organic synergy with Zeiss's professional equipment. This exemplifies how digitalization is dissolving traditional industry boundaries in eye care, driving the integrated convergence of "hardware, data, and services."

Amid this wave of converging industry boundaries, Chinese companies are also actively participating. For instance, several major listed Chinese ophthalmic service providers have deeply invested in AI-ophthalmology integration.

Aier Eye Hospital Group has achieved notable results in building its telemedicine center, now covering over 20 provinces across China with more than 400 specialist consultants. In the first half of 2025 alone, it completed over 200,000 remote image readings.

He Eye Specialist Hospital uses smart ophthalmic devices as entry points, combining AI-assisted diagnosis with online expert consultations to achieve "early monitoring, early warning, early intervention, and early treatment" for ocular and chronic diseases.

Chaoju Eye Care has successfully launched an AI physician assistant and an AI knowledge base based on multiple large language models including DeepSeek, ushering in the era of multimodal AI ophthalmic applications.

In other words, within certain ophthalmic segments, Chinese innovation is steadily rising. We firmly believe that as more domestic innovators emerge, China is poised to develop large-scale ophthalmic device enterprises. When that day comes, the Chinese ophthalmic M&A landscape will undoubtedly witness remarkable vibrancy.