GenFleet’s record-breaking HKEX Chapter 18A listing: how did they achieve it?

GenFleet Therapeutics

Innovative Drug Developer

On September 19, GenFleet Therapeutics (2595.HK), a commercial-stage biotechnology company focusing on cutting-edge therapies in oncology and immunology, was listed on the main board of the Hong Kong Stock Exchange. The gross proceeds prior to the exercise of the over-allotment option reached USD 233 million, and will increase to USD 268 million after the exercise of the over-allotment option, making it the largest IPO fundraising under Chapter 18 rule on the Hong Kong Stock Exchange (HKEX) since 2022.

Cornerstone investors have committed a total of USD 100 million in subscriptions, setting a new record for HKEX Chapter 18A biotech listings since 2022. The nine cornerstone investors include RTW Funds, OrbiMed, TruMed, UBS Asset Management (Singapore) Ltd., Vivo Funds, CUAM Entities, Fullgoal Entities, Tibet Longrising, Lake Bleu Entities. Over half of these investors are specialized healthcare investors, including top-tier international medical funds with extensive long-term investment track records. This robust investor composition aligns with the relatively large offering size and floating share structure, which will enhance post-listing liquidity, stabilize share price performance, and provide sustained support for the company’s future R&D and operations.

GenFleet was the first biotech to enter the HKEX under Chapter 18A with a commercially launched product (fulzerasib) as well as established licensing revenue at the stage of IPO. Fulzerasib was approved in August 2024 as China's first and the world's third marketed KRAS G12C inhibitor. Since 2021, GenFleet has secured multiple licensing partnerships with leading pharmaceutical and listed companies globally, including Innovent Biologics, SELLAS and Verastem Oncology.

Founded in August 2017 by Dr. Qiang Lu and Dr. Jiong Lan, GenFleet Therapeutics focuses on developing innovative therapies for oncology and immunological diseases. The company has raised RMB 1.421 billion through seven private financing rounds, achieving a pre-IPO Series C+ post-money valuation of RMB 3.124 billion.

As the originator of China's first KRAS G12C inhibitor with a diversified pipeline of both large and small molecules and extensive business development experience, GenFleet exemplifies the typical growth trajectory of a Chinese biotech company.

1From "China's First" to "World's First"

Zooming in on the product pipeline, GenFleet's RAS therapy matrix started from tackling "undruggable targets"—taking the hard path first—then building a diverse product series around the RAS pathway, gradually evolving into one of the world's most comprehensive developers of RAS-targeted therapies.

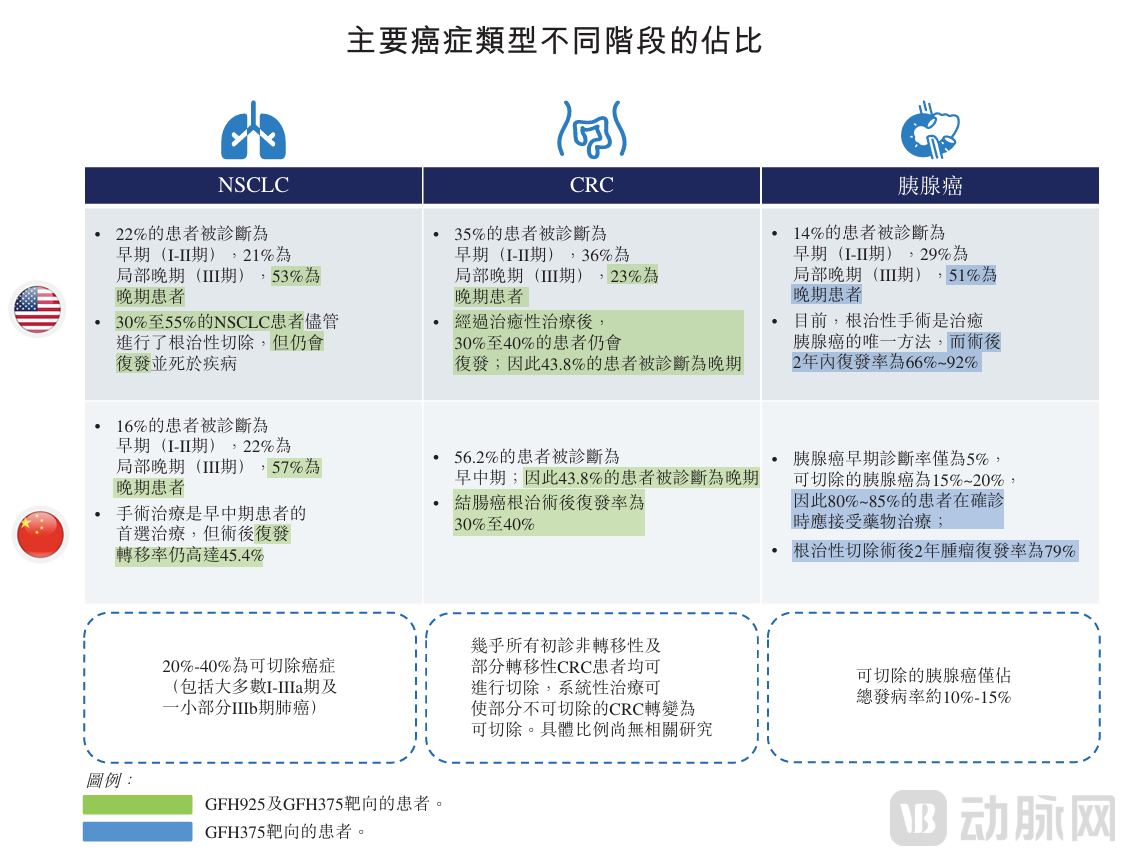

RAS, or rat sarcoma viral oncogene homolog, was the first human oncogene discovered in 1982, with mutations occurring in up to 30% of cancer patients. Among these, KRAS mutations are the most common, detected in approximately 90% of pancreatic cancer cases, 30–40% of colorectal cancers, and 15–20% of lung cancers. Due to the challenges in developing RAS-targeted drugs, it was not until the accelerated approval of Amgen's Lumakras in 2021 that the "undruggable" myth was finally broken.

Through proprietary R&D and collaboration with Innovent, GenFleet’s fulzerasib was approved in mainland China in August 2024 and subsequently in Macau, China this year. For domestic NSCLC patients with KRAS mutations, this marks a critical shift from traditional chemotherapy to precision targeted therapy. The registrational study of fulzerasib demonstrated a mPFS of 9.7 months (2–3 times longer than traditional chemotherapy), a cORR of 49.1% (2–4 times higher than chemotherapy), a DCR of 91%, and an ORR of 48.6% in patients with brain metastases (5 times higher than conventional chemotherapy).

Capitalizing on its deep focus on the RAS pathway, GenFleet Therapeutics has adopted a strategy of vertical expansion in target coverage coupled with horizontal diversification in molecular modalities, enabling breakthroughs through both refined interventions and novel mechanisms.

GFH375:

The G12D mutation represents the most prevalent KRAS mutation subtype across multiple tumor types. GFH375 has now entered Phase II trials, positioning it among the leading global oral KRAS G12D inhibitors. Clinical data for GFH375 have been presented at this year's ASCO and WCLC annual meetings, including a breakthrough research abstract at the latter, demonstrating its promising preliminary efficacy in treating pancreatic cancer and non-small cell lung cancer (NSCLC).

GFH276:

As a Pan-RAS (activated) molecular glue, GFH276 has now received clearance for Phase I/II clinical trials. In various RAS-mutant tumor models, GFH276 demonstrated a lower effective dose compared to overseas counterparts and maintained potent activity across multiple mechanism-induced KRAS inhibitor-resistant cell lines, indicating broad potential to overcome drug resistance.

Throughout this process, GenFleet's proprietary R&D platform has been progressively refined and matured, encompassing target discovery, molecular discovery and evaluation, translational science, global clinical development, production quality control, and regulatory affairs. After establishing the foundation for "China's first," GenFleet rapidly pivoted to tackling "global first-in-class" innovations—developing the internally created FAScon platform, a first-in-class functional antibody-targeted drug payload synergistic conjugate platform. Leveraging the synergistic effects of large and small molecules, FAScon enables the development of highly imaginative novel molecular structures.

Based on the clinically superior results of the GFH925/cetuximab combination therapy, GFS784 consists of a small molecule pan-RAS inhibitor and an EGFR antibody, simultaneously targeting both upstream and downstream mutations in the RAS signaling pathway. In preclinical studies, GFS784 demonstrated sustained antitumor activity in both Dxd payload-sensitive and -insensitive mouse models.

Beyond the RAS pathway, GenFleet is advancing GFS202A, the world's first GDF15/IL-6 bispecific antibody, which received clinical trial approval earlier this year for the treatment of cancer cachexia. Cachexia commonly occurs in chronic diseases such as heart failure, COPD, and chronic nephritis, leading to various wasting symptoms. Moreover, over 50% of cancer patients develop cachexia, and approximately 30% of cancer-related deaths are associated with this condition. Patients with gastrointestinal tumors, particularly pancreatic cancer, exhibit an exceptionally high incidence of cachexia. Currently, there are no approved targeted therapies specifically for cachexia in either China or the United States, highlighting a significant clinical unmet need.

2From First-Line Treatment of NSCLC to the Pancreatic Cancer Gap

Breakthroughs in targeted therapies require precision strikes—advancing into frontline treatments and expanding indications. An analysis of GenFleet’s core asset strategy reveals that precise clinical insights, efficient development tactics, and combination therapy collaborations are all indispensable. Overall, GenFleet is addressing a massive and rapidly growing market. The incidence rates of NSCLC, CRC, and PDAC continue to rise.

How does one identify key entry points in major disease areas? GenFleet's underlying logic is to start from clinical needs and innovative treatment concepts, leverage established technology platforms, and pursue both druggability and differentiation in its programs.

In 2023, the combination therapy of fulzerasib and cetuximab (GFH925/cetuximab) entered Phase I/II multicenter trials in Europe, making it the first KRAS inhibitor developed in China to go global in the first-line treatment race—demonstrating the company’s long-term commitment to advancement. This determination is supported by original global clinical development strategies and solid CMC expertise.

As the world's first KRAS+EGFR first-line combination therapy for lung cancer, it demonstrates excellent overall efficacy with significant activity against brain metastases and a superior safety profile compared to fulzerasib monotherapy in the second-line setting. According to breakthrough research abstract data presented at this year's ELCC, the ORR was 80%, DCR reached 100%, and mPFS was 12.5 months. As of the latest practicable date, the patent term for fulzerasib remains valid for over 15 years, and coupled with the global leadership of this first-line combination therapy, the window of opportunity remains open.

In the field of pancreatic cancer, GenFleet's core strategy centers on GFH375, a KRAS G12D-targeted agent for which the company retains Greater China rights and is independently advancing domestic clinical development. This path has proven highly efficient—within just nine months, GenFleet progressed GFH375 from IND to Phase II, focusing on patients with KRAS G12D-mutant PDAC, NSCLC, or CRC. The company plans to initiate pivotal studies for PDAC and NSCLC. Furthermore, GFH375 is expected to form a targeted therapy matrix against pancreatic cancer in the future, combining with GenFleet's pan-RAS inhibitors, EGFR-Pan RAS conjugate drugs, and the cachexia-targeting bispecific antibody GFS202A.

3The Only Biotech with Both Approved Drug and BD Revenue at HKEX IPO Stage

Following this logic, GenFleet's strategic approach of "Product + BD" dual-driven growth with self-sustaining capabilities becomes clear. The company initiated its business development efforts well ahead of China's "wave of innovative drug globalization," engaging in both domestic collaborations and out-licensing partnerships.

As of the first half of 2025, among the 73 biotech companies listed under HKEX Chapter 18A, several have adopted this dual-driven model of "commercialized products + global BD partnerships," including BeiGene, Innovent Biologics, Henlius, and Akeso. However, GenFleet stands out as the only company to have successfully implemented both components by the time of its IPO.

In 2021, following the clinical approval of GFH925 in China, GenFleet entered into an in-licensing partnership with Innovent Biologics, creating what was then the largest transaction for a local asset at the IND stage in China. This collaboration leveraged GenFleet's strengths in small molecule R&D and production alongside Innovent's clinical and commercial capabilities, enabling rapid clinical advancement and eventual new drug approval. In 2022, GenFleet established an out-licensing agreement with U.S.-listed SELLAS for GFH009 (a CDK9 inhibitor), which has now entered multiple Phase II studies in both China and the U.S., and has received designations from the FDA and EMA including Fast Track, Orphan Drug, and Rare Pediatric Disease Therapy. In 2023, GenFleet signed an overseas licensing and collaboration deal with U.S.-listed Verastem Oncology valued at over $600 million, with GFH375 serving as the lead asset among the three partnered therapies.

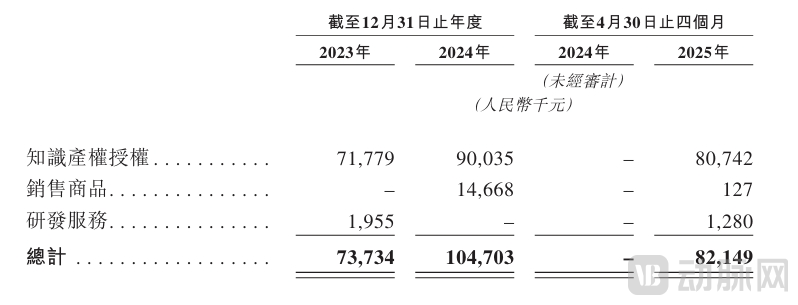

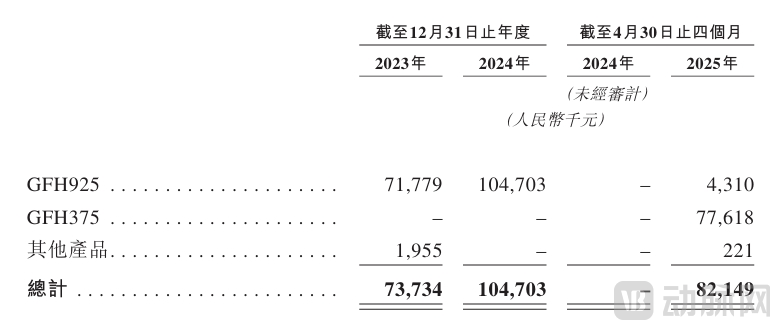

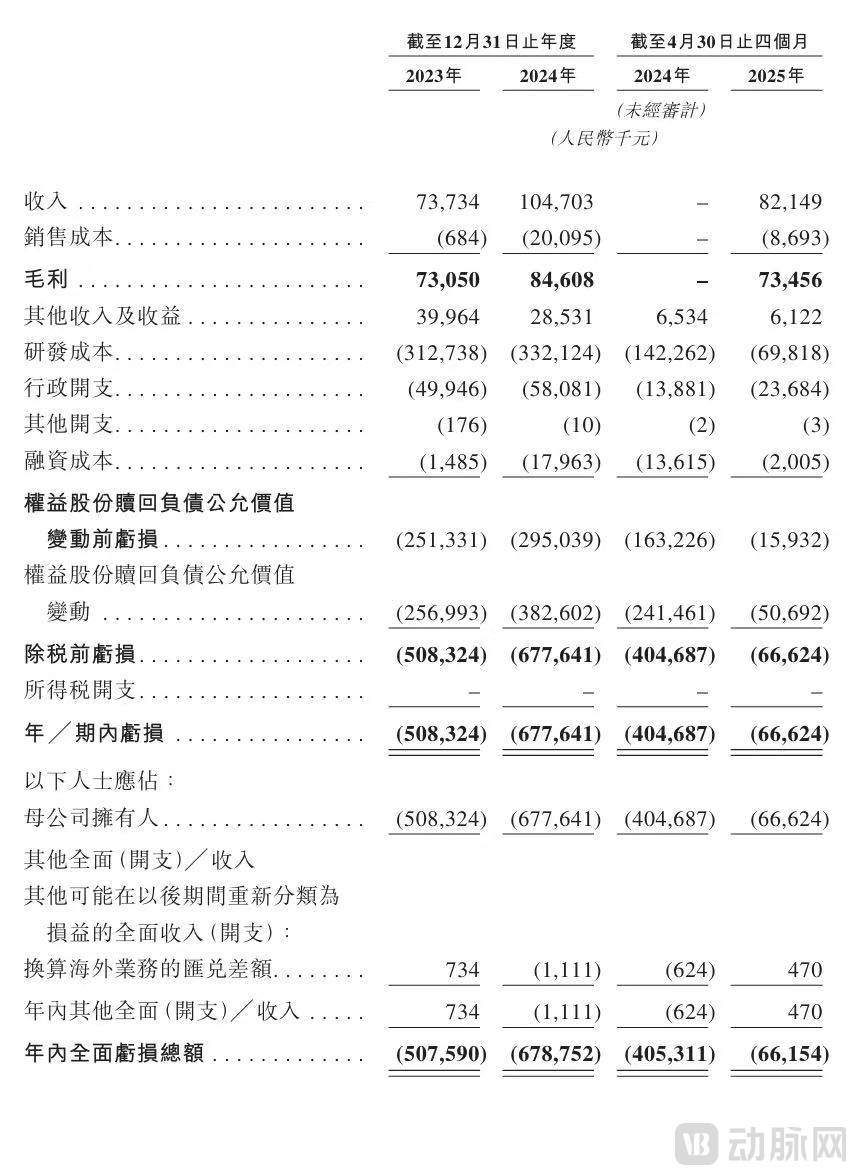

At the financial operational level, the majority of GenFleet's revenue derives from licensing income, milestone payments, and sales royalties from external partnerships. According to the prospectus, the company's annual revenue increased from RMB 73.73 million in 2023 to RMB 105 million in 2024, representing a growth rate of 42.4%. Revenue for the first four months of 2025 reached RMB 82.15 million, primarily attributable to licensing income from GFH375.

Financial Data - Main Components of Revenue

Financial Data - Consolidated Income and Other Comprehensive Income Statement

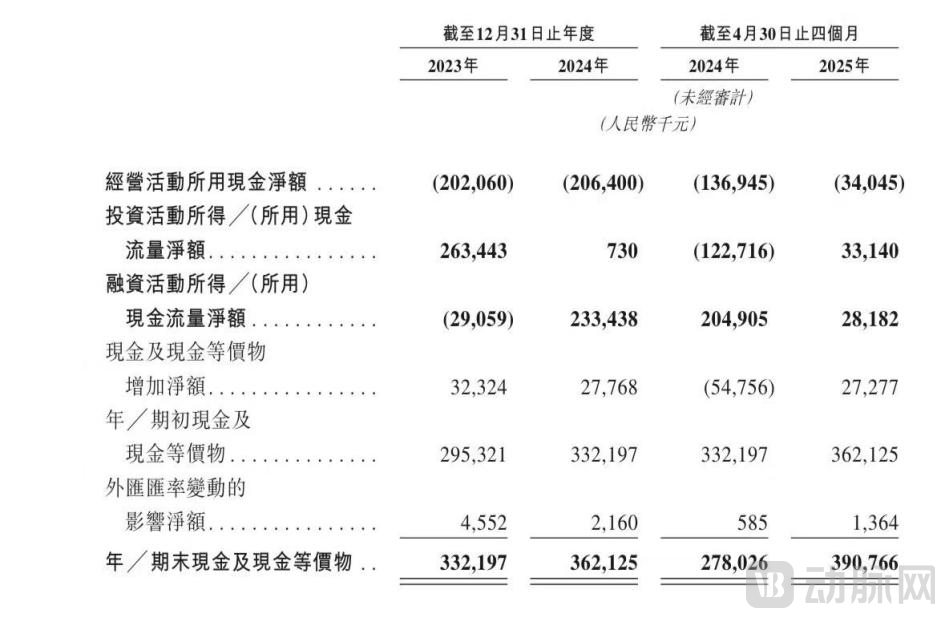

From a cash flow perspective, although GenFleet has not yet achieved profitability and is simultaneously advancing late-stage clinical development of core products both domestically and internationally, it demonstrates positive signals of cash flow stability. Cash and cash equivalents increased from RMB 332 million in 2023 to RMB 362 million in 2024. As of April 30, 2025, cash and cash equivalents stood at RMB 390 million.

Financial Data - Consolidated Cash Flow Statement

Financial Data - Consolidated Cash Flow Statement

BD-driven self-sustainability and pioneering innovative pipelines represent both an exploration and a return to fundamentals for biotechs adapting to the evolving global pharmaceutical landscape. From co-commercializing core assets to independently conducting overseas clinical trials, from securing out-licensing deals to collaborating with MNCs on combination therapies—the extensive experience gained in partnerships and global expansion over the years has laid a solid foundation for GenFleet's future growth in the global market.

Guided by a product-first, druggability-first, and efficiency-first philosophy, how will GenFleet continue to shape the legacy of Chapter 18A biopharma innovation?