From Chinese pipelines to Nasdaq: the Newco that raised $505M goes public via merger

Rallybio

Developer and Manufacturer of Rare Disease Therapeutics

Candid

3D Printing Dental Company

EpimAb Biotherapeutics

Developer of Tumor Bispecific Antibodies

On March 2, 2026, Nasdaq-listed Rallybio (RLYB) and clinical-stage biotechnology company Candid Therapeutics ("Candid") announced a merger agreement. According to the agreement, the combined entity will operate under the name Candid Therapeutics and trade under the stock code "CDRX." As a key component of the transaction, Candid simultaneously completed a private financing of $505 million. The investor syndicate is prestigious, including top-tier healthcare venture capital firms such as Venrock and RA Capital Management, as well as globally renowned asset management companies like Janus Henderson Investors. The proceeds are expected to provide the new company with operating capital through 2030.

Furthermore, according to the plan, the combined company will continue advancing Candid's diversified T-cell engager pipeline toward multiple key clinical milestones, including initiating Phase 2 clinical studies for myasthenia gravis and rheumatic disease-associated interstitial lung disease in 2026.

The most noteworthy aspect of this transaction is not the merger itself, but the identity of Candid Therapeutics—a company that officially debuted in September 2024, having been established for only six months, with its core assets entirely sourced from Chinese biotechnology companies. From EpimAb Biotherapeutics' BCMA×CD3 bispecific antibody, to Genor Biopharma's CD20×CD3 bispecific antibody, to research collaborations with WuXi Biologics, Nona Biosciences, and Ab Studio, the names of Chinese innovative drug companies are densely arrayed across Candid Therapeutics' pipeline landscape.

Chinese Pipelines + Global Operators: Why Clinical Data Was the Ultimate Deal-Maker

Candid's very inception carried a strong Sino-American hybrid character.

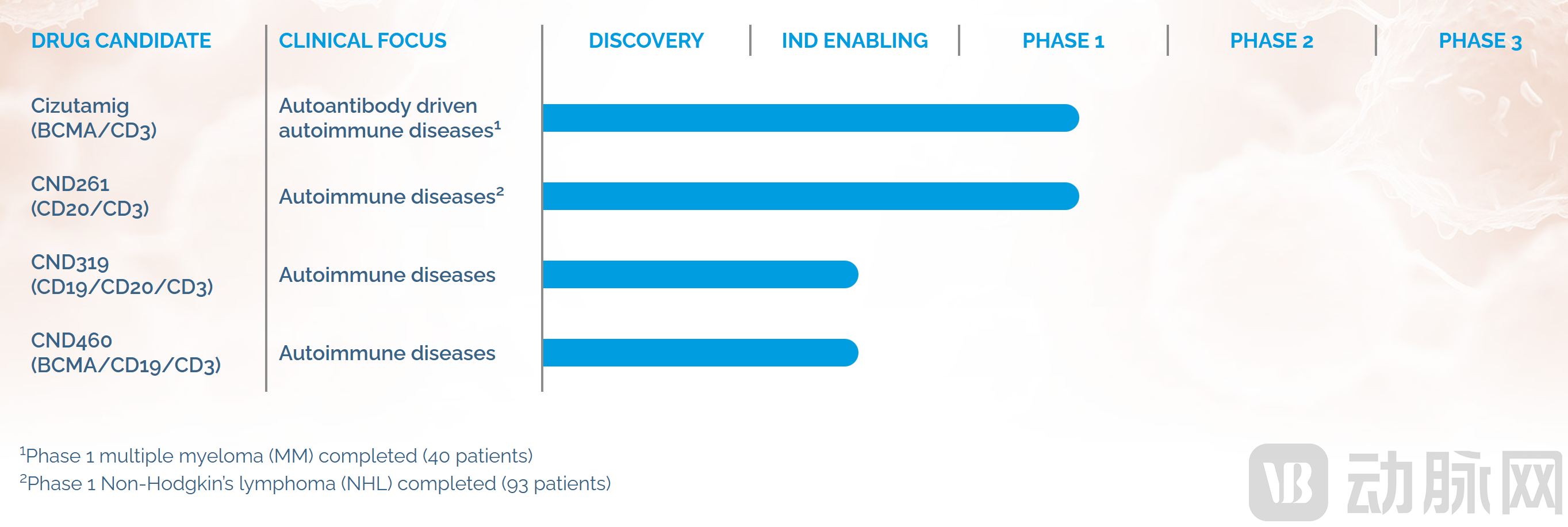

In September 2024, Candid set a new financing record for the biopharmaceutical industry that year with a $370 million Series A funding round, featuring investors including nearly 20 top-tier healthcare funds such as Venrock, Fairmount, TCGX, venBio, and Third Rock. At that time, Candid simultaneously announced the acquisition of two Newcos established almost concurrently—Vignette Bio and TRC 2004—thereby obtaining two core pipeline assets: CND106 targeting BCMA and CND261 targeting CD20.

The origins of both pipelines lie in China. CND106 originated from EpimAb Biotherapeutics' EMB-06, and CND261 originated from Genor Biopharma's GB261. Notably, EpimAb and Genor did not simply sell their assets; instead, they adopted a model of exchanging global rights to their assets for equity in the Newco, becoming shareholders in Candid. This means that if Candid's value is realized in the future, these two Chinese biotech companies will also be able to share in the returns.

Candid's operator, Ken Song, is a serial entrepreneur in the U.S. biopharmaceutical sector. His previous company, RayzeBio, took only three years from its founding to being acquired by BMS for $4.1 billion. The core capabilities of Ken Song's team were summarized by Wu Chenbing, CEO of partner EpimAb Biotherapeutics, into three points: strong scientific judgment, rapid team assembly, and high capital cohesion ability. This capability is vividly demonstrated in Candid: less than four months after its establishment, Candid announced on a single day three TCE collaboration agreements with Nona Biosciences, EpimAb Biotherapeutics, and Ab Studio, further expanding its early-stage research pipeline.

In January 2026, Candid secured another deal, signing an exclusive global license agreement with WuXi Biologics for a trispecific TCE antibody, with a total transaction value of up to $925 million, adding a CD19/CD20 dual-targeting TCE to its portfolio.

Thus, Candid has constructed a TCE pipeline matrix covering multiple B-cell targets including BCMA, CD20, and CD19. Candid's willingness to place significant bets on Chinese assets so early in its existence was not blind acquisition but was based on the fact that these pipelines had already been validated by clinical data.

The distinctiveness of Ken Song and his team lies not just in being entrepreneurs, but in acting as asset portfolio managers, capable of identifying the most promising opportunities among numerous projects, rapidly integrating resources, driving up value, and then exiting at an opportune time. According to public reports, Ken Song's team evaluated nearly 50 TCE assets before deciding to invest in EpimAb Biotherapeutics' EMB-06. The core reason for ultimately selecting EpimAb and Genor was that these two molecules had already undergone preliminary clinical validation.

Both CND106 (EpimAb Biotherapeutics' EMB-06) and CND261 (Genor Biopharma's GB261) have completed Phase I clinical trials for oncology indications, enrolling over 130 and 100 patients respectively. This means that the safety of these two molecules has been validated in humans, and they have preliminarily demonstrated pharmacological activity.

More critically, these molecules have demonstrated favorable safety profiles. The core pipeline asset, cizutamig (CND106), precisely binds to both BCMA and T-cell CD3, mediating specific T-cell killing of BCMA-positive B cells. This achieves deep tissue-level depletion, laying the foundation for disease remission.

Candid disclosed in its merger announcement that among 87 patients treated with cizutamig, including 47 patients with autoimmune diseases, less than 20% experienced mild cytokine release syndrome. No adverse events of immune effector cell-associated neurotoxicity syndrome were observed. Its favorable tolerability supports an outpatient administration model, significantly enhancing treatment accessibility.

CND261 has also demonstrated promising performance. This CD20×CD3 bispecific antibody was engineered with reduced CD3 affinity to avoid excessive T-cell activation while maintaining potent B-cell depletion capability. To date, CND261 has been administered to over 110 patients, including more than 20 patients with autoimmune diseases, with favorable safety data: less than 20% of patients experienced Grade 1 CRS, and no ICANS occurred.

Additionally, Candid's pipeline includes CND319, a dual-targeting CD19/CD20 TCE, which has shown a promising therapeutic index profile in non-human primate studies. A first-in-human study is planned for mid-2026.

Acquiring Chinese TCE Assets Through Newcos: A Long-Term Play

At first glance, there is reason to view Candid as the epitome of the Chinese biotech overseas expansion Newco model in recent years.

The so-called Newco model involves overseas experienced teams and capital jointly establishing a new company. Chinese pharmaceutical companies contribute pipeline rights in exchange for equity in the Newco and future revenue sharing. In other words, the Newco model bridges the technological value of Chinese assets with the capital operation capabilities of overseas teams. This model experienced an explosion in 2024: in addition to Candid's acquisitions from EpimAb Biotherapeutics and Genor Biopharma, several other Chinese pharmaceutical companies—including Leads Biolabs, Keymed Biosciences, Curon Biopharmaceutical, and Chimagen—also licensed out their TCE pipelines through the Newco model.

Candid's growth trajectory clearly demonstrates the power of this approach. From its inception to acquiring a public listing platform, Candid took less than two years—a speed unimaginable for traditional biotech companies.

On the other hand, the rapid pace of Candid's actions, combined with Ken Song's previous entrepreneurial experiences, led some to believe that Candid might also be a "fast-in, fast-out" Newco. As recently as late 2024, there were voices suggesting that Ken Song's team aimed to rapidly advance clinical development and ultimately be acquired by a large company, profiting from the differential.

However, industry insiders did not share this view. According to public interviews and reports, after Candid acquired two TCE assets and initiated three early-stage research collaborations, Wu Chenbing noted in an interview that Ken Song genuinely intended to innovate and build a company, possessing "long-term strategic planning, a desire to create value, a commitment to innovation, and an ambition to scale up in the autoimmune TCE field."

TCE, as a bispecific antibody, operates on a core mechanism: one arm engages T cells (typically via CD3), and the other arm recognizes and engages target cells, forcing T cells to kill the target cells. Compared to earlier autologous CAR-T therapies, TCEs offer several core advantages: first, they are an "off-the-shelf" drug modality requiring no customized manufacturing and allowing batch production; second, they have a more controllable safety profile, with lower incidence and milder severity of cytokine release syndrome. This "ready-to-use" characteristic also gives TCEs the potential for outpatient administration, broadening patient accessibility.

Over the past two years, the TCE field has undergone a migration from oncology to autoimmune diseases. According to data, the number of global TCE clinical trial initiations rose significantly to 175 in 2024, including 13 trials for immune diseases, with strong growth momentum. The core driver of this migration is the breakthrough efficacy achieved by CD19 CAR-T in autoimmune diseases such as lupus erythematosus. However, the manufacturing cost and process complexity of CAR-T inherently limit its application to a very small number of patients, making TCE the only viable solution to fill this gap.

Returning to the Candid case, Ken Song's team chose the autoimmune TCE field, not oncology. Oncology TCEs already have more mature markets and clearer regulatory pathways, making them faster to develop and easier to exit from. However, autoimmune TCE represents a direction requiring long-term investment, exploration of the unknown, and acceptance of failure risk. The reason for choosing this path is not speed, but scale—the market size for autoimmune diseases far exceeds that of oncology, and success in this area would represent a true paradigm shift.

At this point, the Candid case further validates that, beyond initial public offerings and traditional financing, the Newco model can provide Chinese biotech companies with a new path for sustainable development. Exchanging assets for equity and gaining future appreciation is becoming a pragmatic exit strategy.

First, the foundational capabilities of Chinese biotechnology are gaining increasing global recognition, and Chinese companies are expanding their influence. Whether in oncology or autoimmune diseases, Chinese TCE bispecific antibody assets are becoming hard currency in the global transaction market.

Simultaneously, the potential of TCEs in autoimmune diseases is accelerating towards realization. Candid plans to initiate global Phase 2 clinical trials for cizutamig in myasthenia gravis and rheumatic disease-associated interstitial lung disease in 2026. If the data are positive, this could represent another revolution in the treatment of autoimmune diseases, following the breakthrough of CD19 CAR-T.