Vietnam's healthcare gold rush: why Chinese companies are flocking

"The takeoff of the Vietnamese economy", "Vietnam replacing China as the world's factory", "Vietnam becoming a developed country within five years"... these were hot topics frequently seen on Chinese social media in 2025. While there is a degree of exaggeration and hype in these narratives, they are not entirely without a foundation in reality.

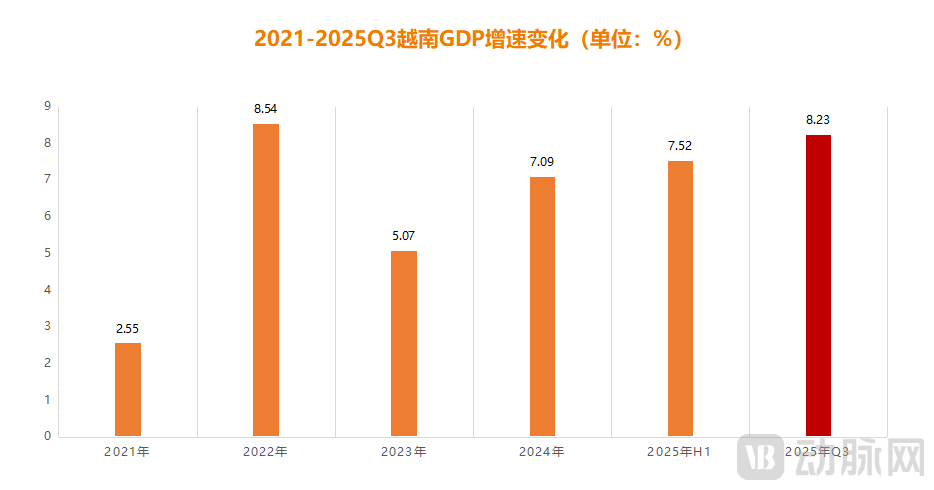

Figure 1. GDP Growth Rate Changes in Vietnam from 2021 to Q3 2025 (Data Source: Vietnam General Statistics Office, Chart by VCBeat)

Figure 1. GDP Growth Rate Changes in Vietnam from 2021 to Q3 2025 (Data Source: Vietnam General Statistics Office, Chart by VCBeat)

From the most direct economic perspective, according to statistics from the General Statistics Office of Vietnam, Vietnam's Gross Domestic Product (GDP) in the first half of 2025 grew by 7.52% year-on-year, reaching a 15-year high. In the third quarter, GDP grew by 8.23% year-on-year, making it a certainty that the annual growth rate will surpass 8%. Against the backdrop of weak consumption and widespread economic downturn in many global economies, Vietnam has indeed emerged as the most prominent growth pole among emerging markets.

In terms of investment attraction, Vietnam's performance has also been remarkable. According to data from the Ministry of Finance of the Socialist Republic of Viet Nam, in the first half of 2025, Vietnam attracted Foreign Direct Investment (FDI) amounting to $21.51 billion, a year-on-year increase of 33%. The number of newly registered foreign-invested enterprises reached 1,988, up 21.7% year-on-year. Furthermore, global giants such as Samsung, NVIDIA, Apple, Intel, and Foxconn have continued to increase their investments in Vietnam. Taking Samsung as an example, by mid-2025, the company had relocated half of its global mobile phone production capacity to Vietnam, with cumulative investment reaching a total of $23.2 billion.

This is indeed a market full of potential, and Chinese healthcare companies, eager to expand overseas, have keenly sensed the opportunity. Consequently, in 2025, they began flocking to Vietnam, with frequent activities ranging from building factories and making investments to obtaining certifications and establishing channels. For instance, in May of this year, Livzon Pharmaceutical announced the acquisition of a controlling stake in the Vietnamese pharmaceutical company Imexpharm for 5.73 trillion Vietnamese Dong (approximately $220 million). This marks the first time Chinese capital has achieved substantive control over a leading listed company in Vietnam's pharmaceutical industry. In October, Haier Biomedical entered into a strategic cooperation with Vietnam's renowned stroke treatment center, S.I.S International Hospital, and the Vietnamese medical company VT Healthcare. Together, they are promoting the implementation of Vietnam's first "Hospital-wide Intelligent Digital Solution for Medication Management."

In fact, there are many similar collaborations. One telling statistic is that in the first quarter of 2025 alone, 391 new Chinese enterprises registered in Vietnam, with healthcare companies accounting for over 20% of this number. Amidst these astonishing figures, a pressing question is growing louder: Why are Chinese healthcare companies flocking to Vietnam? What models are they adopting for their market entry? What are the potential future risks, and how can they be mitigated? The answers may lie within those Chinese healthcare companies that have already ventured into Vietnam.

Why Vietnam?

Vietnam's healthcare market is expanding at a remarkable pace. According to data from the Drug Administration of Vietnam - Ministry of Health, the country's pharmaceutical market reached a size of $8 billion in 2023, with an annual growth rate maintained between 8% and 10%. It is projected that by 2030, the market size will grow to $16 billion. In terms of medical devices, the market size is expected to increase to $1.77 billion by 2025 and surpass $2.47 billion by 2029, representing a compound annual growth rate (CAGR) of 8.62%.

Figure 2. Import Proportion in Vietnam's Medical Device Field (VCBeat Mapping)

Figure 2. Import Proportion in Vietnam's Medical Device Field (VCBeat Mapping)

However, within this rapidly growing market, Vietnam's healthcare industry remains heavily dependent on imports, with the import dependency rate for medical devices reaching as high as 90%. It is reported that domestically produced devices account for less than 10% of the market share, predominantly consisting of simple, low-value items such as surgical scalpels and disposable medical products. High-precision equipment like ultrasound and magnetic resonance imaging (MRI) machines, as well as other advanced devices for surgery, endoscopy, sterilization, and testing, are primarily sourced from overseas. Approximately 55% of these imports come from Japan, Germany, the United States, China, and Singapore.

A similar situation exists in the pharmaceutical sector. GSO data show that the Vietnam's domestic drug production capacity meets only about 53% of its domestic demand, with the output mainly consisting of generic drugs. Consequently, Vietnam's annual expenditure on imported pharmaceuticals exceeds $5 billion. Key imported drug categories include antibiotics, cardiovascular medicines, anticancer drugs, vaccines, and diabetes treatments, primarily sourced from countries such as the United States, Japan, India, and China. For active pharmaceutical ingredients (APIs), Vietnam relies heavily on China and India, which together account for over 90% of its total API imports.

Beyond its high import dependency, Vietnam's sustained demographic dividend, rapidly expanding healthcare needs, gradually easing market access policies, and increasing health insurance coverage have collectively made it a highly contested overseas destination for global healthcare companies.

First, regarding the demographic dividend, Vietnam currently has a population of approximately 100 million, with 68% falling within the 15-64 age range, indicating it is in a "demographic golden structure" period. Compared to the current aging curves of China, Japan, and South Korea, Vietnam's "ageing burden" phase is not expected to arrive for at least another 15 to 20 years. This suggests that not only is current healthcare demand robust, but it is also poised for sustained expansion over the next generation.

Secondly, on the crucial payment front, data from Vietnam Social Security shows that in 2023, the number of insured individuals exceeded 93.3 million, achieving a health insurance coverage rate of 93.35%. Annual total health insurance expenditures surpassed 439 trillion Vietnamese Dong (VND; approximately $16.83 billion). Additionally, the rapid rise of Vietnam's middle class has significantly enhanced out-of-pocket spending capacity for healthcare. From 2019 to 2024, the proportion of the middle-income group increased from 26.86% to 33.07%, while the middle-to-high-income group grew from 14% to 23%. This evolving "olive-shaped" income structure is not only unleashing demand for premium medical services but also creating substantial market space for the penetration of private healthcare institutions, international health insurance products, and commercial health insurance.

Figure 3. Differences and timelines in Vietnam's medical device approval pathways (Chart by VCBeat)

Figure 3. Differences and timelines in Vietnam's medical device approval pathways (Chart by VCBeat)

Next is the aspect of market access. As early as 2019, Vietnam's amended Pharmacy Law permitted foreign enterprises to directly apply for drug registration certificates for the first time and significantly streamlined the clinical trial approval process, reducing the approval timeline from 12-18 months to 6-9 months. Regarding medical devices, the Law on Medical Devices, which took effect in 2022, devolved the registration authority for 70% of Class II devices and all Class I devices to provincial health departments, cutting approval times by 40%. Furthermore, starting July 2025, the Vietnamese Ministry of Health reduced medical device registration fees by 50%, further alleviating the burden on companies. As a highly import-dependent healthcare market, Vietnam is expected to establish more "green channels" for overseas medical products in the future to meet its rapidly growing health demands.

Finally, advantages are evident in production. Leveraging a plentiful young workforce, a low-cost structure, and export benefits derived from various free trade agreements, Vietnam is progressively evolving into a global base for the low-cost, large-scale production of medical consumables and pharmaceuticals. This not only offers significant cost advantages to established companies but also enhances supply chain resilience, thereby maintaining competitiveness in the global market.

In light of this, against the backdrop of its own growth demands and regional policy dividends, Vietnam is emerging as an exceptional springboard for healthcare overseas expansion and a strategic industrial hub.

From Simple Product Sales to Deep Integration of the Entire Industry Chain

As early as 1996, China and Vietnam signed a bilateral pharmaceutical cooperation agreement, laying the groundwork for subsequent exchanges and collaboration. Around the year 2000, pioneering Chinese pharmaceutical companies including Sinopharm, Guangzhou Pharmaceutical Holdings, Yunnan Baiyao Group, China Resources Pharmaceutical, and Yiling Pharmaceutical began initial forays into Vietnam, primarily exporting traditional Chinese medicinal materials and active pharmaceutical ingredients (APIs). Among them, Guangzhou Pharmaceutical's Huatuo Zaizao Wan became the first foreign traditional medicine included in Vietnam's health insurance drug list.

In the following years, cooperation between Chinese healthcare enterprises and the Vietnamese market gradually expanded and deepened. To date, several companies have achieved significant success in Vietnam. Taking Sinopharm as an example, as the first Chinese company to establish a production plant in Vietnam that meets WHO-GMP standards, it now achieves 95% market coverage and a 25% market share in Vietnam, reaching the hundreds of millions of RMB range. Another representative company is INTCO Medical. Since investing $140 million to build a factory in Vietnam in 2019, its market share has rapidly increased to 18%, with local sales in 2023 nearly quadrupling compared to 2020. Additionally, companies such as Kanghui Medical, Mindray, Bluesail Medical, YHLO Biotech, and Fosun Pharma have also achieved notable success in the Vietnamese market.

Entering 2025, as export-related advantages have further materialized, an increasing number of Chinese companies are entering the Vietnamese market. This time, how are they establishing their presence? Through case analysis, VCBeat has identified that their approaches are primarily focused on three key areas: investment, product approval and market sales, and core business partnerships.

Starting with investment, companies are making substantial commitments to Vietnam through various methods including mergers and acquisitions (M&A), factory establishment, and joint ventures. As mentioned earlier, in May of this year, Livzon Pharmaceutical acquired a controlling 64.81% stake in the Vietnamese listed pharmaceutical company Imexpharm for 5.73 trillion Vietnamese Dong. This was not merely a simple transaction but a crucial part of Livzon's localization strategy for production. It is reported that Imexpharm possesses three EU-GMP certified factory clusters, holds over 300 local Vietnamese drug registration certificates, and maintains a distribution network covering 29 Vietnamese provinces and cities. This allows Livzon to localize its R&D, production, and sales operations in Vietnam simultaneously, enabling rapid, "plug-and-play" market expansion.

This point is critical. Although the Vietnamese market is relatively open, its strategy has consistently been to ensure that all foreign enterprises develop local operations within Vietnam, a trend that has noticeably strengthened in recent years. Therefore, for Chinese healthcare companies aiming to establish deep roots in Vietnam, investment methods such as M&A, factory setup, and joint ventures represent the fastest strategies to achieve localized operations. In April 2024, DIAN Diagnostics simultaneously established two subsidiaries in Vietnam: DIAN Diagnostics Vietnam Laboratory and DIAN Vietnam. In the first half of 2025, the laboratory successfully obtained local ISO 15189 certification and external quality assessment certification, marking its critical transition from "product export" to "localized operation" in Vietnam.

Figure 4. Some Chinese medical device products approved for marketing in Vietnam in 2025 (VCBeat Mapping)

Figure 4. Some Chinese medical device products approved for marketing in Vietnam in 2025 (VCBeat Mapping)

Second, focusing on the level of product exports. According to incomplete statistics, as of November 30, 2025, nearly a hundred medical products from China had been approved for market launch in Vietnam, predominantly medical devices. Representative examples include Allgens Medical's BonGold artificial bone repair material, Haifu Medical's ultrasound tumor therapy system, and Tongee Medical's gastric bypass stent. In terms of pharmaceuticals, Hybio Pharmaceutical's Atosiban Acetate Injection was approved in Vietnam in August 2025, primarily indicated for pregnant women with signs of preterm labor. In November, Baiyunshan Zhongyi Pharmaceutical's Angong Niuhuang Wan successfully obtained its drug registration certificate in Vietnam, forming a dual-product driving strategy alongside Huatuo Zaizao Wan, which has been a bestseller in Vietnam for nearly 20 years.

Beyond market approvals, several other medical products have secured distribution rights in Vietnam. For instance, in October 2025, Buchang Pharma authorized Helios as the exclusive distributor for Efparepoetin alfa for Injection within Vietnam for RMB 512 million. Also in October, TaiGen Biotechnology licensed the development and sales rights for its novel antibiotic "Taijiexin" (Nemonoxacin) in Vietnam to two Vietnamese pharmaceutical companies, leveraging their complementary strengths to facilitate market entry.

Lastly, collaboration extends to the operational level with Vietnamese institutions. In June 2025, Hengrui Pharma entered the high-end market by partnering directly with a large Vietnamese private hospital group, focusing on oncology injectables and complex dosage forms. In September, Mindray announced the signing of a comprehensive memorandum of understanding with Benh Vien Bach Mai Hospital to help establish Vietnam's first critical care talent certification system compliant with JCI standards. In November, Fubao Robot entered into a strategic partnership with Vietnam's TCI Hospital to facilitate the first large-scale deployment of a "Hospital-wide Intelligent Logistics Robot Solution" in the Vietnamese market.

In fact, compared to investment and product exports, business-level cooperation represents a deeper method of engaging with Vietnam's healthcare industry chain. It establishes direct links with hospitals or laboratories and progressively embeds companies into the standard-setting, talent cultivation, clinical pathways, and operational processes of the Vietnamese healthcare system, thereby fostering long-term, sustainable synergistic relationships.

Commenting on this trend, a founder of a company with long-standing operations in Vietnam noted, "From my personal observation, 2025 has indeed seen a significant presence of Chinese healthcare companies in Vietnam. They come from various subsectors, and their forms of collaboration are highly diversified. They are no longer limited to simple product sales but are engaging more deeply in the construction of the local healthcare ecosystem, aiming for broader market prospects."

A Dual Game of Speed and Risk

Expanding overseas carries risks, and investment requires prudence. Although Vietnam is an emerging market, significant challenges remain for Chinese healthcare companies venturing there.

One major challenge is facing intense competition from global products. In fact, Chinese healthcare companies entered the Vietnamese market relatively late and lack first-mover advantage. Currently, countries such as Japan, the United States, Germany, and South Korea have already established mature industrial chain systems in Vietnam. Taking Japan as an example, as early as the 1990s, companies like Olympus, Fujifilm Corporation, Toshiba Medical Systems, and Terumo began providing medical equipment and infrastructure support to Vietnam through Official Development Assistance (ODA) projects. To date, they have secured a dominant share in the Vietnamese market for high-end imaging, endoscopic, and radiology equipment.

It is also noteworthy that the Japan International Cooperation Agency (JICA) has included "medical equipment renewal" in its ODA catalog for Vietnam since 2006. These projects offer extremely favorable terms, such as interest rates as low as 0.1% and repayment periods of up to 40 years, but come with a clause stipulating "priority procurement of Japanese products." This makes it exceptionally difficult for latecomers to win bids, even with quotations up to 30% lower. Therefore, for Chinese healthcare companies to break through this entrenched landscape, relying solely on traditional cost-effectiveness or sales channels is insufficient. They must adopt more strategic, differentiated, and systematic approaches, employing a comprehensive "combination of strategies" to pry open a crack in the market.

Figure 5. Market share of the United States, Japan, South Korea, Singapore, and Germany in Vietnam's medical market (Chart by VCBeat)

Figure 5. Market share of the United States, Japan, South Korea, Singapore, and Germany in Vietnam's medical market (Chart by VCBeat)

A seasoned investor familiar with the Vietnamese healthcare market commented: "The Vietnamese market has long been influenced by companies from Europe, the United States, Japan, and South Korea. As a result, the vast majority of hospitals still place greater trust in American, Japanese, and German brands for major equipment such as CT and MRI scanners. This obviously presents higher demands for Chinese companies. They must not only maintain technological reliability and cost advantages but also gain a deeper understanding of local clinical needs and win long-term trust by creating sustainable healthcare value."

Another significant challenge stems from the influence of geopolitics. In fact, a major reason for Vietnam's rapid development this year is its role as an industrial intermediary amid the trade tensions between the United States and China, which has allowed it to benefit from wider price margins. However, geopolitical uncertainties could alter this favorable situation at any time. Should the international trade environment change or relations between major powers improve, Vietnam's advantageous position as an intermediary, developed amidst the tensions, may gradually weaken. This requires Chinese healthcare companies expanding into Vietnam to build resilience against risks and deepen their localization efforts to withstand potential fluctuations in policies and the trade environment.

At the recently concluded Vietnam Medi-pharm, the scale of participation by Chinese healthcare companies was unprecedentedly large, accounting for 52% of exhibitors and forming the largest overseas contingent. Beyond the sheer number of participants, the business collaborations secured were highly substantial, with on-site contract signings over $500 million, a 65% increase compared to the previous session. This vividly demonstrates the determination and proactive efforts of Chinese healthcare companies in expanding into Vietnam. However, amidst this enthusiasm, it is crucial to remain rational, continuously uncover genuine local healthcare needs, and achieve localized development in Vietnam at the earliest opportunity.